Acquisition Costs under SFAS 19

1 / 21

Title:

Acquisition Costs under SFAS 19

Description:

Top Lease. A top lease is one where the WI owner wants to lease the property again and ... 3. Measure the loss by writing down asset to discounted future cash flows. ... – PowerPoint PPT presentation

Number of Views:30

Avg rating:3.0/5.0

Title: Acquisition Costs under SFAS 19

1

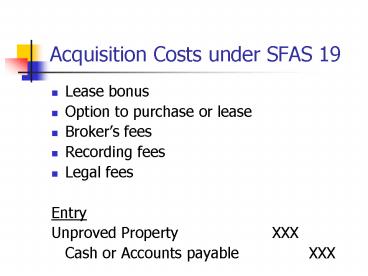

Acquisition Costs under SFAS 19

- Lease bonus

- Option to purchase or lease

- Brokers fees

- Recording fees

- Legal fees

- Entry

- Unproved Property XXX

- Cash or Accounts payable XXX

2

Database of Properties

- Items included in database

- Location and legal description

- Proved or unproved

- Parties to the agreement

- Royalty owners

- Working interest owners

- Used for the following functions

- Revenue distribution

- Joint interest billing

3

More Complex Acquisition Costs

- Purchase in fee Allocate between the surface

rights and mineral rights based on relative FMVs - Internal Costs Cost of internal legal and land

department costs should be allocated to

properties - Allocate first between acquisition activities and

other activities. - Allocate acquisition costs to properties acquired

based on acreage acquired or - Capitalize acquisition cost for properties

acquired and expense for allocable costs for

properties not acquired

4

Example Problem 4-8

- Sure Things internal land departments allocable

costs for acquisition of leases is given as

150,000. - Of the 1,000,000 acres of prospects evaluated,

450,000 acres were leased. - 45 to unproved properties - 67,500

- 55 expensed 82,500

5

Shooting Rights with Option to Lease

- Shooting rights should be expensed

- Option

- capitalized until it is known whether acreage

will be acquired - If acquired, unproved property

- If not acquired, expensed

- Treatment of shooting rights coupled with an

option to lease in practice - If acquired, entire amount usually capitalized

- If a portion is acquired, all usually capitalized

6

Example Problem 14

- From Mr. T

- Mabel Oil shooting right _at_ .10/acre for 15,000

acres 1,500. - Spent 85,000 on GG.

- Leased 5,000 acres for 35/acre 175,000

- GG expense 1,500

- GG expense 85,000

- Unproved property 175,000

7

Example Problem 14 (Contd)

- From Mr. H

- Shooting rights and option to lease for .25/acre

on 10,000 acres - 2,500. - Leased 5,000 acres for 35/acre 175,000.

- Property purchase suspense 2,500

- Unproved property 175,000

- Then move the 2,500 to unproved property

8

Delinquent Taxes and Mortgage Payments

- To get a clear title, lessee may have to pay back

taxes and mortgage payments. - Can these payments be recovered from lessor???

- If nonrecoverable, capitalize as part of

acquisition costs of property - If recoverable, set up as an account receivable

9

Example of Delinquent Taxes

- If not recoverable

- Unproved property 300

- Cash 300

- If recoverable from delay rentals

- Receivable 300

- Cash 300

- Delay rental expense 400

- Receivable 300

- Cash 100

10

Top Lease

- A top lease is one where the WI owner wants to

lease the property again and executes a new lease

prior to expiration of the old lease. - If execution is prior to expiration of he old

lease, add the costs of the new lease to the

costs of the old lease. - If the old lease has expired, write off the costs

of the old lease and capitalize the cost of the

new lease.

11

Impairment of Assets FASB Statement 144 (2001)

- 1. Conduct impairment review when change in

business environment or way asset is used. - 2. Recognize impairment loss when undiscounted

future cash flows is less than book value of

asset. - 3. Measure the loss by writing down asset to

discounted future cash flows. - 4. If impairment loss is not shown as a line

item in the income statement, must have footnote

disclosure.

12

Impairment of Oil Gas Leases

- Is the property Oil or gas lease impaired???

- Dry holes drilled on lease or surrounding leases?

- Is lease about to expire?

- Are there firm plans for drilling?

- Impairment estimation is difficult and subjective

- Impairment loss is recognized by providing a

valuation allowance

13

Method of Computing Valuation Allowance

- If lease significant, account for valuation

separately - If lease not significant, account for lease along

with other insignificant leases - Significance

- Many companies consider lease significant if

costs exceed 10 - 20 of capitalized costs of

unproved leases - Other companies set dollar amount for

significance - Each WI owner makes the impairment decision

separately

14

Impairment Example Significant Property

(Problem 4-3)

- Green Company has an individually significant

lease with cost of 200,000. Prior to the

issuance of the financial statements, a well on

adjacent property is dry. And lease is determined

to be 40 impaired. - Impairment expense 80,000

- Allowance for impairment 80,000

15

Impairment Insignificant Properties

- Impairment for insignificant properties is

computed for the group - An allowance account for the group is established

- A company may establish more than one group

account, for example, grouping by state - The allowance account works in a manner similar

to a computation of allowance for bad debts from

ACCT 2113 and 3113.

16

Impairment Methods of Computation

- Balance sheet approach determine the amount

that should be the ending account balance and

adjust to get it there - Income statement approach we will omit this one

17

Impairment Example (from p. 97 in text)

- Lucky Company has a policy of providing 60 as an

impairment allowance. 60 of 250,000 150,000 - Allowance account

- 70,000

- _________80,000

- 150,000

- Lease impairment expense 80,000

- Allowance for impairment, Texas 80,000

18

Surrender or Abandonment

- Significant property Surrendered lease expense

is net carrying value of lease (cost less

allowance for impairment) - Insignificant property

- The charge is to allowance for impairment and the

credit is to unproved property - If the allowance account is not large enough,

charge surrendered lease expense for an amount to

bring the allowance account back to zero.

19

Reclassification of an Unproved Property to

Proved Property

- Significant properties Transfer the net amount

to proved property - Example- Lease has an acquisition cost of 100,000

and an allowance for impairment of 25,000 - Proved property 75,000

- Allowance for impairment 25,000

- Unproved property 100,000

20

Reclassification of an Unproved Property to

Proved Property

- Insignificant properties Transfer the full

amount to proved property - Example- Lease has an acquisition cost of

100,000. No specific allowance account. - Proved property 100,000

- Unproved property 100,000

21

Example Problem 4-6

- Lease impairment expense 365,000

- Allowance for impairment, group

365,000 - Allowance for impairment, group 300,000

- Unproved property 300,000

- Proved property 50,000

- Unproved property 50,000

- Unproved property 310,000

- Cash 310,000

- Lease impairment expense 278,000

- Allowance for impairment, group 278,000

- Allowance for impairment, group 428,000

- Unproved property 428,000

- Surrendered lease expense 10,000

Recommended

CrystalGraphics Presentations