Endogeneity in Corporate Governance Studies - PowerPoint PPT Presentation

Title:

Endogeneity in Corporate Governance Studies

Description:

An econometric model for investigating, say, the impact of takeover defense on ... Separation: f1 (Governance, Ownership, Performance, Z1, e1) ... – PowerPoint PPT presentation

Number of Views:56

Avg rating:3.0/5.0

Title: Endogeneity in Corporate Governance Studies

1

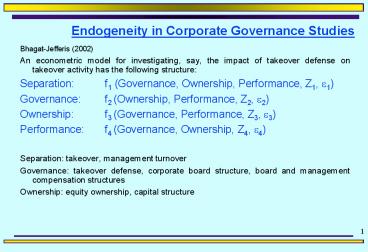

Endogeneity in Corporate Governance Studies

- Bhagat-Jefferis (2002)

- An econometric model for investigating, say, the

impact of takeover defense on takeover activity

has the following structure - Separation f1 (Governance, Ownership,

Performance, Z1, e1) - Governance f2 (Ownership, Performance, Z2, e2)

- Ownership f3 (Governance, Performance, Z3, e3)

- Performance f4 (Governance, Ownership, Z4, e4)

- Separation takeover, management turnover

- Governance takeover defense, corporate board

structure, board and management compensation

structures - Ownership equity ownership, capital structure

2

Endogeneity in Corporate Governance Studies

- Bhagat-Jefferis (2002)

- Identification requires some combination of

exclusion restrictions, assumptions about the

joint distribution of the error terms, and

restrictions on the functional form of the fi. - Maddala (1983) discusses restrictions that

identify the model when the ?i are normally

distributed. - Identification in single equation semiparametric

index models, where the functional form of f1 is

unknown and the explanatory variables in that

equation are continuous, known functions of a

basic parameter vector is discussed by Ichimura

and Lee (1991). - Estimation of a system of the form (1)-(4) in the

absence of strong restrictions on both the fi and

the joint distribution of error terms is, to the

best of our knowledge, an unsolved problem.

3

Endogeneity in Corporate Governance Studies

- Bhagat-Jefferis (2002)

- We are unaware of a model of takeover defense

that implies specific functional forms for the

fi. If these functions are linear,

identification may be attained through either

strong distributional assumptions or exclusion

restrictions. Maddala (1983) and Amemiya (1985)

discuss restrictions on the ?i that identify the

model in the absence of exclusion restrictions.

But these restrictions are inconsistent with

incentive-based explanations of takeover defense,

since unobservable characteristics of managerial

behavior or type will be reflected in all of the

?i. Using panel data and firm-fixed effects it

would be possible to control for unobservable

characteristics of managerial behavior or type

however, a system such as in (1)-(4) would have

to be specified and estimated. Aside from the

non-trivial data collection effort required to

estimate such a system, this system would not be

identified when Z2 Z3 Z4. Exclusion

restrictions are therefore the most likely path

to identification.

4

Endogeneity in Corporate Governance Studies

- Corporate Ownership and Performance

- Diffused share ownership

- Costs Manager-shareholder agency costs

(separation of ownership and control) - Benefits Better risk-bearing

- If the costs of diffused share ownership

dominate - Greater management ownership should lead to

better corporate performance. - However, corporate performance can also have an

impact on management ownership! Why? - Management compensation plans Superior corporate

performance leads to an increase in the value of

stock options owned by management which, if

exercised, would increase their share ownership. - Insider information If there are significant

divergences between insider expectations and

market expectations of future firm performance,

then insiders have an incentive to adjust their

ownership in relation to the expected future

performance. Insider trading is legal subsequent

to earnings/corporate announcements and with

appropriate disclosure.

5

Endogeneity in Corporate Governance Studies

- Corporate Ownership and Performance

- What determines the firms ownership structure?

Ownership may be endogenously determined by the

firms contracting/investment environment. If the

scope for perquisite consumption is low in a

firm, then a low level of management ownership

may be the optimal incentive contract. For firms

with significant growth opportunities, greater

management ownership may be appropriate. - Ownership has an impact on corporate performance.

Also, corporate performance has an impact on

management ownership. - Ownership f3 (Governance, Performance)

- Performance f4 (Governance, Ownership)

6

Endogeneity in Corporate Governance Studies

- Measurement of Corporate Performance

- Market-based measures of performance.

- Industry- and size-adjusted stock returns.

- Anticipation problem.

- Tobins Q (Current market value of the

company/Replacement cost) - Denominator does not reflect cost of intangible

assets. - Numerator includes value of market power.

- Accounting-based measures of performance.

- Return on invested capital. Return on sales.

- Avoids anticipation problem.

- Avoids anticipation problem no credit given for

future sales/growth opportunities. - Some managerial discretion.

Recommended

CrystalGraphics Presentations