Multivariate Linear Regression - PowerPoint PPT Presentation

1 / 31

Title:

Multivariate Linear Regression

Description:

... the multivariate regression model with full rank (Z) = r 1, n r 1 m, and ... Thus the 100(1 a)% confidence interval for the predicted mean value of Y0 ... – PowerPoint PPT presentation

Number of Views:139

Avg rating:3.0/5.0

Title: Multivariate Linear Regression

1

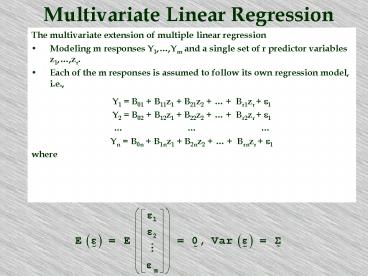

Multivariate Linear Regression

- The multivariate extension of multiple linear

regression - Modeling m responses Y1,,Ym and a single set of

r predictor variables z1,,zr. - Each of the m responses is assumed to follow its

own regression model, i.e., - Y1 B01 B11z1 B21z2 Br1zr e1

- Y2 B02 B12z1 B22z2 Br2zr e1

- Yn B0n B1nz1 B2nz2 Brnzr e1

- where

n

2

Conceptually, we can let zj0, zj1, ,

zjr denote the values of the predictor

variables for the jth trial and

be the responses and errors for the jth trial.

Thus we have an n x (r 1) design matrix

3

If we now set

4

The multivariate linear regression model is

with

and

For example

5

The ordinary least squares estimates b are found

in a manner analogous to the univariate case we

begin by taking

collecting the univariate least squares

estimates yields

Now for any choice of parameters

the resulting matrix of errors is

6

The resulting Error Sums of Squares and

Crossproducts is

We can show that the selection b(i) b(i)

minimizes the ith diagonal sum of squares

generalized variance

i.e.,

are both minimized.

7

so we have matrices of predicted values

and we have a resulting matrices of residuals

Note that the orthogonality conditions which

hold in the univariate case are also true in the

multivariate case

8

which means the residuals are perpendicular to

the columns of the design matrix

and to the predicted values

Furthermore, because

we have

predicted sums of squares and crossproducts

residual (error) sums of squares and crossproducts

total sums of squares and crossproducts

9

Example suppose we had the following six

sample observations on two independent variables

(palatability and texture) and two dependent

variables (purchase intent and overall quality)

How is the multivariate linear regression model

formulated?

10

We wish to estimate Y1 B01 B11z1

B21z2 and Y2 B02 B12z1

B22z2 jointly. The design matrix is

11

so

and

12

and

so

13

and

so

14

so

This gives us estimated values matrix

15

and residuals matrix

Note that each column sums to zero!

16

Inference in Multivariate Regression

The least squares estimators b b(1) b(2)

?b(m) of the multivariate regression model

have the following properties - -

- if the model is of full rank, i.e., rank(Z)

r 1 lt n. Note that e and b are also

uncorrelated.

17

This means that, for any observation z0

is an unbiased estimator, i.e.,

We can also determine from these properties that

the estimation errors

have covariances

k

k

k

k

18

Furthermore

i.e., the forecasted vector Y0 associated with

the values of the predictor variables z0 is an

unbiased estimator of Y0. The forecast errors

have covariance

19

Thus, for the multivariate regression model with

full rank (Z) r 1, n ? r 1 m, and

normally distributed errors e,

is the maximum likelihood estimator of b and

where the elements of S are

20

Test for Ho b(2) 0

Define the Error Sum of Squares and

Crossproducts as E nS and the Hypothesis or

Extra Sum of Squares and Crossproducts as H

n(S1 - S) then we can define Wilks lambda as

where h1 ? h2 ? ? ? hs are the ordered

eigienvalues of HE-1 where s min(p, r - q).

21

There are other similar tests (as we have seen

in our discussion of MANOVA)

Pillais Trace Hotelling-Lawley Trace Roys

Greatest Root

Each of these statistics is an alternative to

Wilks lambda and perform in a very similar

manner (particularly for large sample sizes).

22

Example Regressing palatability and texture

onto purchase intent and overall quality

to test the hypotheses that i) palatability has

no joint relationship with purchase intent and

overall quality and ii) texture has no joint

relationship with purchase intent and overall

quality.

23

We first test the hypothesis that palatability

has no joint relationship with purchase intent

and overall quality, i.e., H0b(1) 0 The

test of this hypothesis is given by the ratio of

generalized variances as given by Wilks lambda

statistic

24

The error sum of squares and crossproducts

matrix is

and the hypothesis sum of squares and

crossproducts matrix for this null hypothesis is

25

so the calculated value of the Wilks lambda

statistic is

26

The transformation to a Chi-square distributed

statistic (which is actually valid only when n

r and n m are both large) is

at a 0.01 and m(r - q) 1 degrees of freedom,

the critical value is 9.210351. Not enough

evidence to reject H0 b(1) 0

27

We next test the hypothesis that texture has no

joint relationship with purchase intent and

overall quality, i.e., H0b(2) 0

The Chi-square transformation yields

Again, not enough evidence to reject H0 b(2) 0

28

We can also build confidence intervals for the

predicted mean value of Y0 associated with z0 -

if the model

has normal errors, then

and

independent

so

29

Thus the 100(1 a) confidence interval for the

predicted mean value of Y0 associated with z0

(bz0) is given by

and the 100(1 a) simultaneous confidence

intervals for the mean value of Yi associated

with z0 (z0 b(i) ) are

i 1,,m

30

Finally, we can build prediction intervals for

the predicted value of Y0 associated with z0

here the prediction error

has normal errors, then

and

independent

so

31

the prediction intervals the 100(1 a)

prediction interval associated with z0 is given by

and the 100(1 a) simultaneous prediction

intervals with z0 are

i 1,,m

Recommended

CrystalGraphics Presentations