Oligopoly - PowerPoint PPT Presentation

Title:

Oligopoly

Description:

Oligopoly Powerpoint produced by Rachel Farrell (PDST) & Aoife Healion (SHS, Tullamore) Sources of information: SEC Marking Scheme Long run equilibrium of a firm in ... – PowerPoint PPT presentation

Number of Views:396

Avg rating:3.0/5.0

Title: Oligopoly

1

Oligopoly

Powerpoint produced by Rachel Farrell (PDST)

Aoife Healion (SHS, Tullamore) Sources of

information SEC Marking Scheme

2

Syllabus

3

Exam Questions (HL)

- Short

- Long

- 2010 Q 4

- 2004 Q 4

- 2002 Q 5

- 2011 Q 2

- 2006 Q 2

- 2003 Q 1

- 1999 Q 2

4

Oligopoly

- Is a market form in which a market or industry is

dominated by a small number of sellers who likely

to be aware of the actions of the others and can

influence price or quantity sold. - Proctor Gamble, Unilever, Tesco..

5

Car manufacturers

6

Examples

- Petrol/Oil Topaz, Esso..

- Motor Ford, Toyota, Nissan

- Retail Banks AIB, BOI

- Supermarkets Tesco, Dunnes

- Detergent Manuf P G. Unilever

7

Assumptions of oligopolies

- 1. Few large firms

- There are a few large firms that dominate the

industry. - They can influence the price or quantity

produced.

8

- 2. Firms interact with each other

- Firms in oligopoy do not act independently of

each other. - They take into account the likely reactions of

their competitors.

9

- 3. Product differention

- Firms sell similar products.

- They engage in competitive advertising.

- They engage in brand marketing.

- They try to convince consumes that their product

is better.

10

- 4. Collusion

Is an agreement among firms to divide the market,

set prices, or limit production. Eg. OPEC

11

5. Firms may pursue objectives other than profit

maximisation

- a) Maximise sales

- Once a certain level of profit has been earned

the firm may concentrate on increasing their

share of the market. - b) Prevent government intervention

- Firms may fear that SNP would attract a

government investigation and restrict their

activities.

12

- 6. There may be barriers to entry into the

industry - Firms may not be able to enter the industry

because of - Economies of scale

- Limit pricing

- Control over the channels of distribution

- Brand proliferation

13

Barriers to Entry

- 1. Economies of Scale

- Large firms produce on a large scale and benefit

form decreased cost per unit . - If a new firm tries to enter the market the

existing firm that is well established can afford

to lower price to deter them. - New firms will be unable to compete due to the

huge set up costs involved.

14

Limit Pricing

- Is an agreement between firms to set a relatively

low price to make it unprofitable for new firms

to enter the industry.

15

Control over the channels of distribution

- Ologopolies may refuse to supply retailers who

stock the products of competitors.

16

Brand Proliferation

- The same firm produces several brands of the same

type of product. - This will leave very little room for new firms to

competitor.

17

Unilever

18

Proctor Gamble

19

Research!!!!

- Look at the household products in your own home

to see what company produces them.

20

Non price competition2010 SQ 4

- Is when competing firms try to increase

sales/market share by methods other than changing

prices.

21

Examples

- Branding To create loyalty and recognition.

- Packaging Distinctive to competitors.

- Competitive advertising Creates difference in

the minds of consumers.

22

- Opening hours Extended, 24/7.

- Quality of service Layout, staff, services.

- Sponsorship Of local or national events.

- Special offers Gifts, coupons, loyalty cards.

23

Benefits of non-price comp to consumers2002 SQ

5/2011 Q 2

- 1. Consumer loyalty rewarded

- Consumers can receive loyalty points which can be

used as they wish. - 2. Stability in prices

- Consumers will be better able to budget as prices

will not always be changing. - 3. Better quality commodities / services

- Firms may offer better service and/ or after

sales service - to consumers.

- 4. More informed consumers

- Through advertising consumers may get more

information about products and services and so

can make more informed choices.

24

Price competition

- Is when competing firms try to increase

sales/market share by changing price.

25

Benefits of price competition to consumers

- 1. Lower prices

- Consumers will be able to get better value from

their limited income. - 2. More choice

- Consumers will have a greater disposable income

and can decide what to spend it on. - 3. Preferable to NPC because

- Special offers of NPC may be unwanted

- Vouchers may be unused.

26

Shape of the demand curve of a firm in oligopoly

- If the price leader sets the price at B then all

firms face a kinked demand curve ABC.

27

Kinked Demand Curve (2011/2006/2003)

Elastic demand curve increase in price, lose

many customers

A

Price

- D AR

P1

B

Inelastic demand curve decrease in price, gain

few customers

C

Q1

Quantity

28

- 1. Along the elastic demand curve above point B,

if a firm increases price it will lose many

customers and revenue. - 2. Along the inelastic demand curve below pon B,

if a firm decreases price so will competitors, so

it will gain few customers but will lose revenue.

29

Relationship between the demand curve and the

marginal revenue curve.

- Because the D/C is kinked the firms MR curve

consists of two distinct parts. - It is constant between D and E.

- Between these points if MC changes, price will

not change.

30

Relationship between the demand curve and the

marginal revenue curve.

A

D AR

Price

P1

B

- D

MR

E

C

Q1

Quantity

31

Price rigidity/Sticky prices

- Prices tend not to change when costs change in

oligoploy. - Firms fear the reaction of their competitors.

- If a firm increase price their competitor will

not, so they will lose customers revenue. - If a firms decrease price so will competitors, so

they will not gain customers and lose revenue.

32

Constant prices

- Firms in oligopoly may not increase prices when

costs increase as it may cost more to change

catalogues and price lists than change the price. - In this case the oligopolist will absorb the

price increase themselves.

33

Long run equilibrium of a firm in oligopoly

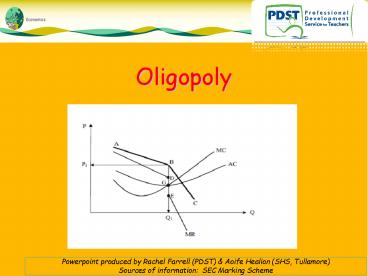

DAR

34

Long run equilibrium of a firm in oligopoly

- Eq is where MCMR MC is rising.

- This occurs at point G on the diagram.

- The firm will produce at Q 1

- The firm will charge price P 1

- Due to barriers to entry firms may earn SNP if AR

gt AC. - Even if costs rise between D E prices remain

rigid at P 1.

35

- Sweezys kinked demand curve explained price

rigidity in the 1930s. - However in the 1970s oligopolies did increase

prices due to oil prices. - In the 1980s oligopolists increased prices due

to increased demand.

36

Question

- Do you believe that the Irish retail market for

banking services operates under oligopolistic

conditions?

37

- Yes

- Few sellers.

- Interdependence between firms

- Close substitutes

- Remember headings, bullet points examples.

Recommended

CrystalGraphics Presentations