Weighted average cost of capital WACC

1 / 18

Title:

Weighted average cost of capital WACC

Description:

15% = company cost of capital, discount rate. Expansion of existing business (same risk as firm) ... rate should Bauer use to discount a project's cash flows if ... – PowerPoint PPT presentation

Number of Views:374

Avg rating:3.0/5.0

Title: Weighted average cost of capital WACC

1

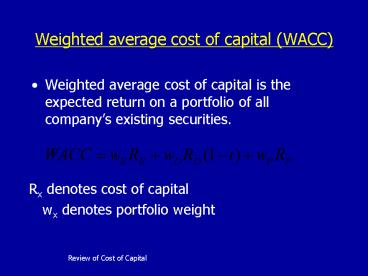

Weighted average cost of capital (WACC)

- Weighted average cost of capital is the expected

return on a portfolio of all companys existing

securities.

Rx denotes cost of capital wx denotes

portfolio weight

2

Weighted average cost of capital

- It is used as a discount rate for capital

budgeting purposes. - A companys cost of capital can be compared to

the CAPM required return

3

CAPM and cost of capital

- For a project

SML

Required return

Cost of capital

Project beta

4

CAPM and cost of capital

- Cost of capital is not always the correct

discount rate. - Only if new project is the same risk as the

firms existing business. - Evaluate NPVs of different projects using the

projects discount rate.

5

What happens if we use cost of capital approach

for projects with more/less risk than the firm?

- For a project

SML

Required return

Incorrectly accept

Cost of capital

Incorrectly reject

Project beta

6

Discount rate should be dependent on risk

7

Why use the cost of capital?

- Most projects are treated as average risk.

- Used as a starting point for riskier/safer

projects.

8

Measuring the cost of equity

- Using CAPM

- Required return rf ß (rm rf)

- Where ß is calculated as

9

Standard error of beta

- A regression model of the CAPM for an individual

firm will give us an estimate of ß, the

coefficient of the market risk premium. - It will also give us a standard error (or

standard deviation) of this estimate.

10

Another measure for cost of equity

- Use the Dividend Growth Model approach (constant

growth model) - Cost of preferred stock

11

Cost of debt

- The cost of debt is the required rate of return

on the firms outstanding debt. - In other words, the yield of maturity.

- Calculate the yield on a companys long term

bonds to find the cost of debt (Rd) - Multiply by (1-t) since interest payments are tax

deductible.

12

Weighted average cost of capital

- Remember,

- The weights are the capital structure market

values divided by total assets - wE Market value of equity (E)/firm value (V)

- wD Market value of debt (D)/firm value (V)

- wP Market value of pref stk (P)/firm value (V)

13

Example

- Bauer, Co. has 8 million shares of common stock

outstanding, .5 million shares of 6 preferred

stock outstanding, and 100,000 9 seminannual

bonds outstanding, par value 1,000 each. The

common stock currently sells for 32 per share

and has a beta of 1.15, the preferred stock

currently sells for 67 per share, and the bonds

have 15 years to maturity and sell for 91 of

par. The market risk premium is 10 and T-bills

are yielding 5. The tax rate is 35.

14

Example

- Calculate Bauers market value capital structure

- What rate should Bauer use to discount a

projects cash flows if the new project has the

same risk as the firms typical project? - Bauer has a prospective investment that is the

same risk as the firms typical project. The

cash flows from the investment are as follows

Year 0 -10,000 Year 1 150,000 Year 2

50,000 Year 3 25,000. Should Bauer accept

the project?

15

Example

- E 8M(32) 256M

- D 100,000(1000)(.91) 91M

- P 500,000(67) 33.5M

- V EDP 380.5M

- E/V .6728, D/V .2392, P/V 0.0880

16

Example

- RE .05 1.15(.10) 16.5

- RD YTM

- on calculator N 30, PV 910, PMT 45, FV

1000. YTM 2(5.092) 10.18 - RP 6/67 8.96

17

Example

- WACC .6728(.1650) .2392(.1018)(1-.35)

.0880(.0896) - 13.47

- This should be used as the discount rate on the

project.

18

Example

- Should the firm accept the project?

- Calculate the NPV of the cash flows using the

WACC as the discount rate.

Recommended

CrystalGraphics Presentations