ShortTerm Financing STCM Chapter 16 ETM Chapter 13 - PowerPoint PPT Presentation

1 / 47

Title:

ShortTerm Financing STCM Chapter 16 ETM Chapter 13

Description:

Common Base Rates. LIBOR. Prime Rate. T - Bill. Credit Ratings. Ratings are issue-specific ... Advances bear interest at prime (currently 7%) plus 2%. ... – PowerPoint PPT presentation

Number of Views:58

Avg rating:3.0/5.0

Title: ShortTerm Financing STCM Chapter 16 ETM Chapter 13

1

Short-Term FinancingSTCM Chapter 16ETM Chapter

13

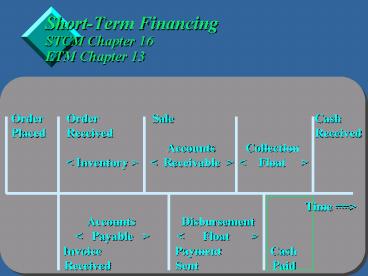

Order Order Sale

Cash Placed Received

Received

Accounts Collection lt

Inventory gt lt Receivable gt lt Float

gt

Time gt Accounts Disbursement

lt Payable gt lt

Float gt Invoice

Payment Cash

Received Sent

Paid

2

Financing and the Cash Flow Timeline

- A deficit cash position may result from the

iteration of inefficient or inappropriate working

capital policies - Management should first evaluate its working

capital policies to ensure the most efficient

stream of cash flow from operations - Strategic Plans can also cause a need for

financing - Balance Sheet Management will help dictate the

financing strategies

3

Overall Borrowing Strategy

- Access to Capital

- Benefits of Using Financial Leverage

- Coordination with Capital Budgeting

4

Financing Strategies

Short-Term

Excess

Liquidity

Financing

Temporary Current Assets

Permanent Current Assets

Long-Term

Financing

Fixed Assets

Time

5

Decisions/Issues to Consider in Borrowing

Strategy

- Source - Debt vs Equity

- Maturity - Short or Long

- Interest Rate Characteristics

- Secured vs Unsecured

- On-and Off-Balance Sheet Financing

6

Short-Term Borrowing Objectives

- Maintaining Availability of Credit

- Optimizing the Cost of Funds

- Minimizing Risk

- Maintaining Flexibility

7

Factors Influencing Financing Costs

8

Loan Pricing

- All-in-RateBase Rate Spread

- Spread and Creditworthiness

- Common Base Rates

- LIBOR

- Prime Rate

- T - Bill

9

Credit Ratings

- Ratings are issue-specific

- Useful tool in evaluating overall

creditworthiness - Incorporates business risk and financial risk

factors - A company pays for the rating service

10

Short-Term Funding Alternatives

- Trade credit

- Internal borrowing

- Asset sales

- Commercial bank credit

- Single payment notes

- Reverse repurchase agreement

- Line of credit

- Revolving credit agreement

- Commercial paper (CP)

- Asset-based borrowing

- Bankers acceptance (BA)

11

Asset Based Loans

- Receivable financing

- Inventory financing

12

Line of Credit

- An agreement between a lender and a borrower in

which the borrower has access to funds up to a

specific amount during a specific period of time.

13

Line of Credit Key Characteristics

- Lender gives access to funds up to a maximum

amount over a specified period - May be committed or uncommitted lines

- Committed obligate the buyer to provide funding

as long as the buyer is not in default - Uncommitted can be cancelled by the lender at any

time - Usually revolving

- May be secured or unsecured

- Usually have a 30- to 60-day cleanup period

14

Effective Rate for Lines of credit

- Out of pocket costs

- Interest expense

- Commitment fee

- Usable funds

- Compensating balance

15

Effective Annual Borrowing Ratefor a Line of

Credit Formula

- Where

- Total interest paid is the all-in rate times the

average loan amount outstanding. - Total fees paid include all commitment fees,

placement fees and any issuance costs. - Average useable loan is the net amount of

borrowed funds available after any compensating

balances are deducted.

16

Effective Annual Borrowing Rate for a Line of

Credit

Example A company wants a 30 million line of

credit with average borrowing to be 20 million.

The bank charges a commitment fee of 0.2 on the

unused portion. Advances bear interest at prime

(currently 7) plus 2. A possible compensating

balance requirement is also shown below.

17

Revolving Credit Agreement

- A facility which allows the borrower to borrow,

repay, and reborrow up to a defined amount. - It is a contractual commitment which includes

covenants, commitment fees, and facilities fees.

18

Commercial Paper

- An unsecured promissory note issued by companies

for a specific amount with maturities ranging

from overnight to 270 days.

19

Commercial Paper (CP) Issuance

20

Commercial Paper Pricing

- Out of pocket costs

- Interest expense

- Line of credit fee

- Dealer underwriting fee

- Remarketing fee

- Usable funds

- Discounted price (Face value less interest)

- Dealer spread

21

Effective Annual Interest Cost for Commercial

Paper (CP)

Example A company wants 10 million commercial

paper issue . The dealer charges a fee of 0.1 .

The bank providing a letter of credit wants a

fee of .2.The Commercial Paper is utilized for

60 days. The Commercial Paper is sold at a

discount rate of 4.2.

Part 1 of 2

22

Effective Annual Interest Cost for Commercial

Paper (CP)

Example A company wants 10 million commercial

paper issue . The dealer charges a fee of 0.1 .

The bank providing a letter of credit wants a

fee of .2.The Commercial Paper is utilized for

60 days. The Commercial Paper is sold at a

discount rate of 4.2.

Part 2 of 2

23

Letter of Credit

- Substitutes the credit of a financial institution

for that of the borrower - Financial institution guarantees payment to the

seller and then collects from the borrower

24

Bankers Acceptance (BA)

- A negotiated short-term instrument used primarily

to finance the import, export or domestic

shipment of goods or the storage of readily

marketable staples.

25

Key Characteristic of BAs

- It is a time draft accepted by a bank.

- The BA is the direct obligation of the accepting

bank. - The credit rating of the accepting bank backs the

BA. - A BA is a marketable instrument.

- A BA is a discount instrument.

26

Asset-Backed Borrowing

- A secured form of lending based on the pledging

of A/R or inventory as collateral for the loan.

27

Types of Asset-Backed Borrowing

- A/R

- Inventory

- Floor Planning

- Factoring

28

Accounts Receivable

- Collateralized over 100

- Payments by customers made directly to lender

- Lender does not own the receivables

29

Inventory

- Collateralized over 100

- Finished Goods or Raw Materials

30

Floor Planning

- High Cost Goods (Autos, Appliances)

- Lender takes title to the goods

- Loans are repaid when the goods are sold

31

Securitization

- Financing technique in which a company issues

debt securities backed by a pool of selected

financial assets.

32

Key Characteristics of Securitization

- Off-balance sheet financing

- Helps improve the balance sheet by reducing

leverage - Issues are credit enhanced

33

Credit Enhancement Methods for Securitization

- Over-collateralization

- Letter of Credit

- Spread Accounts

34

Securitization

Acme Corp

Auto Loans 8 5 years 10M

Subsidiary (off balance sheet) 9.5M

35

Securitization

Acme Corp

Cash

Investors

Auto Loans 8 5 years 10M

Subsidiary (off balance sheet) 9.5M

Asset backed securities

4 3yr 4M

2 1yr 2.3M

6 5yr 3.2M

36

Acme Corp

Securitization

Cash

Investors

Auto Loans 8 5 years 10M

Borrowers 11.5M

Subsidiary (off balance sheet) 9.5M

Asset backed securities

Repay loans

4 3yr 4M

2 1yr 2.3M

6 5yr 3.2M

37

Securitization

Acme Corp

Cash

Investors

Auto Loans 8 5 years 10M

Borrowers 11.5M

Subsidiary (off balance sheet) 9.5M

Asset backed securities

Repay loans

Acme Corp 1M

4 3yr 4M

2 1yr 2.3M

6 5yr 3.2M

Residuals

38

Medium and Long-Term Borrowing Alternatives

- Medium Term Notes

- Bonds

- Debt-Equity Hybrids

- Term Loans

- Leasing

- Private Placement

39

Private Placement

- Is a direct sale of securities by a company to

institutional investors. - Securities are not registered with the SEC.

- May offer longer or more flexible terms than term

loans. - Less costly to arrange than for public debt

issues.

40

Reasons Private Placement is Preferred Over

Public Issuance

- Less restrictive covenants

- The size of the issue

- The reduced time and number of parties involved

- The complexity of the securities

- A desire for minimal reporting, agency ratings or

public disclosure - Lower costs

- Control over who holds the debt

41

Debt (Bond) Capital Markets

- Use of short- and long-term debt usually results

in lower overall cost of capital and an increase

in cash flows per dollar of equity due to - Generally lower cost of debt (vs. equity)

- Tax deductibility of interest payments

- Fixed nature of debt payments

- Profitable companies favor debt

- Payments limited to principal/interest

- Risk of insufficient cash flows

- Additional borrowing or possible default or

bankruptcy

42

Long-Term Bonds (1 of 2)

43

Long-Term Bonds (2 of 2)

44

Key Characteristics of Bonds

- Bonds are administered through a trustee.

- Bonds can be secured versus unsecured.

- Bonds can be classified as senior or subordinate.

- Bonds have call features.

- Secured bondholders have priority claim in

liquidation. - Ratings

45

Issuance of Bonds

- Competetive or Negotiated

- Hire a Financial Advisor or Underwriter(s).

- Hire Bond Counsel.

- Create Documents including Official Statement

(OS). - Apply for Ratings.

- Finalize Structure and issuance date.

- Marketing and Order Period.

- Sale.

- Closing.

46

Leasing

- An alternative to term lending for financing

equipment purchases. - Typically 100 of the equipment cost can be

financed. - A capital lease is an on-balance sheet

transaction. - An operating lease is an off-balance sheet

transaction. - Tax advantages exists for the lessor and the

lessee

47

Types of Leases

- Sale and leaseback

- Operating or service leases

- Lessor maintains, retains asset at end

- Often OBSA

- Shorter duration than life of asset

- Capital or financial leases

- gt 1 yr., not cancelable, fully depreciate list

on balance sheet as a capitalized lease - Lessor does not maintain

- Lease runs for life of asset lessee can purchase

or renew contract at end

Recommended

CrystalGraphics Presentations