An Application of MultiObjective Optimization to - PowerPoint PPT Presentation

1 / 1

Title:

An Application of MultiObjective Optimization to

Description:

Every investor is faced with a risk-return tradeoff when allocating their funds ... preference; two particular assets must never fall below a given parameter (20 ... – PowerPoint PPT presentation

Number of Views:49

Avg rating:3.0/5.0

Title: An Application of MultiObjective Optimization to

1

An Application of Multi-Objective Optimization to

Portfolio Optimization Erica D. Parker,

Operations Research, North Carolina State

University, Raleigh NC 27695, edparker_at_ncsu.edu

Introduction Every investor is faced with a

risk-return tradeoff when allocating their funds

into various stocks and securities. Because

there are several patterns in which stocks tend

to follow (i.e. moving together, moving in

opposite directions, and not having any relation

to one another at all), investing is essentially

a case of trial and error. However, through the

utilization of mathematical models and

probabilistic rules, investing may not have to

be.

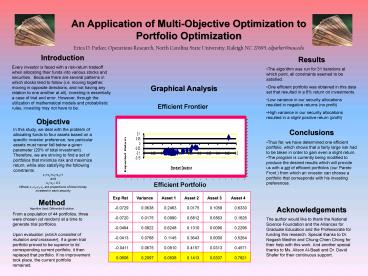

- Results

- The algorithm was run for 31 iterations at which

point, all constraints seemed to be satisfied. - One efficient portfolio was obtained in this data

set that resulted in a 6 return on investments. - Low variance in our security allocations resulted

in negative returns (no profit) - High variance in our security allocations

resulted in a slight positive return (profit)

Graphical Analysis

Efficient Frontier

Objective In this study, we deal with the problem

of allocating funds to four assets based on a

specific investor preference two particular

assets must never fall below a given parameter

(20 of total investment). Therefore, we are

striving to find a set of portfolios that

minimize risk and maximize return, while also

satisfying the following constraints x1x2x3x4

1 and x1x2 0.2 Where x1,x2,x3,x4 are

proportions of total money invested in each

security

- Conclusions

- Thus far, we have determined one efficient

portfolio, which shows that a fairly large risk

had to be taken in order to gain even a slight

return. - The program is currently being modified to

produce the desired results which will provide us

with a set of efficient portfolios (our Pareto

Front ) from which an investor can choose a

portfolio that corresponds with his investing

preferences.

Efficient Portfolio

- Method

- Algorithm Used Differential Evolution

- From a population of 44 portfolios, three were

chosen (at random) at a time to generate trial

portfolios. - Upon evaluation (which consisted of mutation and

crossover), if a given trial portfolio proved to

be superior to its corresponding current

portfolio, it then replaced that portfolio. If no

improvement took place, the current portfolio

remained.

Acknowledgements The author would like to thank

the National Science Foundation and the Alliances

for Graduate Education and the Professorate for

funding this research. Special thanks to Dr.

Negash Medhin and Chung-Chien Chong for their

help with this work. And another special thanks

to Ms. Alison Al-Baati and Dr. David Shafer for

their continuous support.

Recommended

CrystalGraphics Presentations