Usage challenge: the iceberg effect - PowerPoint PPT Presentation

1 / 10

Title:

Usage challenge: the iceberg effect

Description:

Revenues threatened by multiple alternatives and technology disruptions. TELEPHONY ... from SK Telecom's acquisition of Cyworld and BT's failed acquisition of Bebo ... – PowerPoint PPT presentation

Number of Views:34

Avg rating:3.0/5.0

Title: Usage challenge: the iceberg effect

1

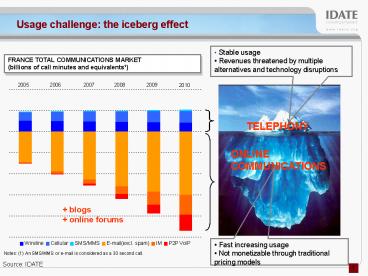

Usage challenge the iceberg effect

- Stable usage

- Revenues threatened by multiple alternatives and

technology disruptions

FRANCE TOTAL COMMUNICATIONS MARKET (billions of

call minutes and equivalents¹)

2005

2006

2007

2008

2009

2010

TELEPHONY

ONLINE COMMUNICATIONS

blogs online forums

- Fast increasing usage

- Not monetizable through traditional pricing

models

Notes (1) An SMS/MMS or e-mail is considered as

a 30 second call.

Source IDATE

2

The growth challenge the wireline market is

stagnating

Fixed line loss is generalizing across Western

Europe

resulting in high deflationary pressure

on wireline voice

EU 5 fixed voice market 01-06 evolution (bn)

EU 5 fixed line net adds (000s)

while usage is declining under fixed mobile

substitution

barely compensated by broadband growth

Outgoing call minutes per year in France (billion

minutes)

EU 5 fixed services market evolution (bn )

3

Next generation carriers will achieve agility

through increased specialization

Market approach

Strategic imperatives for ROIC optimization

Likely candidates

Revenues

Value added application provider

Primarily allocating resources to the

proliferation of applications targeting niches

and short-lived opportunities to increase

customer base and/or revenue per customer.

Network no longer considered a strategic asset

and outsourced to reduce invested capital base.

1

Customers services

3

1

Enhanced connectivity provider

Maximizing utilization of best-of-breed network

to enable economies of scale, at the lowest

possible cost per Mb provisioned. Revenues

generated from leased capacity of enhanced

connectivity. End user service creation and

commercialization left to 3rd party providers.

Converged services integrated operator

2

Value added application provider

Converged services integrated operator

2

Enhanced connectivity provider

Network

Operations

Converged services integrated operator

Leveraging owned fixed and mobile networks to

offer truly converged and seamless

multimedia-rich premium services in addition to

over the top content.. Incremental revenues by

targeting the premium digital content opportunity

and tight cost control through converged IP

network architectures.

3

Opex

Invested capital

4

Network outsourcing is becoming a real strategic

option

subscribers /network at time of outsourcing

750 employees transferred

Ned 150 employees transferred

12M

10M

Tipping point

UK 1000 employees

Europe excl. UK Spare parts mgt for 2G, 3G

transmission

4M

Italy 750 employees transferred

3M

Global services Maintenance spare parts mgt

200 employees transferred

2M

300 employees

1M

50 employees

Switz.

Maintenance

3G Network

2002

2003

2004

2005

2006

2007

MAINTENANCE

ACCESSCORE

ACCESS

5

but is only a fraction of an overall operations

transformation

Network outsourcing

Operations transformation

Operational complexity

6

Separation questions

Where is network separated?

- Which part will keep the risk?

- Will it stop the alternates investments?

- Is it the end of the infrastructure based

competition?

- Which part will keep the risk?

- Is it the end of the infrastructure based

competition ?

7

Separation v. Consolidation TI TEF

- Brazilian regulator restrictions?

- Level of synergiesTI-TEF?

- Structure of power

- Portfolio changes

TIs new shareholding structure

8

Next generation carriers will achieve agility

through increased specialization

Market approach

Strategic imperatives for ROIC optimization

Likely candidates

Revenues

Value added application provider

Primarily allocating resources to the

proliferation of applications targeting niches

and short-lived opportunities to increase

customer base and/or revenue per customer.

Network no longer considered a strategic asset

and outsourced to reduce invested capital base.

1

Customers services

3

1

Enhanced connectivity provider

Maximizing utilization of best-of-breed network

to enable economies of scale, at the lowest

possible cost per Mb provisioned. Revenues

generated from leased capacity of enhanced

connectivity. End user service creation and

commercialization left to 3rd party providers.

Converged services integrated operator

2

Value added application provider

Converged services integrated operator

2

Enhanced connectivity provider

Network

Operations

Converged services integrated operator

Leveraging owned fixed and mobile networks to

offer truly converged and seamless

multimedia-rich premium services in addition to

over the top content.. Incremental revenues by

targeting the premium digital content opportunity

and tight cost control through converged IP

network architectures.

3

Opex

Invested capital

9

Engaged in this cross-industry battle, carriers

have overlooked the threat posed by new entrants

on their core market.

Communications account for a substantial proportio

n of online usage

yet carriers are struggling to innovate and be

competitive in this space

Competition dynamics

Carrier strategies

Share of time spent online

- Continue to bundle with internet access

- Match webmail providers innovations to limit

their market share

USA

Instant Messaging

- After trying to push their own solutions,

carriers are now partnering with leading IM

providers

Worldwide

Blogs

- Still dominated by independent companies but

consolidating

- Isolated initiatives to transform the homepage

activitiy

- Consolidation by media companies

- No significant initiative apart from SK

Telecoms acquisition of Cyworld and BTs failed

acquisition of Bebo

Social networks/ online forums

Communications account for nearly 40 of time

spent online

Source Online Publishers Association, Comscore

Hitwise, IDATE

10

PURE COMBINED STRATEGIES

Horizontal concentration

- Domestic

- Pan-European

- Development economies

Vertical integration

- Networks-contents-services

- Wholesale retail

- Access WW Web infrastructure player

Specialization

- Pure Mobile V. FMC

- Wholesale v. Retail

- MVNO FVNO

- Business v. Consumers

Execution

- Winners

- Losers

?

Source IDATE

Recommended

CrystalGraphics Presentations