New Auditing Standards: How they impact YOU! - PowerPoint PPT Presentation

1 / 6

Title:

New Auditing Standards: How they impact YOU!

Description:

Auditors will look at documentation, will recreate a transaction, will interview departments ... Auditors may talk to more departments to gather information. ... – PowerPoint PPT presentation

Number of Views:21

Avg rating:3.0/5.0

Title: New Auditing Standards: How they impact YOU!

1

New Auditing Standards How they impact YOU!

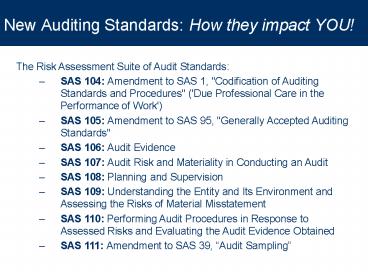

- The Risk Assessment Suite of Audit Standards

- SAS 104 Amendment to SAS 1, "Codification of

Auditing Standards and Procedures" ('Due

Professional Care in the Performance of Work') - SAS 105 Amendment to SAS 95, "Generally Accepted

Auditing Standards" - SAS 106 Audit Evidence

- SAS 107 Audit Risk and Materiality in Conducting

an Audit - SAS 108 Planning and Supervision

- SAS 109 Understanding the Entity and Its

Environment and Assessing the Risks of Material

Misstatement - SAS 110 Performing Audit Procedures in Response

to Assessed Risks and Evaluating the Audit

Evidence Obtained - SAS 111 Amendment to SAS 39, Audit Sampling

2

Key Control Evaluation

- Key control those that are most effective and

reliable in preventing or detecting material

misstatements. - Often includes actions of supervisors and

business managers - Examples reconciliations, follow up on exception

reports, budget to actual analysis, proper access

to information systems.

3

Key Control Evaluation

- Does the controls prevent or detect errors?

- Ownership Comptrollers Office

- Are departments actually using the control?

- Ownership Departments

- Auditors will look at documentation, will

recreate a transaction, will interview departments

4

Processes

- Auditors will focus less on financial statement

balances and more of the processes leading to

those balances. - Auditors may interview you to learn about

internal controls that you have in place. - Auditors may interview you to learn where

existing documentation of controls, such as

policies, reside. - Auditors may look at your transactions to see if

they were carried out as dictated in the policy.

5

Sampling of Transactions

- Auditors may look at more transactions than they

have in the past. - Auditors may look at transactions in process

areas that they have not examined in the recent

past. - Auditors may talk to more departments to gather

information. - If you cant prove it, it didnt happen.

6

Impacts to NAU

- Identify areas for improvement of key business

processes and internal controls. (policy

improvement, better monitoring) - Provides documentation for accountability to ABOR

- Can impact bond ratings

- Can be basis for Internal Audit plans and

Financial Controls reviews

Recommended

CrystalGraphics Presentations