XYZ Inc - PowerPoint PPT Presentation

1 / 22

Title:

XYZ Inc

Description:

120k boot paid by XYZ Inc in addition to stock, Jim would recognize gain equal ... Basis in stock would equal 100k plus 100k gain less 120k boot = 80k basis. ... – PowerPoint PPT presentation

Number of Views:84

Avg rating:3.0/5.0

Title: XYZ Inc

1

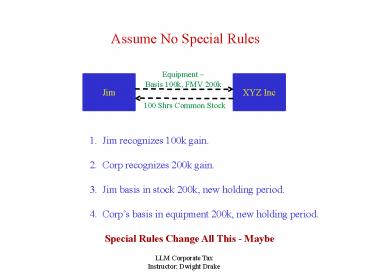

Assume No Special Rules

Equipment Basis 100k, FMV 200k

XYZ Inc

Jim

100 Shrs Common Stock

1. Jim recognizes 100k gain. 2. Corp

recognizes 200k gain. 3. Jim basis in stock

200k, new holding period. 4. Corps basis in

equipment 200k, new holding period.

Special Rules Change All This - Maybe

2

Rule 1 351 Rule

Equipment Basis 100k, FMV 200k

XYZ Inc

Jim

100 Shrs Common Stock

No gain or loss is recognized by the

transferor on the transfer of property to a

corporation in exchange for stock of the

corporation if 1. Property is

transferred 2. Solely in exchange

for stock 3. Transferor(s) in

control immediately after exchange. Two

80 requirements 80 of all voting stock and

80 of total shares of each other class of

stock. Result Jim recognizes no gain or

loss on the exchange.

3

Rule 2 351(b) Boot Rule

Equipment Basis 100k, FMV 200k

Jim

XYZ Inc

Common Stock Cash

If 351 would apply except that corporation issues

property in addition to stock (boot) to the

shareholder, then shareholder recognizes

gain on the property transferred to corporation

equal to the lesser of 1. The

built-in gain on the property transferred the

excess of FMV over basis

2. The FMV of boot received by the

shareholder. Result If 80k cash boot, Jim

recognizes gain equal to boot 80k. If 120k

boot paid by XYZ Inc in addition to stock, Jim

would recognize gain equal to 100k

excess of 200k FMV over 100k basis.

4

Rule 3 The 358 Basis Rule

Equipment Basis 100k, FMV 200k

Jim

XYZ Inc

Common Stock Cash

If 351 applies to an exchange of

property for stock in a corporation, the basis of

the stock received by the shareholder equals

1. The basis of the property

transferred to the corporation in the hands of

the shareholder, plus 2. Any gain

recognized by shareholder ala the 351(b) rule,

less 3. The FMV of any boot

received. Result If XYZ Inc issues

100 share of its stock and 80k cash, Jim

recognizes gain equal to boot 80k, and Jims

basis in stock is equal to 100k (basis in

equipment), plus 80k gain less 80k boot 100k.

If 120k boot was paid by XYZ Inc in

addition to stock, Jim would recognize gain equal

to 100k. Basis in stock would equal 100k plus

100k gain less 120k boot 80k basis.

5

Rule 4 Shareholder Tacking Rule

Equipment Basis 100k, FMV 200k

Jim

XYZ Inc

Common Stock Cash

If 351 applies to an exchange of property

for stock in a corporation, the holding period of

the property transferred by the shareholder is

tacked on to the holding period of the stock if

the transferred property was a capital asset or a

1231 asset (asset used in trade or business). No

inventories or receivables.

Result Jims holding period of equipment is

tacked on in determining holding period of

stock.

6

Rule 5 The 1032 Rule

Equipment Basis 100k, FMV 200k

Jim

XYZ Inc

Common Stock Cash

Corporation recognizes no gain or loss on

receipt of money or property in exchange for its

own stock Result XYZ Inc issues 100

share of its stock and 80k cash to its sole

shareholder Jim for equipment worth 200k that has

a basis of 100k. XYZ Inc recognizes no gain or

loss.

7

Rule 6 The 362 Rule

Equipment Basis 100k, FMV 200k

Jim

XYZ Inc

Common Stock Cash

A corporations basis in property

acquired in exchange for its stock in a

transaction that qualifies under 351 equals the

shareholders basis in the property basis plus

any gain recognized by the shareholder. But if

net built-in loss, basis limited to FMV of

property unless all elect to reduce stock basis

of shareholder to FMV. Result XYZ Inc

issues 100 share of its stock and 80k cash to

Jim, Jim recognizes gain equal to boot 80k.

XYZ Inc.s basis in equipment is equal to 100k

(Jims basis in equipment), plus 80k gain

recognized by Jim 180K.

8

Rule 7 Corporate Tacking Rule

Equipment Basis 100k, FMV 200k

Jim

XYZ Inc

Common Stock Cash

If 351 applies to an exchange of property

for stock in a corporation, the holding period of

the property transferred by the shareholder is

tacked on in determining the holding period of

the property in the hand of the corporation.

Result Jims holding period of equipment is

tacked on in determining XYZ Inc.s holding

period of equipment.

9

Problem 64(a)

25k Cash / 25 Shares

Note / 20 Shares

X Corp

Inventory / 10 Shares

Equip. / 25 Shares

Land / 20 Shares

A

B

C

D

E

FMV -10k Basis 5k

FMV - 20k Basis 25k

FMV - 25k Basis 5k

FMV - 20k Basis 2k

- 351 requirements satisfied. Hence

- A No gain or loss. Stock basis 25k.

Holding period starts on exchange. - B No gain recognized Stock basis 5k

no tacking holding period. - C No loss recognition Stock basis

25k tacking holding period. - D No gain recognition Stock basis 5k

tacking holding period. - E No gain recognition Stock basis 2k

tacking holding period.

10

Problem 64(b)

25k Cash / 25 Shares

Note / 20 Shares

X Corp

Inventory / 10 Shares

Equip. / 25 Shares

Land / 20 Shares

A

B

C

D

E

FMV -10k Basis 5k

FMV - 20k Basis 25k

FMV - 25k Basis 5k

FMV - 20k Basis 2k

(b) Per 1032, X Corp recognizes no income on

issuance of stock. X takes transferred basis in

each asset (except land) and may tack holding

period per 1223(2). Tacking is irrelevant to

inventory, as it will be ordinary income or loss.

Land 5k built-in loss forces basis reduction to

FMV 20k per 362(e)(2)(A), unless C agrees to

stock basis reduction to 20k.

11

Problem 64(c) (d)

25k Cash / 25 Shares

Note / 20 Shares

X Corp

Inventory / 10 Shares

Equip. / 25 Shares

Two 10k Parcels / 20 Shares

A

B

C

D

E

FMV -10k Basis 5k

1 15k Basis 2 8k Basis

FMV - 25k Basis 5k

FMV - 20k Basis 2k

c) Two land parcels from C each 10k FMV

(20k total) and 23k combined basis (15k and 8k).

May net built-in gains with built-in losses in

applying basis adjustment of 362(e)(2)(A). Thus

only 3k basis reduction, all allocated to

built-in loss parcel, reducing its basis to 12k.

As option, C could elect to take 3k basis

reduction. d) What impact if X corp sells

inventory for 10k and B sells stock for 10k.

Both recognize 5k gain on inventory appreciation.

Thus, double tax inherent in 351 carryover

non-recognition impact. Note S Corp impact where

shareholder basis is increased by S Corp income.

12

Problem 73-1 (a) (b)

Newco

Property / 10 Shares Preferred

Property / 50 Shares

Jan 2

March 2

A

B

FMV - 50k Basis 10k

FMV - 10k Basis 1k

(a) A transfer qualifies under 351 A has no

gain or loss A stock basis 10k tack holding

period if asset was capital asset or 1231 Newco

no gain or loss Newco takes basis of 10k in

property. B transfer not qualify under 351 B

sole transferor and no voting stock. B

recognizes 9k gain Stock basis is 10k Newco no

gain or loss Newco basis in asset is 10k. (b)

If both part of integrated transaction, 351

applies to both A B are both transferors and

together own all voting and non-voting stock.

Requirement of immediately after exchange does

not require simultaneous transfers.

13

Problem 73-1 (c)

Newco

Property / 10 Shares Preferred

Property / 50 Shares

Jan 2

March 2

A

B

D

March 5

25 Share Gift

FMV - 50k Basis 10k

FMV - 10k Basis 1k

(c) A gift of half voting shares after

integrated transfers should not impact 351

treatment for A B. If gift on 1/5, between

integrated exchanges, 351 is killed because not

own voting control after transfers.

14

Problem 73-1 (d)

Newco

Property / 10 Shares Preferred

Property / 50 Shares

Jan 2

March 2

A

B

E

May 2

15 Share Sale

FMV - 50k Basis 10k

FMV - 10k Basis 1k

(d) Pre-existing promise to sale stock kills

351. E is not a transferor under 351, but is

part of the plan.

15

Problem 73- 2 (a) (b)

Jyve Inc.

Assets / 200 Shares

5 Yr. Employment / 150 Shares

Cash/ 150 Shares

Java

Manager

Venturer

FMV - 200k Basis 50k

150 k Cash

- 351 requirements not satisfied services not

property for 351 and Java and Venturer (the

property contributors) do not have control.

Java recognizes 150k gain on incorporation, and

Manager has compensation income equal to FMV of

stock received as much as 150k. - If Manager pays 150k for stock - 351 then works.

Note from manager may also qualify as property,

but many state laws prohibit unsecured note for

stock. May need to secure note with escrowed

stock.

16

Problem 73- 2 (c) (d)

Jyve Inc.

Assets / 200 Shares

5 Yr. Employment Plus Cash for 150 Shares

Cash/ 150 Shares

Java

Manager

Venturer

FMV - 200k Basis 50k

150 k Cash

c) Idea Manager pays 1k for 150 shares

of stock and documents say services of manager

not consideration for stock. No hope under 351.

Substance will prevail. Stock will still be

deemed for services because property is of

relatively small value compared to services.

d) Manager pays 20k for stock? Since

property transferred exceeds 10 of shares for

services, not relatively small value per Rev.

Proc. 77-37 and 351 available. This helps Java

big time, but Manager still must recognize 130k

on receipt of compensation-related shares.

17

Problem 73- 2 (e)

Jyve Inc.

5 Yr. Employment Plus Cash for 150 Shares

130 Subject to Risk

Assets / 200 Shares

Cash/ 150 Shares

Java

Manager

Venturer

FMV - 200k Basis 50k

150 k Cash

e) What impact if compensation related shares

subject to forfeiture if Manager leaves within 5

years? Per Section 83, Manager not recognize

until restriction lapse, but then recognize full

FMV as ordinary income. 83(b) election allows

recognition now, against risk of forfeiture and

potential of more favorable capital gain

treatment on growth.

18

Compensation Gross-Up Game

Assume 1. Stock for services equal 150k

2. Corporation tax rate 34 3.

Executive tax rate 33 Straight recognition

transaction - Executive pays

taxes of 50k - 33 of 150k. -

Corporation saves taxes of 51k 34 of 150k

Gross up amount formula

Stock value / (1 - Executive tax rate)

Stock value Gross-Up Tax Bonus

150k / (1 - .33 .67) 150k 74k

- Corp tax savings (150k 74k) x 34

76k (More than Gross-up) - Employee

tax bill (150k 74k) x 33 74k (Paid by

Gross-up)

19

Problem 83 (a)

X Corp.

15k common 2k Cash 5k Pf

10k Common 5k Cash 35k Note

15k Common 15k Cash

A

C

B

22k Equip Basis -15k

50k Land Basis -20k

Inv 20k, Land 10k Basis 7k Inv, 25k Land

- A 2k boot 1245 ordinary income Stock basis 15k

75 common, 25 preferred holding period

tacked X basis is 17k X may tack holding

period. - B 15k boot allocated 10k inv, 5k land

recognize 10k ordinary on inv, no loss

recognition land B Stock basis is 27k (32k

15k(boot) gain recognized(10K)) 1/3 stock

tack, 2/3 not. X basis inv is 17k (7k 10k),

land 23k (25k less 2k aggregate built-in loss).

20

Problem 83 (a)

X Corp.

15k common 2k Cash 5k Pf

10k Common 5k Cash 35k Note

15k Common 15k Cash

A

C

B

22k Equip Basis -15k

50k Land Basis -20k

Inv 20k, Land 10k Basis 7k Inv, 25k Land

(a) C 40k boot 30k gain recognized If no

453(d) elect out, C could use installment. 10k

basis allocated to stock other to 40k note and

cash, with 25 (10k/40k) recovery ration. Of 5k

cash, 3.75 recognized yr one 75 of all future

payments taxable. C stock basis is 20k start

30k gain recognized 40k boot received 10k. X

Corp land basis is 20k start 3.75 yr 1 gain and

increased as more payments received ultimately

to 50k.

21

Problem 83 (a) Calculation for C

(a) C - Detailed installment sales

calculations - Transferred basis

(20K) first allocated to permitted property

the stock up to FMV here 10k. Prop. Reg.

1.453-1(f)(3)(iii). - Excess 10k

transferred basis is allocated to boot 5k cash

and 35k note. Total boot of 40k, against basis

of 10k, and gain of 30k. Thus, ratio of profit

to total boot is 30/40 75. -

First year payment of 5k produce 3.75 income (5k

x .75) - C basis under 358

determined without regard to 453 installment

reporting. Hence is 20k transfer 30k gain

40k boot 10k. - X Corp basis

does use 453 installment. Hence, year 1 is 20k

3.75k 23.75k. Will eventually get to

50k as installment not paid.

22

Problem 83 (b)

X Corp.

15k common 2k Cash 5k Pf

10k Common 5k Cash 35k Note

15k Common 15k Cash

A

C

B

22k Equip Basis -15k

50k Equipment Basis -20k

Inv 20k, Land 10k Basis 7k Inv, 25k Land

(b) C instead transfers equipment with 50k FMV

and 20k basis. Original cost 50k. All 30 income

recognized as 1245 ordinary income, with no 453

installment reporting available. C stock basis

is 10k. X Corp basis in equipment is 20k 30k

gain recognized 50k.

Recommended

CrystalGraphics Presentations

![[PDF]❤READ⚡ Rowe v. Pacific Quad, Inc.: Deposition File, Defendant's Materials (NITA) 6th Editi PowerPoint PPT Presentation](https://s3.amazonaws.com/images.powershow.com/10063482.th0.jpg?_=20240625011)

![[READ]⚡PDF✔ Rowe v. Pacific Quad, Inc.: Deposition File, Plaintiff''s Materials (NITA) 6th Edit PowerPoint PPT Presentation](https://s3.amazonaws.com/images.powershow.com/10063483.th0.jpg?_=20240625011)

![[READ] beekyoo space Kismet Score Sheets - 130 Large Score Sheets for Kismet Game, 8.5 x 11 Inc PowerPoint PPT Presentation](https://s3.amazonaws.com/images.powershow.com/10056745.th0.jpg?_=202406160810)

![[READ] beekyoo space Kismet Score Sheets - 130 Large Score Sheets for Kismet Game, 8.5 x 11 Inc PowerPoint PPT Presentation](https://s3.amazonaws.com/images.powershow.com/10056606.th0.jpg?_=20240616075)

![download⚡[PDF]❤ Schlesinger's Comparative Law: Cases, Text, Materials, 7th Edition (University PowerPoint PPT Presentation](https://s3.amazonaws.com/images.powershow.com/10067865.th0.jpg?_=20240628097)

![[PDF]❤READ⚡ Playing Up: One Man's Rise From Public Housing To Public Service Through Mentorship PowerPoint PPT Presentation](https://s3.amazonaws.com/images.powershow.com/10061564.th0.jpg?_=202406221210)