Early 1970s - PowerPoint PPT Presentation

1 / 22

Title:

Early 1970s

Description:

Consistency Must Be Achieved Across GROUNDS! ... CAS Consistency! CAS: ... Standard #9905.501: 'Consistency in estimating, accumulating, and reporting ... – PowerPoint PPT presentation

Number of Views:51

Avg rating:3.0/5.0

Title: Early 1970s

1

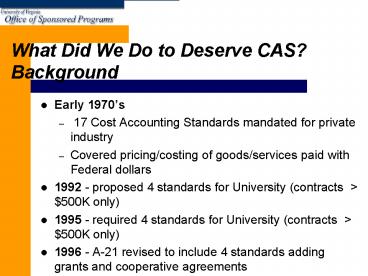

What Did We Do to Deserve CAS? Background

- Early 1970s

- 17 Cost Accounting Standards mandated for

private industry - Covered pricing/costing of goods/services paid

with Federal dollars - 1992 - proposed 4 standards for University

(contracts gt 500K only) - 1995 - required 4 standards for University

(contracts gt 500K only) - 1996 - A-21 revised to include 4 standards adding

grants and cooperative agreements

2

Types of Awards and Applicable Guidance

- Three main types of awards with unique

characteristics - Grant -

- Contract -

- Cooperative Agreement -

3

CAS The Basic Philosophy

- CONSISTENCY ..

- In the budgeting, charging and reporting of costs

on Federal sponsored awards. - Consistency Must Be Achieved Across GROUNDS!!!

4

CAS Costing Basics

CAS Federal Regulations are included in the

Office of Management and Budgets Circular A-21

Cost Principles for Educational Institutions

in - Section C.10-14 - Exhibit C Major

Projects - Appendix A - Standards

- 1. Dont charge the Government twice for the

same cost. - (Direct Costs versus Facilities Administrative

Costs) - 2. Dont charge the government for any

expressly unallowable costs. - Philosophy of CAS Consistency!

5

CASFour Standards Applicable to Educational

Institutions

- Standard 9905.501 Consistency in estimating,

accumulating, and reporting costs by educational

institutions. - In other words

- All costs 1) initially used in budgeting

proposals, 2) subsequently included in

charging/assigning costs to sponsored awards and

finally 3) included in the reporting to sponsors

are treated consistently as either direct or FA

costs in like circumstances.

6

CASFour Standards Applicable to Educational

Institutions

- Standard 9905.502 Consistency in allocating

costs incurred for the same purpose by

educational institutions. - In other words

- All costs incurred for the same purposes are

either direct costs only or facilities and

administrative (indirect) costs only.

7

CASFour Standards Applicable to Educational

Institutions

- Standard 9905.505 Accounting for unallowable

costs Educational Institutions - In other words

- Any costs considered as unallowable by

provisions of any law, regulation or sponsored

agreement cannot be included in the pricing, cost

reimbursement or settlement under a Federally

sponsored award and should be expressly

identified and excluded from both direct costs

and facilities and administrative (indirect)

costs.

8

CASFour Standards Applicable to Educational

Institutions

- Standard 9905.506 Cost Accounting Period

Educational Institutions - In other words

- The institution should select a standard time

period to be used for the accounting of costs.

This normally coincides with the institutions

fiscal year.

9

Definition - Unallowable Costs (Both Direct and

FA Considerations)

- Costs which cannot be proven to be necessary,

reasonable, allocable and thus, the federal

government will not cover/reimburse. Such costs

are expressly UNALLOWABLE. - Examples include

- alcoholic beverages

- Entertainment (lab gatherings, non-technical

meetings) - fines/penalties/fees (late payments to vendors)

- lobbying

- losses on other sponsored projects

- memberships in civic, community organizations and

country clubs - public relations

- This list is not inclusive see A-21 Section J.

These costs cannot be charged direct OR recovered

through an FA rate.

10

Definitions Allowable Costs

- There are 2 ways to charge allowable costs

- Direct Budgeted/charged to specific cost

categories - allocable and identifiable to a single project

- reasonably supports the technical

goals/objectives/outcomes of the project - identification is made with relative ease and a

high degree of accuracy - examples include PI and research assistant

salary, travel, equipment, subcontractors, lab

supplies, etc. - FA Budgeted/charged to FA cost category only

rate based - benefit common objectives

- cannot be allocated to a single project with

relative ease and a high degree of accuracy - included in the Universitys FA cost rate

proposal and negotiation - examples include utilities, building

maintenance, landscaping, payroll, procurement

and other central office salaries, the BIG 5,

etc.

11

To be Considered Direct The Cost Must Be

- Allowable - A cost must be allowable under both

the provisions of OMB Circular A-21, Section J

AND the terms of the particular award. - Allocable - The project which pays the expense

must directly benefit from it. The item charged

to a grant must be directly related to the

objectives of the science.

12

To be Considered Direct The Cost Must Be

- Reasonable - An expense must be reasonable, in

that a prudent person would have paid the

stated amount for the good/service and also would

have applied the cost to a sponsored award in the

same manner. - Consistent - All costs incurred for the same

purpose, in like circumstances, are either to be

treated as direct OR FA (indirect) costs.

13

CAS Unlike Circumstances

- Exist when a cost that is normally considered an

FA cost qualifies as a direct cost by.. - satisfying the definition of a direct cost,

- KEYS allocable and identifiable with relative

ease high degree of accuracy - being extensive in nature (over and above routine

use at the University/support by the academic

unit),

14

CAS Unlike Circumstances

- Exist when a cost that is normally considered an

FA cost qualifies as a direct cost by.. - ensuring that the purpose of the award (survey

creation, database building) is such that its

activities are unlike those generally charged as

FA costs and can support the direct charging of

the questioned costs.

15

MAJOR PROJECTS OMB EXAMPLE 1

ADMINISTRATIVE - CLERICAL

- Large, complex research programs -

Coordination/management of a team of

researchers, units, departments,

institutions, centers

- Large consortiums

16

MAJOR PROJECTS OMB EXAMPLE 2

ADMINISTRATIVE - CLERICAL

- Projects that are geographically inaccessible to

routine support, i.e., remote field locations

17

MAJOR PROJECTS OMB EXAMPLE 3

ADMINISTRATIVE - CLERICAL

Projects that require a large number of repeated

travel and/ or meeting arrangements for

large numbers of participants

18

MAJOR PROJECTS OMB EXAMPLE 4

ADMINISTRATIVE - CLERICAL

- Projects involving

- extensive surveying, data entry and collection,

tabulation, cataloging, analysis

19

MAJOR PROJECTS OMB EXAMPLE 5

ADMINISTRATIVE - CLERICAL

- Projects focused on producing large numbers of

reports, manuals, books, and monographs,

excluding routine progress and technical reports

20

CAS The Disclosure Statement (DS-2)

- Institutions receiving an aggregate of sponsored

agreements totaling 25 million or more during

their most recently completed fiscal year must

disclose costing practices by completing the DS-2 - DS-2 is submitted to the institutions Federal

cognizant agency for review and approval - Institutions must file amendments when disclosed

practices change to comply with a new or modified

standard or for any other accounting changes made

to existing practices. - Changes having material impacts on the

institutions negotiated FA rates must obtain

approval before any change is implemented

21

CAS The Disclosure Statement (DS-2)

- Parts of the DS-2 include

- - General Information

- - Direct Costs

- - FA Costs

- - Depreciation and Use Allowances

- - Other Costs and Credits

- - Deferred Compensation and Insurance Costs

- - Central System or Group Expenses

22

CAS The Disclosure Statement (DS-2)

- Cost Accounting Standards require

- that U.Va. discloses our costing practices in a

formalized document, called the Disclosure

Statement, or DS-2 - that we actually follow the costing practices

weve outlined in the DS-2 - The DS-2 describes to the government how were

treating costs at the University. In simplified

terms, it details which costs we treat

(allocate or assign) as direct costs, and

which ones we treat as facilities

administrative (FA) costs. - The development and preparation of the FA rate

agreement is regulated by OMB Circular A-21,

Sections E-G. - No two disclosure statements are alike!

Recommended

CrystalGraphics Presentations