Cost synergies are well advanced - PowerPoint PPT Presentation

1 / 21

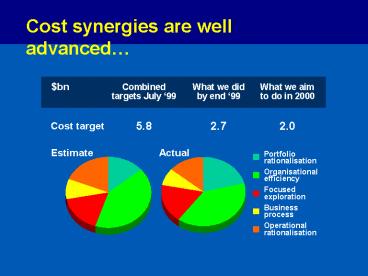

Title: Cost synergies are well advanced

1

Cost synergies are well advanced

bn

Combined targets July 99

What we did by end 99

What we aim to do in 2000

5.8

2.7

2.0

Cost target

Estimate

Actual

Portfolio rationalisation Organisational

efficiency Focused exploration Business

process Operational rationalisation

2

Global demand for gas is growing

mtoe

800

North America

600

Europe

400

200

Asia Pacific

0

1975

1980

1985

1990

1995

3

We have continued to discover giant fields

4

Future delivery

- Sustainable, double-digit earnings growth

- At mid cycle assumptions

- By demonstrating our capability

- developing the portfolio

- improving productivity

- managing a global company

- Within a disciplined, dynamic financial framework

5

We have grown

Increase since 1996

25

Supermajors

20

15

10

5

0

-5

Oil

Petrochemicals

Gas

6

Continuity and change

What hasnt changed

What has changed

- Determination to deliver

- Leadership

- Organisation model

- Commitment to performance

- Stronger finances

- Wider opportunity set

- Wider skill base

- People diversity

- Unit cost

- Commitment to cost control

- Focus on total productivity

Delivery of continuing productivity improvements

7

Investing for growth - Upstream

of Group capex 2001- 03

20

15

10

5

0

Deepwater oil

Core oil

Core gas

Emerging gas

8

Growth secured by identified projects

2000 - 2003

2004 - 2007

Deepwater oil

Marlin Crosby King Kings Peak Nakika

Gulf of Mexico

Mad Dog Holstein Atlantis Crazy Horse

Angola

Girassol

Dalia Plutonio Kizomba

9

Growth secured by identified projects

2000 - 2003

2004 - 2007

Core oil

Shearwater (UK) Northstar (Alaska)

Chirag-Azeri

Shearwater (UK)

Egypt Alaska

Core gas

Emerging gas

Trinidad Algeria Indonesia

Trinidad Indonesia

10

Growth from many sources

mboed

6000

5000

Emerging Gas

4000

Core Gas

3000

2000

Deepwater Oil

1000

Core Oil

1998

2000

2003

2007

1999

2001

2002

11

Production volumes

Mbbl/d actual/targeted

3500

Oil

99 Target

3000

2500

2000

1500

1000

500

1995

2000

2003

2007

12

Production volumes

Bcf/d actual/targeted

21

Gas

99 Target

18

15

12

9

6

3

1995

2000

2003

2007

13

Learning reduces capital costs

/ tpa LNG Plant costs

700

600

500

400

300

200

100

0

65-70

70-75

75-80

80-85

85-90

90-95

95-99

00

Trinidad Train 1

Trinidad Trains 2 and 3

14

Investing for growth - Downstream

of Group capex 2001- 03

15

10

5

0

OECD retail

Refining

Lubricants/ new markets

15

Investing for growth - Petrochemicals

of Group capex 2001- 03

10

5

0

Olefins

Aromatics

Related

16

The oil price remains unpredictable

/ bbl

30

28

26

24

22

Gulf War

20

18

Mid - cycle

16

14

Bottom - cycle

12

10

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

17

The US gas price is trending higher

per mscf

5

4

3

Mid - cycle

2

Bottom - cycle

1

0

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

18

Refining margins remain volatile

/ bbl

10

8

6

4

Mid - cycle

2

Bottom - cycle

0

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

19

Supply-led chemicals cycle drives margins

/ te

400

350

300

250

200

Mid - cycle

150

100

Bottom - cycle

50

0

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

20

New top-line growth aspiration

Growth pa 2000 to 2003

Retail Petroleum sales

3 - 4

21

driven by selective investment

bn Average pa

Gross Capex 2001 - 2003

Growth in capital employed 4 - 6 pa

Recommended

CrystalGraphics Presentations