AA DD Model - PowerPoint PPT Presentation

1 / 12

Title:

AA DD Model

Description:

Fixed exchange rate. Permanent change. SCENARIO 1: ... Since the exchange rate is supposed to be fixed, ... Money Market / Exchange Rate Equil. Perspective ... – PowerPoint PPT presentation

Number of Views:406

Avg rating:3.0/5.0

Title: AA DD Model

1

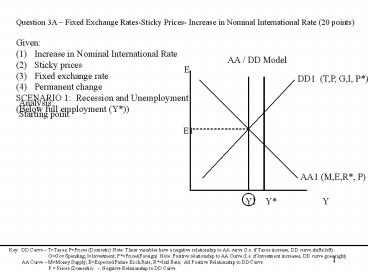

- Question 3A Fixed Exchange Rates-Sticky Prices-

Increase in Nominal International Rate (20

points) - Given

- Increase in Nominal International Rate

- Sticky prices

- Fixed exchange rate

- Permanent change

- SCENARIO 1 Recession and Unemployment

- (Below full employment (Y))

AA / DD Model

E

DD1 (T,P, G,I, P)

Analysis Starting point

E1

AA1 (M,E,R, P)

Y1 Y Y

Key DD Curve TTaxes PPrices (Domestic)

Note These variables have a negative

relationship to AA curve (I.e. if Taxes increase,

DD curve shifts left)

GGov Spending IInvestment

PPrices(Foreign) Note Positive relationship

to AA Curve (I.e. if Investment increases, DD

curve goes right) AA Curve MMoney

Supply EExpected Future Exch.Rate RIntl

Rate All Positive Relationship to DD Curve

P Prices (Domestic)

-- Negative Relationship to DD Curve

2

- Question 3A Fixed Exchange Rates-Sticky Prices-

Increase in Nominal International Rate (20

points) - Given

- Increase in Nominal International Rate

- Sticky prices

- Fixed exchange rate

- Permanent change

- SCENARIO 1 Recession and Unemployment

- (Below full employment (Y))

AA / DD Model

E

DD1 (T,P, G,I, P)

Analysis Short-term impact on AA/DD model Step

1 If R increases then the AA1 curve shifts out

to AA2 This stimulates the economy to Y

and leads to a depreciation of the currency to

E2 Since the exchange rate is supposed to be

fixed, the central bank intervenes to appreciate

the currency by selling official international

reserves (OIR) with local currency which is like

decreasing the money supply.

E2

E1

AA2 (R )

AA1 (M,E,R, P)

Assets Liabilities

OIR High-powered money (H)

(also equivalent to an

decrease Domestic credit in money supply

(M)) (I.e. treasury bonds)

Y1 Y Y

Key DD Curve TTaxes PPrices (Domestic)

Note These variables have a negative

relationship to AA curve (I.e. if Taxes increase,

DD curve shifts left)

GGov Spending IInvestment

PPrices(Foreign) Note Positive relationship

to AA Curve (I.e. if Investment increases, DD

curve goes right) AA Curve MMoney

Supply EExpected Future Exch.Rate RIntl

Rate All Positive Relationship to DD Curve

P Prices (Domestic)

-- Negative Relationship to DD Curve

3

- Question 3A Fixed Exchange Rates-Sticky Prices-

Increase in Nominal International Rate (20

points) - Given

- Increase in Nominal International Rate

- Sticky prices

- Fixed exchange rate

- Permanent change

- SCENARIO 1 Recession and Unemployment

- (Below full employment (Y))

AA / DD Model

E

DD1 (T,P, G,I, P)

Analysis Short-term impact on AA/DD model Step

2 Since money supply (M) has decreased, The AA2

curve shifts back to AA1 and the economy moves

back to Y1 (or some point under full

employment.) E2 will move back to E1

E2

E1

AA2

In a fixed rate regime under the AA/DD model, the

positive economic impact due to an increase in

international rates will be negated by the

negative impact from a decrease in money supply

due to CB intervention which is immediate.

Short-termlong-term

AA1 (M )

Y1 Y Y

Special note DD model with regards to changes

in Domestic Rates Although changes in

domestic rates ( R ) should affect Investment

(I), in the AA/DD model, investment is considered

exogenous and therefore the DD curve

will not shift.

Key DD Curve TTaxes PPrices (Domestic)

Note These variables have a negative

relationship to AA curve (I.e. if Taxes increase,

DD curve shifts left)

GGov Spending IInvestment

PPrices(Foreign) Note Positive relationship

to AA Curve (I.e. if Investment increases, DD

curve goes right) AA Curve MMoney

Supply EExpected Future Exch.Rate RIntl

Rate All Positive Relationship to DD Curve

P Prices (Domestic)

-- Negative Relationship to DD Curve

4

- Question 3A Fixed Exchange Rates-Sticky Prices-

Increase in Nominal International Rate (20

points) - Given

- Increase in Nominal International Rate

- Sticky prices

- Fixed exchange rate

- Permanent change

- SCENARIO 1 Recession and Unemployment

- (Below full employment (Y))

ISLM-BP Model

R

LM1 (M, P)

Analysis Equilibrium starting point

RRd

BP

IS1 (C,I,G,CA)

Y1 Y Y

Key LM Curve PPrices (Domestic) Note

Price has a negative relationship to LM curve

(I.e. if P increases,LM curve shifts left)

MMoney Supply Note

Money supply has a positive relationship to LM

Curve (I.e. if M increases, LM curve goes right)

IS Curve CConsumption IInvestment (

a function of RRate (domestic), GGovt

Spending, CACurrent Acct All Positive

Relationship to IS Curve BP Curve- R

Rate (Domestic), RRate (Intl) d (Risk

Premium)

5

- Question 3A Fixed Exchange Rates-Sticky Prices-

Increase in Nominal International Rate (20

points) - Given

- Increase in Nominal International Rate

- Sticky prices

- Fixed exchange rate

- Permanent change

- SCENARIO 1 Recession and Unemployment

- (Below full employment (Y))

ISLM-BP Model

R

LM1 (M, P)

Analysis Short-term impact on ISLM model Step 1

If nom. Intl. Rates go up then Rlt R This

leads to capital outflows which will cause a

depreciation of the local currency. Why? Ee

E (Interest Rate Parity

Condition) 1R- R The central bank will

intervene by selling OIR to appreciate the

currency

R

RRd

BP

IS1 (C,I,G,CA)

Assets Liabilities

OIR High-powered money (H)

(also equivalent to a

decrease Domestic credit in money supply

(M)) (I.e. treasury bonds)

Y1 Y Y

Key LM Curve PPrices (Domestic) Note

Price has a negative relationship to LM curve

(I.e. if P increases,LM curve shifts left)

MMoney Supply Note

Money supply has a positive relationship to LM

Curve (I.e. if M increases, LM curve goes right)

IS Curve CConsumption IInvestment (

a function of RRate (domestic), GGovt

Spending, CACurrent Acct All Positive

Relationship to IS Curve BP Curve- R

Rate (Domestic), RRate (Intl)

d (Risk Premium)

6

- Question 3A Fixed Exchange Rates-Sticky Prices-

Increase in Nominal International Rate (20

points) - Given

- Increase in Nominal International Rate

- Sticky prices

- Fixed exchange rate

- Permanent change

- SCENARIO 1 Recession and Unemployment

- (Below full employment (Y))

ISLM-BP Model

R

LM2 (M )

LM1 (M, P)

Analysis Short-term impact on ISLM model Step 2

Since money supply (M) has decreased, The LM1

curve shifts back to LM2 and the economy moves

back to Y2. Because the M has decreased domestic

rates have increased to equal the new

intl nominal rate hence you see the new BP line.

BP2

RRd

BP1

RRd

IS1 (C,I,G,CA)

In a fixed rate regime under the ISLM-BP model,

a rise in R causes a depreciation which the CB

will offset by appreciating the currency

(reducing M). This will raise domestic rates and

hurt an economy even more.

Y2 Y1 Y

Key LM Curve PPrices (Domestic) Note

Price has a negative relationship to LM curve

(I.e. if P increases,LM curve shifts left)

MMoney Supply Note

Money supply has a positive relationship to LM

Curve (I.e. if M increases, LM curve goes right)

IS Curve CConsumption IInvestment (

a function of RRate (domestic), GGovt

Spending, CACurrent Acct All Positive

Relationship to IS Curve BP Curve- R

Rate (Domestic), RRate (Intl)

d (Risk Premium)

7

- Question 3A Fixed Exchange Rates-Sticky Prices-

Increase in Nominal International Rate (20

points) - Given

- Increase in Nominal International Rate

- Sticky prices

- Fixed exchange rate

- Permanent change

- SCENARIO 2 In an overheated economy where the

economy is past Y, the model mechanics are still

the same

AA / DD Model ISLM-BP Model

E

R

LM2 (M )

DD1 (T,P, G,I, P)

LM1 (M, P)

BP2

E2

RRd

RRd

E1

1 2

BP1

2 1

AA2

AA1 (M )

IS1 (C,I,G,CA)

Y Y1 Y2 Y

Y Y1

1 2

8

- Question 3B Fixed Exchange Rates-Sticky Prices-

Increase in Nominal International Rate (20

points) - Given

- Increase in Nominal International Rate

- Sticky prices

- Fixed exchange rate

- Permanent change

- STERILIZING OUTFLOW OF CAPITAL

Money Market / Exchange Rate Equil. Perspective

Analysis Equilibrium starting point

E1

E Ee 1R-Rd

R (Domestic)

R1

L(R,Y)

M1 P1

New Key for MM/EE graph

Key Money Market side MMoney Supply

PPrices(Domestic) M/P Money Demand L(R,Y)

Economy as a function of RRate(Domestic) and

YOutput) Exchange Rate side RRate

(International) EeExpected future exchange

rate ECurren exchange rate d Risk Premium

9

- Question 3B Fixed Exchange Rates-Sticky Prices-

Increase in Nominal International Rate (20

points) - Given

- Increase in Nominal International Rate

- Sticky prices

- Fixed exchange rate

- Permanent change

- STERILIZING OUTFLOW OF CAPITAL

Money Market / Exchange Rate Equil. Perspective

E2

Analysis A rise in R would lead to capital

outflows causing A depreciation on the local

currency to E2

E1

E2 Ee 1R-R d

E Ee 1R-Rd

R (Domestic)

R1

L(R,Y)

M1 P1

Key Money Market side MMoney Supply

PPrices(Domestic) M/P Money Demand L(R,Y)

Economy as a function of RRate(Domestic) and

YOutput) Exchange Rate side RRate

(International) EeExpected future exchange

rate ECurren exchange rate

10

- Question 3B Fixed Exchange Rates-Sticky Prices-

Increase in Nominal International Rate (20

points) - Given

- Increase in Nominal International Rate

- Sticky prices

- Fixed exchange rate

- Permanent change

- STERILIZING OUTFLOW OF CAPITAL

Money Market / Exchange Rate Equil. Perspective

E2

Analysis The central bank would immediately

intervene by selling OIR (or buying local

currency and taking it out of circulation) thereby

appreciating the local currency but reducing

the money supply which shifts the money demand

curve back to M2 . E2 now appreciates back to

E1 P2

E1

E2 Ee 1R-R d

E Ee 1R-Rd

R (Domestic)

R1

R2

L(R,Y)

Assets Liabilities

OIR High-powered money (H)

(also equivalent to an

decrease Domestic credit in money supply

(M)) (I.e. treasury bonds)

M2 P2

M1 P1

Key Money Market side MMoney Supply

PPrices(Domestic) M/P Money Demand L(R,Y)

Economy as a function of RRate(Domestic) and

YOutput) Exchange Rate side RRate

(International) EeExpected future exchange

rate ECurren exchange rate

11

- Question 3B Fixed Exchange Rates-Sticky Prices-

Increase in Nominal International Rate (20

points) - Given

- Increase in Nominal International Rate

- Sticky prices

- Fixed exchange rate

- Permanent change

- STERILIZING OUTFLOW OF CAPITAL

Money Market / Exchange Rate Equil. Perspective

E2

Analysis By correcting the exchange rate

issue, the resulting reduction in money supply

will slow the economy by raising domestic

interest rates to R2. Sterilization would

correct this problem. To attract foreign

capital the govt could offer treasury bonds

with a higher risk premium, thereby lowering the

exchange rate curve. This increase in domestic

credit would increase high-powered money and

thereby reduce domestic rates back down to R1,

minimizing any economic Impacts from a rise in

R

E1

E2 Ee 1R-Rd

E Ee 1R-Rd

R (Domestic)

R2

R1

L(R,Y)

M2 P2

Assets Liabilities

OIR High-powered money (H)

(also equivalent to an

decrease Domestic credit in money supply

(M)) ( treasury bonds)

M1 P1

Key Money Market side MMoney Supply

PPrices(Domestic) M/P Money Demand L(R,Y)

Economy as a function of RRate(Domestic) and

YOutput) Exchange Rate side RRate

(International) EeExpected future exchange

rate ECurren exchange rate

12

- Question 3C Fixed Exchange Rates-Sticky Prices-

Increase in Nominal International Rate (20

points) - Given

- Increase in Nominal International Rate

- Sticky prices

- Fixed exchange rate

- Permanent change

- POLICY RECOMMENDATION Sterilize if scenario 1.

Do not sterilize if scenario 2

Scenario 2 (Overemployment) Do NOT sterilize.

The rise in R will lead to capital outflows

causing a depreciation. The CB would

intervene would selling OIR thereby

appreciating the currency. The resulting

decrease in high-powered money (H) would cool off

the overheated economy. Sterilization would

simply keep the economy overheated

Scenario 1 (Underemploymentt) DO sterilize. The

rise in R will lead to capital outflows

causing a depreciation. The CB would

intervene would selling OIR thereby

appreciating the currency. The resulting

decrease in high-powered money (H) would

slowl the economy more making it worse

off. Sterilization would help offset the negative

effects of a CB currency appreciation

intervention One risk of sterilization is that

the country default risk grows from the issuance

of bonds if the bonds are used primarily to

finance a consumption-based fiscal deficit. In

order to entice investment, the govt will raise

the risk premium which further exacerbates

country default risk because investors will

question the governments ability to pay back

both the interest and principal of the bonds. A

second risk is that the govt may run out of

bonds and be forced to borrow from the central

bank. This leads to what is called a

quasi-fiscal deficit.

Recommended

CrystalGraphics Presentations