Properties of the least squares estimates... - PowerPoint PPT Presentation

Title:

Properties of the least squares estimates...

Description:

( the standard error is the estimated standard deviation of the estimator) ... Note that when x0 = 0, we have the special case of testing and/or estimating b0. ... – PowerPoint PPT presentation

Number of Views:246

Avg rating:3.0/5.0

Title: Properties of the least squares estimates...

1

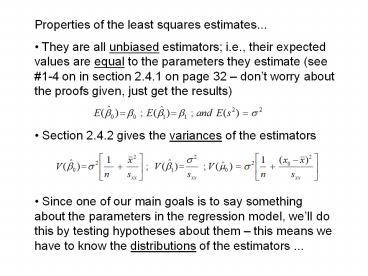

- Properties of the least squares estimates...

- They are all unbiased estimators i.e., their

expected values are equal to the parameters they

estimate (see 1-4 on in section 2.4.1 on page 32

dont worry about the proofs given, just get

the results) - Section 2.4.2 gives the variances of the

estimators - Since one of our main goals is to say something

about the parameters in the regression model,

well do this by testing hypotheses about them

this means we have to know the distributions of

the estimators ...

2

To get the distributions of the estimators, we

must assume normality of the error term in the

model so not just that E(e) 0 and V(e) s2

but that eN(0, s2). This assumption implies the

following important distributional result about

the estimator of the slope Notice that weve

basically standardized b1-hat by taking away its

mean and dividing by its so-called standard

error. (the standard error is the estimated

standard deviation of the estimator)... The

resulting standardized statistic has a

t-distribution with n-2 degrees of freedom. Note

that the df n-2 the number of df associated

with the error sum of squares, the numerator in

our estimator s2 .

3

- So now, we may use the distribution of the

estimated slope to either - test the hypothesis that H0 b1 0 or

- get a confidence interval for b1

- Lets review both of these concepts from

elementary statistics... - compare the value of the test statistic, T on the

previous slide, assuming the null hypothesis is

true, with the percentiles of the t(n-2)

distribution to decide on whether to reject the

null hypothesis or not. This comparison yields a

so-called p-value and small p-values yield

rejection while large p-values yield

non-rejection of the null hypothesis. - construct a 100(1 a ) confidence interval for

the true slope b1 by the usual estimate /-

(margin of error) - estimate /- (value from t table)(s.e. of

estimator) - ...remember that the s.e. of the estimator

standard error of estimator estimated standard

deviation of the estimator

4

- Similarly, we may either test hypotheses or

estimate m0 where using the unbiased least

squares estimator - Note that when x0 0, we have the special case

of testing and/or estimating b0 . - Now go back over the Hardness example and do the

various tests dont forget to write out an

interpretation of what the results mean...! - Look at how R implements these tests and

estimates, try for the Hardness data.... - do a scatterplot plot in the prediction line

(the regression line, the mean line) can you

plot the confidence bands around this line using

the formula 2.23 at the top of page 37? - do the hypothesis test for no slope and give

your results in terms of p-value. Is Hardness

linearly related to Temperature of the quench

bath water?

Recommended

CrystalGraphics Presentations