Comparing APV, FTE, and WACC continued from lecture 4 - PowerPoint PPT Presentation

1 / 21

Title:

Comparing APV, FTE, and WACC continued from lecture 4

Description:

( otherwise we could use firm beta) ... Failing to releverage asset betas. Failing to include taxes in unleveraging and leveraging betas. ... – PowerPoint PPT presentation

Number of Views:886

Avg rating:3.0/5.0

Title: Comparing APV, FTE, and WACC continued from lecture 4

1

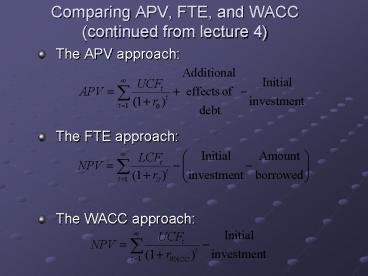

Comparing APV, FTE, and WACC (continued from

lecture 4)

- The APV approach

- The FTE approach

- The WACC approach

2

What cash flows to use?

- Both APV and WACC use unlevered after tax cash

flows EBIT(1-Tc), i.e. NOT actual after tax cash

flows (EBIT-i)(1-Tc)i !!! - Thats why in WACC the cost of debt for the firm

is kd(1-Tc) - For the shareholders paying i out of EBIT and

then being taxed is the same as simply paying

i(1-Tc) out of EBIT(1-Tc) they get

(EBIT-i)(1-Tc) anyway.

3

What are the discount rates?

- For APV use the cost of equity for the unlevered

firm r0. - For FTE and WACC use the cost of equity for the

levered firm rS.

4

Which capital structure?

- Always use target weights in WACC.

- When computing weights in WACC and B/S for rs use

market values market values are closer to actual

amounts of money that can be raised by issuing

securities. - Ideally, the resulting capital structure (in

terms of market values) should coincide with the

target. - If you choose an arbitrary B/S mix as a target,

compute WACC based on it, calculate the projects

PV and then calculate the actual B/S in market

values it may be the same as the initial target! - Example at the previous lecture (WACC for

Pearson). The assumed target ratio was 1.5, but

the actual one turned out to be 600/406.68 - (Here 406.68 is the market value of equity PV

Debt 106.68 600)

5

Which method is better?

- In theory they are equivalent (at least for the

case when debt is perpetuity) - In practice

- Use WACC and FTE when you target the constant

debt ratio. Otherwise computations become

complex. - Use APV when the level of debt is supposed to be

constant. APV does not care about B/S, it only

cares about the PV of Tax Shield. - In the real world, WACC is the most widely used

6

Determining rs. Pure play technique

- We know that

- What if we dont know r0? We can use

- But how to determine ?S if the project has a risk

different from the one of the firm? (otherwise we

could use firm beta) - Answer look at a firm whose whole business is

similar to your project (pure-play firm).

7

- The problem pure-play firm may have a leverage

that differs from your project - Solution unlever the pure-play firm, calculate

its beta and then relever it with your

projects leverage.

In a world with corporate taxes, and riskless

debt, it can be shown that the relationship

between the beta of the unlevered firm and the

beta of levered equity is

8

Applying the Pure-Play Technique -Time Warners

Cable Division

- Pure-Play Equity or

Debt To Debt To - Firm Market Beta MV

of Capital MV of Equity - Cablevision Systems 1.20 68.2

214.5 - Century 1.01

64.8 184.1 - Comcast 1.18

48.5 94.8

- Jones Intercable 1.07

60.7 154.5 - TCI Group 1.17

50.0 100.0

9

- Unlevered beta ?U ?L /1 (1 - TC) B/S

Pure-Play Equity or Debt

To Debt To Asset or Firm

Market Beta Capital

Equity Unlevered

Beta Cablevision Systems

1.20 68.2 214.5

0.501 Century 1.01

64.8 184.1 0.460 Comcast

1.18 48.5

94.8 0.730 Jones Intercable

1.07 60.7 154.5

0.534 TCI Group 1.17

50.0 100.0 0.705

Average Asset

Beta 0.586

10

Releveraging Asset Betas - Time Warners Cable

Division

- values for your project

Calculating the Cost of Equity - Time Warners

Cable Division

11

Common Errors in Calculating the WACC Using the

CAPM

- Using different capital structure assumptions in

computing the cost of equity than are used in

calculating the WACC. - Using a different maturity for the risk-free rate

in the CAPM than the one used in calculating the

market risk premium. - Estimating the market risk premium based on the

most recent returns rather than a long-term time

series.

12

- Using the historical average T-bond or T-bill

rate instead of the current rate. - Failing to releverage asset betas.

- Failing to include taxes in unleveraging and

leveraging betas. - Using the historical market return instead of the

market risk premium.

13

Other ways to deal with uncertainty

- Sensitivity analysis

- How sensitive NPV is to changes in parameters

- Identifies the most important variables that can

alter NPV in a drastic way - Scenario analysis identifies the most important

scenarios (i.e. combinations of variables

values) rather than considering each variable

separately

14

- Traditional simulation

- Estimate the probability distributions of the

variables that affect cash flows. - Simulate NPV to get a distribution of NPV.

- To calculate NPV for each realization of cash

flows discount at the risk-free rate. - Problem what is the meaning of the resulting

distribution? Shall we accept or reject the

project? - Decision trees

- Allows to account for managerial flexibility!

- But the problem at what rate to discount???

15

Failure of traditional capital budgeting

- Option to defer investment

- The manager has an option to defer undertaking a

project (building a plant) for a year. - If he chooses to defer, after a year he either

may or may not find it profitable to build a

plant - What is the value of this flexibility?

16

Setup

- At t 0 investment outlay (required inv-t) I0

104 - At t 1

- If the market moves up (prob. q) the project

generates V 180 - If the market moves down (prob. 1-q) the project

generates V 60 - The manager has a choice

- To invest at t 0 and get 180 with prob. q and

60 with prob 1-q, or - To wait until t 1 and build a plant only in the

good state of nature (i.e. if the market has

moved up). But then the required investment is I1

112.32. Thus, then he gets - E 180 I1 67.68 in the good state

- E 0 in the bad state.

17

- Assume q 1/2

- Risk free rate r 8

- There exist a risky security (twin security),

which payoffs are perfectly correlated with the

payoffs of the project. - Payoffs S 36, S 12

- Price S 20

- ? rate of return k (½ S ½ S)/S 20

- How much a manager would pay for this investment

opportunity (what is the value of the project)?

18

No flexibility case

- Assume theres no option to defer

- The traditional DCF technique yields

- V0 (qV (1-q)V-)/(1k) (0.5180

0.5160)/(1 0.2) 100 - NPVpassive V0 - I0 100 104 - 4

- Reject the project!

19

When the option to defer is present

- Consider a strategy

- Buying N shares of the twin security S, partly

financed by borrowing of amount B at the riskless

rate r 8 - We can always pick such N and B that

- E NS - (1r)B

- E- NS- - (1r)B

- Thus, we can replicate the payoffs from the

project with this portfolio ? the arbitrage

argument tells us that the project value must be

the same as the price of the portfolio E0 NS -

B

20

- N (E - E-)/(S - S-)

- B (NS- E-)/(1r)

- We obtain the risk-neutral valuation!

- E0 NS B (pE (1-p)E-)/(1r)

- where p ((1 r)S S-)/(S - S-)

- Notice q does not enter the expression for E0!

Why? Because q is already incorporated in the

price of the twin security S. - pE (1-p)E- can be viewed as Certainty

Equivalent of the random payoff at t 1.

21

- For our project

- p 0.4, E0 25.07

- The value of the option

- E0 NPVpassive 25.07 (-4) 29.07

- What if we use traditional capital budgeting,

i.e. the actual probabilities q and the rate of

return on the twin security k 20 to discount

cash flows? - E0 (qE (1-q)E-)/(1k) 28.20 gt 25.07

- Overestimation! One should not pay more than

25.07 for this option!

Recommended

CrystalGraphics Presentations