Importance of Accounting - PowerPoint PPT Presentation

1 / 52

Title:

Importance of Accounting

Description:

... and the right side is the normal balance side for liabilities ... Chapter 1 Identifies Records Communicates ... 13 14 ... – PowerPoint PPT presentation

Number of Views:117

Avg rating:3.0/5.0

Title: Importance of Accounting

1

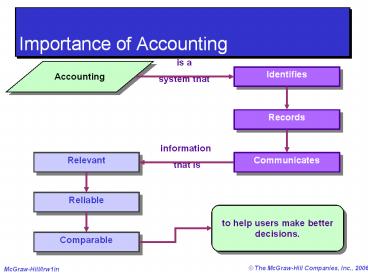

Importance of Accounting

Accounting

Identifies

Records

Communicates

Relevant

Reliable

to help users make better decisions.

Comparable

2

Generally Accepted Accounting Principles

Financial accounting practice is governed by

concepts and rules known as generally accepted

accounting principles (GAAP).

3

Principles of Accounting General Principles

Source documents.

4

Principles of Accounting

5

Expanded Accounting Equation

6

Double-Entry Accounting

Normal Balance

Normal Balance

Nomal Balance

7

Double-Entry Accounting

Exh. 3.8

Equity

Normal Balance

Normal Balance

Normal Balance

Normal Balance

8

Double-Entry Accounting

- When there is a debited account, there must be a

credited account. - The total amount debited must be equal to the

total amount credited for each transaction. - The left side is the normal balance side for

assets, and the right side is the normal balance

side for liabilities and equity. - ?????,??????

9

Analyzing and Recording Process

10

After processing its remaining transactions for

December, FastForwards Trial Balance is prepared.

9,270

11

Recognizing Revenues and Expenses

- Revenue recognition principle requires that

revenue be recorded when earned, not before or

after. - Matching principle intends to record expenses in

the same accounting period as the revenues that

are earned as a result of these expenses.

12

Adjusting Accounts

An adjusting entry is recorded to bring an asset

or liability account balance to its proper amount.

Framework for Adjustments

Adjustments

including depreciation

13

FastForwardWork Sheet For Month Ended December

31, 2004

Prepare adjusted trial balance.

14

Sort adjusted trial balance amounts to financial

statements.

FastForwardWork Sheet For Month Ended December

31, 2004

15

Financial Statements

- Income Statement revenues and expenses together

with the how much profit the firm makes. - Statement of Owners Equity reports information

how equity changes over the reporting period. - Balance Sheet a companys financial position at

a point of time. - Statement of cash flows cash receipts and cash

payments over a period of time.

16

Temporary and Permanent Accounts

The closing process applies only to temporary

accounts.

17

Accounting cycle

18

Inventory Systems

Beginninginventory

Net cost ofpurchases

Merchandiseavailable for sale

Ending Inventory

Cost of GoodsSold

19

Itemized Cost of Merchandise Purchased

20

Accounting for Merchandise Sales

21

Inventory Cost Flow Assumptions

First-In, First-Out(FIFO)

Assumes costs flow in the order incurred.

Last-In, First-Out(LIFO)

Assumes costs flow in the reverse order incurred.

Weighted Average

Assumes costs flow at an average of the costs

available.

22

Sales of Merchandise

- On March 18, Diamond Store sold 25,000 of

merchandise on account. The merchandise was

carried in inventory at a cost of 18,000.

23

Valuing Accounts Receivable

- Some customers may not pay their account.

Uncollectible amounts are referred to as bad

debts. There are two methods of dealing with bad

debts - Direct Write-Off Method

- Allowance Method

24

Estimating Bad Debts Expense

- Two Methods

- Percent of Sales Method

- Accounts Receivable Methods

- Percent of Accounts Receivable

- Aging of Accounts Receivable Method

25

Percent of Accounts Receivable

26

Computing Maturity and Interest

27

Factors in Computing Depreciation

- The calculation of depreciation requires three

amounts for each asset - Cost.

- Salvage Value.

- Useful Life.

28

Depreciation Methods

- Straight-line

- Units-of-production

- Declining balance

29

Disposals of Plant Assets

Update depreciation to the date of disposal.

Journalize disposal by

Recording cashreceived (debit)or paid

(credit).

Recording again (credit) or loss (debit).

Removing accumulateddepreciation (debit).

Removing the asset cost (credit).

30

Determine Gain or Loss on Disposal

Selling Plant Assets

31

Known (Determinable) Liabilities

Accounts Payable

Sales Taxes Payable

Unearned Revenues

Short-Term Notes Payable

Payroll Liabilities

Multi-Period Known Liabilities

32

Estimated Liabilities

- An estimated liability is a known obligation of

an uncertain amount, but one that can be

reasonably estimated.

Warranty Sellers obligation to replace or

correct a product (or service) that fails to

perform as expected within a specified period. To

conform with the matching principle, the seller

reports expected warranty expense in the period

when revenue from the sale is reported.

33

Corporation

- Issuing stocks common / preferred stocks

- Distribute dividends cash / stock dividends

- Stock splits

- Treasury Stock

- Earning Per Share

34

Bond Discount or Premium

Prepare the entry for Jan. 1, 2005 to record the

following bond issue by Rose Co. Par Value

1,000,000Issue Price 92.6405 of par

valueStated Interest Rate 10Market Interest

Rate 12Interest Dates 6/30 and 12/31Bond

Date Jan. 1, 2005Maturity Date Dec. 31, 2009

(5 years)

35

Issuing Bonds at a Discount

On Jan. 1, 2005 Rose Co. would record the bond

issue as follows.

Contra-Liability Account

36

Issuing Bonds at a Discount

Make the following entry every six months to

record the cash interest payment and the

amortization of the discount.

73,595 10 periods 7,360 (rounded) 1,000,000

10 ½ 50,000

37

Issuing Bonds at a Premium

On Jan. 1, 2005 Rose Co. would record the bond

issue as follows.

Adjunct-Liability Account

38

Issuing Bonds at a Premium

This entry is made every six months to record the

cash interest payment and the amortization of the

premium.

81,145 10 periods 8,115 (rounded) 1,000,000

10 ½ 50,000

39

Classes of and Reporting for Investments

Class of Investment

Held-To-Maturity

Available-For-Sale

Significant Influence

Controlling Influence

Trading

Consolidate

EquityMethod

Market ValueMethod

AmortizedCost

Reporting

40

Classifying Cash Flows

- The Statement of Cash Flows includes the

following three sections - Operating Activities

- Investing Activities

- Financing Activities

41

Analyzing the Cash Account

Lets use this Cash account to prepare BG

Companys Statement of Cash Flows under the

Direct Method.

42

Indirect Method of Reporting Operating Cash Flows

Changes in current assets and current liabilities.

Losses and - Gains

Noncash expenses such as depreciation and

amortization.

97.5 of all companies use the indirect method.

43

Tools of Analysis

Horizontal Analysis

Comparing a companys financial condition and

performance across time

Time

44

Tools of Analysis

V e r t i c a l A n a l y s i s

Comparing a companys financial condition and

performance to a base amount

45

Tools of Analysis

Using key relations among financial statement

items

Ratio Analysis

46

Building Blocks of Analysis

Liquidity and Efficiency

Solvency

MarketProspects

Profitability

47

Computing Break-Even Point

How much contribution margin must this company

have to cover its fixed costs (break even)?

Answer 30,000

48

Computing Sales (Dollars) for aTarget Net Income

Exh. 22-14

- Target net income is income after income tax.

Fixed Target net Incomecosts

income taxes

Dollar sales

Contribution margin ratio

49

Computing MultiproductBreak-Even Point

Exh. 22-19

- The resulting break-even formulafor composite

unit sales is

Fixed costsContribution marginper composite unit

Break-even pointin composite units

Consider the following example

Continue

50

Net Present Valuewith Even Cash Flows

Exh. 26-7

A positive net present value indicates that

thisproject earns more than 12 percent on the

investment.

51

Internal Rate of Return (IRR)

The interest rate that makes . . .

- The net present value equal zero.

52

Relevant Costs

- Costs that are applicableto a particular

decision. - Costs that should have a bearing on which

alternative a manager selects. - Costs that are avoidable.

- Future costs that differbetween alternatives.