Reconciling Net Income to CFO using the Indirect Method - PowerPoint PPT Presentation

1 / 10

Title:

Reconciling Net Income to CFO using the Indirect Method

Description:

Reconciling Net Income to CFO using the Indirect Method Start with Net Income Add-back non-cash charges (depreciation, amortization, non-cash ... – PowerPoint PPT presentation

Number of Views:30

Avg rating:3.0/5.0

Title: Reconciling Net Income to CFO using the Indirect Method

1

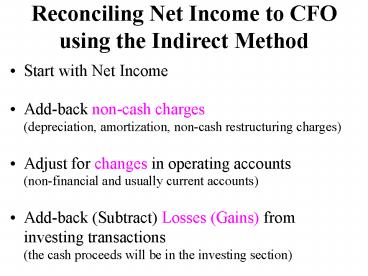

Reconciling Net Income to CFO using the Indirect

Method

- Start with Net Income

- Add-back non-cash charges

(depreciation, amortization, non-cash

restructuring charges) - Adjust for changes in operating accounts

(non-financial and usually current accounts) - Add-back (Subtract) Losses (Gains) from investing

transactions

(the cash proceeds will be in the investing

section)

2

Indirect Cash Flow Statement 1. Cash from

Operations Cash Collections - Cash

Payments (Reflects day-to-day cash flows) 2.

Cash from Investing (Reflects assets cash flows

that are

not day-to-day) 3. Cash from Financing

(Reflects liability and equity cash

flows that are not

day-to-day)

3

Developing the Operating Portion of the Cash

Flow Statement

Converting Income to Operating Cash Flows

1. Convert income to Cash Revenues - Cash

Expenses 2. Convert Cash Revenues - Cash

Expenses to Cash Collections - Cash Payments

from Operations

4

Income Revenues - Expenses

1a. Income Cash revenues non-cash revenues

- cash expenses - non-cash

expenses Solve 1a for Cash revenues - cash

expenses 1b. Cash revenues - cash expenses

Income non-cash

expenses - non-cash revenues

5

Two typical non-cash expenses are

depreciation expense and

purchases on credit (increases in A/P) One

typical non-cash revenue is sales on credit

(increases in A/R)

6

Insert examples for non-cash revenues and

non-cash expenses 1. Depreciation expense is an

example of a non cash expense (Non cash

revenues would be subtractions). 2.

Accounts/Receivable is an example of an operating

asset. 3. Accounts/Payable is an example of an

operating liability. (Not all short-term

accounts are operating accounts. Some

long-term accounts occasionally are operating

accounts.)

7

With examples Cash Revenues - Cash Expenses

Income non-cash

expenses -

non-cash revenues

becomes Cash Revenues - Cash Expenses Income

depreciation

expense increases in A/P

- increases in A/R

8

Recognize that Cash Collections Cash Revenues

decreases in A/R or Cash Revenues Cash

Collections - decreases in A/R and

Recognize that Cash Payments Cash Expenses

decreases in A/P Cash Expenses Cash Payments

- decreases in A/P

9

Substitute for Cash Revenues - Cash Expenses

Basic Relationship Cash Revenues - Cash Expenses

Income

depreciation expense increases in A/P

- increases in

A/R Equations to be substituted Cash Revenues

Cash Collections - decreases in A/R Cash Expenses

Cash Payments - decreases in A/P Relationship

Becomes Cash Collections - decreases in A/R -

Cash Payments - decreases in A/P Income

depreciation

expense increases in A/P

- increases in A/R

10

Rearrange to focus on Cash from Operations (CFO)

Cash Collections - decreases in A/R - Cash

Payments - decreases in A/P Income

depreciation

expense increases in A/P

- increases in A/R

becomes CFO or Cash Collections - Cash

Payments Income

depreciation expense

decreases in A/R - increases in A/R

increases in A/P

- decreases in A/P or CFO or Cash

Collections - Cash Payments Income

depreciation expense

- ? in A/R ? in A/P

Recommended

CrystalGraphics Presentations