Hedging with Currency Options - PowerPoint PPT Presentation

Title:

Hedging with Currency Options

Description:

Hedging with Currency Options An American firm has 1,000,000 payables 3months hence. Today the market rates are: Spot : 1.3825/1.3830; 90day forward swap points ... – PowerPoint PPT presentation

Number of Views:335

Avg rating:3.0/5.0

Title: Hedging with Currency Options

1

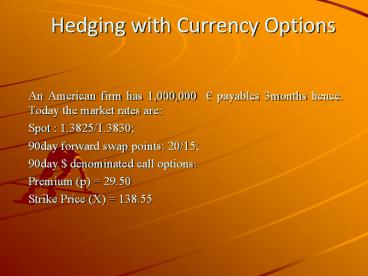

Hedging with Currency Options

- An American firm has 1,000,000 payables

3months hence. Today the market rates are - Spot 1.3825/1.3830

- 90day forward swap points 20/15

- 90day denominated call options

- Premium (p) 29.50

- Strike Price (X) 138.55

2

- Before going into details of the case study we

should be careful about the interpretation of the

quotations of options. - In options market premium and strike price for

dollar denominated contracts are given in cents - So in our problem

- Premium(p) 29.50 cents i.e. 0.2950/100

- Strike Price (X) 138.55 cents i.e. 1.3855

/

3

- The American firm has three alternatives to deal

- with the foreign exchange exposure

- Open Position

- Forward Hedge

- Option Hedge

4

- At maturity, assuming spot rate as ST ,under

different - alternatives the outflow will be

- Open Position

- 1,000,000 ST

- Forward Hedge

- Forward Rate 1.3830

0.0015 -

1.3815 - Outflow 1,000,000 1.3815 1,381,500

5

iii) Options Hedging Case 1 If ST gt X Premium

One contract in involves 10000. So

to purchase 1,000,000 , 100contracts are

needed. Premium for 1 contract 10000

0.2950/100

29.5 So for 100 contracts 100 29.5

2950

6

Premium is paid at Upfront. But Exercising

the option may be done after 90days. So

assuming 10p.a interest for 90 days the maturity

value of this premium will be 2950 2950

90/365 10/100 3023(apprx) At maturity two

cases may happen Case 1 If ST gt X Case 1 If ST

lt X

7

Under Case 1, Option will be exercised and

the outflow in Options hedging will be

1,000,000 1.3855 3023 1,388,523 Under

Case 2, Option will not be exercised and the

outflow in Options hedging will be 1,000,000ST

3023 in

8

So at maturity assuming spot rate ST the

outflows under different alternatives are Open

Position 1,000,000 ST Forward Position

1,000,000 x 1.3815 1,381,500 Option

Position 1,000,0001.3855 3023 1,388,523

(if STgtX) or 1,000,000ST 3023 (if STltX)

9

Break Even Point between different

alternatives Break even point between any two

alternative is that point where outflow is same

i) Open position and Forward position

1,000,000 ST 1,381,500 So these two

positions are equivalent when ST becomes equal to

forward rate determined at time t 0, here

1.3815 /. If STgt 1.3815, the forward hedging

will be preferable.

10

ii) Open position Option position 1,000,000

ST 1,000,0001.3855 3023 So ST 1.3885 As

long as ST lt 1.3885 open position will

be Preferable As soon as ST gt 1.3885, Option

will be exercised and it will be preferable

11

iii) Forward position Option

position 1,000,0001.3815 1,000,000ST 3023

So ST 1.3785 At lower spot value at maturity

than this option is preferable than forward,

because of its one way privilege-the firm can buy

euro in open market letting the option lapse.

Recommended

CrystalGraphics Presentations