Shailaja R Deshmukh

Title:

Shailaja R Deshmukh

Description:

h(x) e-ax (S (a zx)k-1/(k-1)!) dx = 0. h(x) e-?x = 0, ? = a (1 z), 0 ? a ... S d (1 d) k 1( h(x) ak e-ax xk-1/?(k)dx) = 0, sum being taken on I ... –

Number of Views:86

Avg rating:3.0/5.0

Title: Shailaja R Deshmukh

1

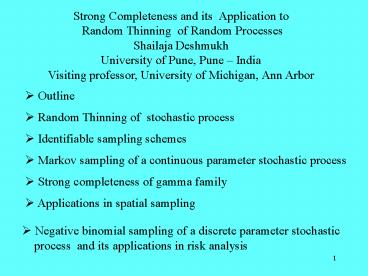

Strong Completeness and its Application to

Random Thinning of Random Processes Shailaja

Deshmukh University of Pune, Pune

India Visiting professor, University of Michigan,

Ann Arbor

- Outline

- Random Thinning of stochastic process

- Identifiable sampling schemes

- Markov sampling of a continuous parameter

stochastic process

- Strong completeness of gamma family

- Applications in spatial sampling

- Negative binomial sampling of a discrete

parameter stochastic - process and its applications in risk analysis

2

- X(t) , t ? T , T Discrete or continuous

- Various observational schemes

- Complete observation for a fixed time interval

- Keiding (1974, 1975), Athreya (1975, 1978)

- Observing a process till a fixed no. events occur

(inverse sampling) - Moran (1951), Keiding (1974, 1975)

- Observing the process at specified deterministic

epochs t1, t2, tn - Prakasa Rao (1988), Su Cambanis

(1993)

3

- Kingman (1963, Ann. Math. Statist )

- Fixed epoch sampling suffers from non-

identifiability - Observed data may come from different processes

- Kingman (1963) advocated selecting epochs t1,

t2, tn randomly

- Criterion Process derived from the original

process randomly, - should determine the stochastic structure of

the original process - uniquely

- The process used for sampling should be

identifiable

- X(t), t ? T Original process under study

- Zn X(Tn), Tn Random variables

- Zn, n ? 1 Derived process or randomly

thinned process

4

- Identifiability of a sampling scheme

d

X(1) (t)

X(2) (t)

?

?

?

d

Z(1) (n)

Z(2) (n)

- Derived process determines the original process

uniquely

- Identifiability is essential for justfication of

inference based - on randomly derived process

- Basawa (1974) , Baba (1982)

- Identifiable sampling schemes

5

continuous

discrete

- Tn n th success in

- independent Bernoulli trials.

- Bernoulli sampling

- Deshmukh (1991), Austr. J. of Statistics

- Tn n th event

- in Poisson process.

- Poisson sampling

- Kingman (1963)

- Ann. Math.Statist

- Tn n th visit to state 1

- in two state Markov chain

- Markov sampling

- Deshmukh (2000), Austr.New

- Zealand J. of Statistics

- Tn n th visit to state 1

- in two state Markov process.

- Markov process sampling

- Strong completeness of gamma

- family. Deshmukh (2005)

- Stochastic modelling Applications

Tn n-th epoch of k-th success in Bernoulli

trials Strong completeness of negative binomial

family

Extension of PASTA

6

- Markov sampling of a continuous parameter

stochastic process

- X(t), t 0 continuous parameter stochastic

process

- Y(t), t 0 Markov process with state space

0,1 and Y(0) 1 - Y(t) is independent of X(t)

- Observe X(t) at the epochs of visits to state

1 of Y(t)

- Tk S1 Sk epoch of k-th visit to state

1 of Y(t) - X(t) is observed at Tk, k 1,

- Z(k) X(Tk), k 1 is derived from the

original process by MS

7

- Aim Whether Z(k) determines the stochastic

structure of the original - process uniquely

- Waiting time Tk for the k-th visit to the state

1 of the Markov process

1 W1 0 W0 1

- Waiting time for the first visit to the state1

S1 W0 W1

- W0 and W1 are independent random variables

having exponential - distribution with mean ?0-1 and ?1-1

respectively.

- Tk S1 Sk V0 V1, where Vi G (?i,

k ), - ?i scale parameter and k is the shape

parameter, i 0,1.

8

- Sampling scheme is identifiable

d

X(1) (t)

X(2) (t)

?

Markov sampling

?

?

d

Z(1) (k)

Z(2) (k)

Family of finite dimensional distribution

functions of X(i) (t)

Fi Fi(t1, t2,, tn) Fi(t1, t2,, tn x1,..,

xn) PXi(tj)

xj j 1,, n,

x1,x2,, xn - real numbers, t1,t2,, tn -

positive real numbers,

t1 lt t2 lt lt tn.

Family of finite dimensional distribution

functions of Z(i) (k)

Gi PZi(K(j)) xj, j 1, 2, ,n , K(j) k1

k2 kj

8

9

k1 k2 kn

0 K(1) K(2)

K(n-1)

K(n)

TK(1) TK(2)

TK(n-1)

TK(n) U1 U2

Un-1 Un L1 L2

Ln

Let TK(j) Uj and Lj Uj Uj-1 , Lj U1

U2 Uj

Gi PZi(K(j)) xj, j 1,, n PXi(TK(j))

xj, j 1,, n PXi(Uj) xj,

j 1,, n E PXi(Uj) xj, j

1,, n U1,U2,,Un

EPXi(Uj) xj, j 1,, n

EFi(L1, L1L2, , L1L2Ln)

10

G1 G2 implies EF1(L1, L1L2, ,

L1L2Ln) EF2(L1, L1L2, ,

L1L2Ln) EF1(L1, L1L2, , L1Ln)- F2(L1,

L1L2, , L1Ln) 0

Expectation is with respect to the joint

distribution of (L1, L2,,Ln). L1, L2,,Ln are

independent and Lj Vokj V1kj ,where

Vokj G (?0, kj ) and V1kj G (?1, kj ),

?0 and ?1 are known, kj j 1, ,n are the only

unknown parameters . Expectation is with respect

to the joint distribution of (Vokj ,V1kj j 1,

,n).

If the joint distribution of (Vokj ,V1kj j 1,

,n) is complete

G1 G2 implies F1 F2 Strong completeness of

family of Vokj /V1kj for any j implies

completeness of the joint distributions

11

X G ( a, k), a scale parameter, k shape

parameter f (x) ak e-ax xk-1/?(k), x gt

0

a known, k ? I

Not a one parameter exponential family, parameter

space is not an open set

Complete family

12

Ek( h(x)) 0 for all k ? I

? ? h(x) ak e-ax xk-1/?(k)dx 0 , for all k ?

I ? g(k) 0 , for all k ? I

? S zk g(k) 0, 0 lt z lt 1

? ? h(x) e-ax (S (a zx)k-1/(k-1)!) dx 0

? ? h(x) e-?x 0, ? a (1 z), 0 lt ? lt a

? ? h(x) e-?x 0, for all ? gt 0, by analytic

continuation

? h(x) 0, a.s. Pk for all k ? I

G(a , k), k ? I is a complete family

Strongly complete

13

- Definition A family of distributions F?, ? ? T

is called strongly - complete if there exists a measure µ on (T ,

?) such that for every - subset T of T for which µ(T T) 0, ?

h(x) F?(dx) 0 for all - ? ? T implies that h (x) 0 a. s. P? for

every ? ? T. (Zacks, 1971)

- Strong completeness implies completeness by

taking T T

- Suppose T1 and T2 are independent random

variables. If F?T1,? ? T - is complete and F?T2, ? ? T is strongly

complete then the family - of joint distributions F?, ?T1,T2 ? ? T, ?

? T is complete. - (Zacks, 1971)

- Gamma family is strongly complete

- Parameter space - I, ? - sigma field, µ is a

measure induced by - geometric distribution

- For A ? ?, µ(A) S d (1 d) k 1, sum being

taken over k ? A

14

Suppose T is a subset of I such that µ(I - T

) 0

? h(x) ak e-ax xk-1/?(k)dx 0 , for all k ? T

? g(k) 0, for all k ? T

µ(k) 0 , for all k ? (I - T)

g(k) µ(k) 0 , for all k ? I

S d (1 d) k 1( ? h(x) ak e-ax xk-1/?(k)dx)

0, sum being taken on I

Using Fubinis theorem, summation and integration

can be interchanged

? h(x) e-?x 0, for all ? gt 0, by analytic

continuation

h(x) 0, a.s. Pk for all k ? I

Gamma family is strongly complete

15

Thus, the joint distribution of ((Vokj ,V1kj j

1, ,n) ) is complete. Further using continuity

of F we get G1 G2

implies F1 F2

Markov sampling is an identifiable sampling

scheme

- Z(k), k 1 is a Markov process iff X(t)is a

Markov process. - Z(k), k 1 is a stationary process iff

X(t)is a stationary - process.

- limt ?8PX(t) ? B lim n?8 PZn ? B

- Fraction of time the process X(t) is in set B

(a measurable - subset of a state space of X(t)) is the

same as the fraction of - time the process X(t) is in B when observed

at the epochs of - visits to the state 1 of Y(t)

- Parallel to the Poisson Arrivals See Time

Averages (PASTA) - property

16

- Application Identifiable sampling designs in

spatial processes to - select the locations.

- Z(s) , s ? D Spatial process

- s Locations, D Study region

- Aim To select locations at which the

characteristic under study is - to be measured, thickness or

smoothness of powder coating, - nests of birds

- Most common scheme Regular sampling,

Cressie,1993

Non-identifiability

16

17

- Study region Continuous

- Aim Selection of locations (s1,s2)

- If both coordinates are selected by Poisson

sampling, it generates - CSR pattern. If both coordinates are selected

by Markov Process - sampling, it generates aggregated pattern.

- Spatial process observed at these locations

determines the original - process uniquely

- Study region Discrete

- Adopt Bernoulli sampling or Markov sampling

- Deshmukh (2003), JISA (Adke Special volume)

- Prayag Deshmukh (2000) Environmetrics

- Test for CSR against aggregated pattern

17

18

- Suppose X has negative binomial distribution

- Pk X x (x k -1)C(k-1) pk qx-k , x

0, 1, ,

- p known, k ? I,

- not a one parameter exponential family

- Complete

- Strongly complete

19

- Risk models in insurance

- U (t) reserve/ value of the fund/ insurers

surplus at time t

- U (t) initial capital input via premiums by

time t output due to claims by t

- S (t) Output due to claim payments by t 0?t

X(u) du, random part

- Probability of ruin P U (t) lt 0

- Distribution of S (t) or its discrete version

Sn S Xi, i running from 1 to n

- Observed data are the claim amounts in various

time periods - weeks or months

- Uk S Xi, i runs from 1 to Nk, Nk is the

frequency of a claim in a fixed time period, - and Xi denotes the claim amount, Nk and Xi are

random.

- If Nk 0, Uk 0

- Nk Poisson, negative binomial

20

- Tk, k 1, Tk Tk-1 are distributed as Nk

with support I

- Uk S(Tk) S(Tk-1)

- Observed data are realization of the process S

(Tn), n 1, a process observed - at random epochs

- On the basis of these data we wish to study the

process Sn, n 1

- Identifiability of the random sampling scheme.

- If Sn is modelled as a renewal process then

identifiability of the random - sampling scheme is valid for any discrete

distribution of Nn with support I . - (Teke Deshmukh,2008, SPL)

- If Sn is a discrete parameter process then

identifiability of the random - sampling scheme is valid for negative

binomial distribution of Nn

- Strong completeness of the family of negative

binomial distributions helps - to prove identifiability

21

Sn , n ? 1 Renewal process, f(s) L.T.

Renewal processes

Cox process

Tn , n ? 1 Renewal process Support N, P(s)

p.g.f.

Zn S(Tn), Renewal process

?

g(s) L.T. g(s) P(f(s)) f(s)

P-1(g(s)) Inversion formula Zn determines

Sn gn(s) Empirical L.T. fn(s) P-1(gn(s))

Cox process

Renewal processes

P(s) Geometric, Shifted geometric

Sn , n ? 1 Random walk S(t) , t ? 0 Levy

process

P(s) Geometric,Poisson negative Binomial,

both truncated at zero Bernstein, Stieltjes

22

Work in progress

- X(t), t ? T Original process under study

- Zn X(Tn), Tn, n 1 Renewal process

G1 G2 implies EF1(L1, L1L2, ,

L1L2Ln) EF2(L1, L1L2, ,

L1L2Ln) EF1(L1, L1L2, , L1Ln)- F2(L1,

L1L2, , L1Ln) 0

Lj sum of kj iid random variables, if the

joint distribution of (L1, L2,,Ln) is complete

then, G1 G2 implies F1 F2.

f(x, k), k ? I family of L

S d (1 d) k 1( ? h(x) f(x,k)dx) 0, sum

being taken on I ? ? h(x) S (1 d)k f(x,k)

0 ? ? h(x) A(x, d) 0, A(x, d) S

(1 d)k f(x,k) Can we conclude that h(x) 0

a.s.?

23

References 1.Baba, Y. (1982). Maximum likelihood

estimation of parameters in birth and death

process by Poisson sampling, J. Oper. Res. 15,

99-111. 2. Basawa, I.V. (1974). Maximum

likelihood estimation of parameters in renewal

and Markov renewal processes. Austral. J.

Statist. 16, 33-43. 3.Cressie, N. A. C. (1993).

Statistics for Spatial Data, Wiley, New

York. 4.Deshmukh, S.R. (1991). Bernoulli

sampling, Austral. J. Statist. 33, 167-176.

5.Deshmukh, S.R. (2000). Markov sampling, Aust.

N. Z.J. Statist. 42(3), 337-345. 6.Deshmukh,

S.R. (2003). Identifiable sampling design for

spatial process. J. Ind.

Statist. Assoc. 41(2) 261-274. 7.Deshmukh, S.R.

(2005). Markov Arrivals See Time Averages,

Stochastic Modelling and Applications.

Vol. 8, 2, p. 1-20.

24

8.Kingman, J.F.C. (1963). Poisson counts for

random sequences of events. Ann.

Math. Statist. 34, 1217-1232. 9.Prakasa Rao,

B.L.S. (1988). Statistical inference from sampled

data for stochastic process. Contemp. Math. 80,

249-284. 10. Prayag, V.R. Deshmukh, S.R.

(2000). Testing randomness of spatial pattern

using Eberhardts index, Environmetrics, Vol. 11,

p. 571-582. 11.Su, Y. and Cambanis, S. (1993).

Sampling designs for estimation of a random

process. Stochastic Process Appl. 46,

47-89. 12.Teke S.P. Deshmukh, S.R.(2008) .

Inverse Thinning of Cox and Renewal Processes,

Statistics and Probability Letters, 78, p.

2705-2708.

25

Thank You

Recommended

CrystalGraphics Presentations