From Financial Statement to Business Analysis - PowerPoint PPT Presentation

1 / 21

Title:

From Financial Statement to Business Analysis

Description:

Income statement: operating performance during a time period ... The Airline Industry ... once they have accumulated 25,000 miles of travel with the same airline. ... – PowerPoint PPT presentation

Number of Views:20

Avg rating:3.0/5.0

Title: From Financial Statement to Business Analysis

1

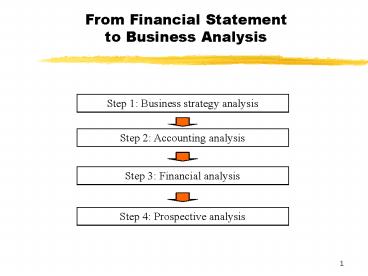

From Financial Statementto Business Analysis

Step 1 Business strategy analysis

Step 2 Accounting analysis

Step 3 Financial analysis

Step 4 Prospective analysis

2

Financial Accounting Analysis

Financial Analysis

Accounting Analysis

Financial Statement

Unbiased Accounting

Recasting Financial Statement firms could adopt

different classifications

3

Financial statements

- Four documents

- Income statement operating performance during a

time period - Balance sheet assets and how they are financed

- Cash flow statement level of the cash flow

gerated by the firm - Statement of changes in equity outlines the

sources of changes in equity during the period

between consecutive balance sheets.

4

Accrual Accounting

Fundamental features of corporate financial

reports

Recording of economic transactions

On the basis of expected cash receipt and payments

Not necessarily actual

5

Income statement

Expenses

Revenues

economic resources

economic resources

earned during

used up in

a time period

realization principle

matching and conservatism principle

Profit revenues - expenses

6

Balance sheet

Liabilities

Assets

economic obbligations arising from past benefit

economic resources owned by a firm

future economic benefit

met with reasonable certainty

measurable with reasonable certainty

time reasonably well defined

Equity assets - liabilities

7

Delegation of reporting to management

Corporate managers

accounting discretion

intimate knowledge of firms businesses

management manipulation of accounting numbers

Benefits

Costs

preserved

reduced

Accounting rules and auditing

8

Accounting analysis

Identify key accounting policies (1)

Evaluate accounting strategy (3)

Assess accounting flexibility (2)

Six steps to evaluate a firms accounting quality

Evaluate the quality of disclosure (4)

Identify potential red flags (5)

Undo accounting distortions (6)

9

Accounting analysis

Identify key accounting policies (1)

Business strategy analysis

- How well the success factors and risks are being

managed by the firm - Bank interest and credit risk management

- Retail inventory management

- Pharmaceuticals research and development

Accounting measures

Business events

10

Accounting analysis

Assess accounting flexibility (2)

- Expense or capitalize costs

- Estimate expected defaults on loans

- Estimate long-terms projects

- Depreciation policy (straight.line or accelerated

methods) - Inventory accounting policy (LIFO, FIFO, or

average cost)

More flexibility

Trade Off

Less flexibility

11

Accounting analysis

Evaluate accounting strategy (3)

- How do the firms accounting policies compare to

the norms in the industry? - Do managers face strong incentives to use

accounting discretion to manage earnings? (tax

policy) - What is the impact of the changes in policies?

(warranty expenses) - Have the companys policies and estimates been

realistic in the past?

12

Accounting analysis

- Does the company provide adequate disclosure to

assess the firms business strategy and its

economic consequences? (industry condition,

competitive position, plans for the future) - Does the firm adequately explain its current

performance? (financial notes) - Does the firm provide adequate additional

disclosure to help outsiders understand how key

success factors are being managed? (decrasing in

profit) - If a firm is in multiple business segments, what

is the quality of segment disclosure? - How forthcoming is the management with respect to

bad news? - How good is the firms investor program?

Evaluate the quality of disclosure (4)

13

Accounting analysis

- Certain items must be examined more closely

- Unexplained changes in accounting, especially

when performance is poor - Unexplained transaction that boost profits

- Unusual increases in trade receivables in

relation to sales increases - Unusual increases in inventories in relation to

sales increases - An increasing gap between a firms reported

profit and its cash flow from operations - An increasing gap between a firms reported

profit anche its tax profit - Unexpected large asset write-offs

- Large year-end adjustments

- Qualified audit opinions or changes in

independent auditors that are not well justified - Poor internal governance mechanisms

Identify potential red flags (5)

14

Accounting analysis

- Restate numbers to reduce the distortion to the

extent possible - Impossibility to perfectly undo the distortion

using outside information alone - Use the cash flow statement and the notes to the

financial statements - Use the tax notes

Undo accounting distortions (6)

15

Accounting analysis pitfalls

Potential pitfalls and common misconceptions

Conservative accounting is not the same as good

accounting

Not all unusual accounting is questionable

An accounting choice might be justified if the

companys business is unusual

The financial statement users want to evaluate

how well a firms accounting captures business

reality in a unbaised manner and conservative

accounting can be as misleading as aggressive

accounting in this respecy

16

Accounting analysis

The Airline Industry Most airlines have frequent

flyer programs that promise customers free

flights once they have accumulated 25,000 miles

of travel with the same airline. How should these

programs be reflected in the airlinesfinancial

statements?

17

Accounting analysis

Liabilities

Promises that require future expenditure

economic obbligation arising from past benefit

ticket sales in the past

met with reasonable certainty

for example 1.2 milion free trips

within 3 to 5 years after the revenue ticket

sales are made

time reasonably well defined

Balance sheet

18

Accounting analysis

Expenses

cost associated

Free-trip tickets in the future

with benefit that are comsumed in this time period

increase in revenue ticket sales

matching concept

- Administrative cost

- Costs related to the flight

- Opportunity cost

Income statement

19

Implement accounting analysis

Process

Analyst

Accounting Analysis

Undo distortions

Balance Sheet

Adjustments to the financial statement

Income Statement (revenue/expenses)

20

Implement accounting analysis

RECASTING FINANCIAL STATEMENT

DIFFERENCES

Nomenclature

Classifications

Formats

New Template

Time-series cross sectional comparison

21

Implement accounting analysis

Different format

IFRS format for operating expenses

By nature

By function

Cause

Purpose

- Cost of materials - Cost of personnel - Cost

of non current assets

- - Cost of sold

- SGA (selling,

- General

- Administrative)

Recast using Financial Notes