International Accounting - PowerPoint PPT Presentation

1 / 10

Title:

International Accounting

Description:

FASB #52(new) : current method can be used if. Functional Currency: ... FASB# 52 !! International Tax Management. Importance of tax management : ... – PowerPoint PPT presentation

Number of Views:28

Avg rating:3.0/5.0

Title: International Accounting

1

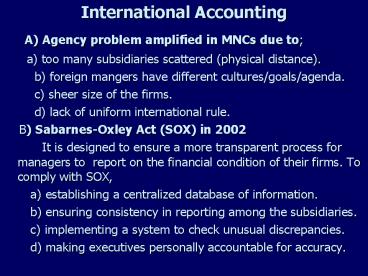

- International Accounting

- A) Agency problem amplified in MNCs due to

- a) too many subsidiaries scattered

(physical distance). - b) foreign mangers have different

cultures/goals/agenda. - c) sheer size of the firms.

- d) lack of uniform international rule.

- B) Sabarnes-Oxley Act (SOX) in 2002

- It is designed to ensure a more

transparent process for managers to report on

the financial condition of their firms. To comply

with SOX, - a) establishing a centralized database of

information. - b) ensuring consistency in reporting among

the subsidiaries. - c) implementing a system to check unusual

discrepancies. - d) making executives personally

accountable for accuracy.

2

- C) 2 steps in financial reporting

- 1) Translation

- a)

- b)

- 2) Consolidation

- Prepare one F/S for the whole MNC.

3

- D) Translation Methods

- Current Temporal

- B/S All ( )

Monetary(cash,A/R, A/P) - except equity ( )

( ) -

Non-monetary(F/A,Inv.,Eqty) - ( )

- I/S All ( )

CGS Dep. ( ) -

others ( ) - Translation

- gain/loss Balance sheet Income

statement - ( )

( )

4

- D) Rules for translation

- FASB 8 (old) all temporal method.

- Problem 1.

- 2.

- FASB 52(new) current method can be used

if - (

) . - Functional Currency

- Most of the MNCs can use current method under

- FASB 52 !!

5

- International Tax Management

- Importance of tax management

- 1) the location 2) business mode

- 3) financing source 4) investment decision

- MNCs are exposed to risk of double taxation

because each - country has different philosophy/method to

impose tax.

6

- Intl Tax Management

- 2 principles of taxation on foreign sourced

income. - 1) Tax Credit

- designed to (

) - ( Domestic tax liability of U.S. firm is

reduced by the -

!! ). - 2) Tax Deferral

- designed to (

) - (Collection of tax on foreign income will be

delayed until -

!! ).

7

- Two types of foreign operation

- Branch

Subsidiary - Legal unincorporated unit created under

foreign law - ( )

( ) - Income immediately taxed delayed until

remitted - tax ( )

( ) - Loss

- Which one would be better if they have loss?

- Which one would be better if they have income?

- What can be the best way to minimize tax

liability?

8

- Many MNCs abused subsidiary as a tool to

- avoid U.S. tax by creating a paper

- company in ( )

country. -

- Two types of F. Subsidiary

- 1. Non controlled F.S

- a. U.S. partner is minority stock holder.

- b. Tax deferral applied (

) - 2. Controlled F.S.

- a. U.S. partner is majority stock holder.

- b. Income will be more scrutinized.

- (

)

paper co.

FS

A

B

FS

FS

Parent in US

9

- Income generated by controlled foreign sub.

- to be classified as

- a) Active income Normal business income

- b) Passive income Abnormal/suspicious income

- resulted

from tax evasive -

maneuvering (such as -

).

10

- ( Application of Tax Deferral )

- Foreign Operation

- Branch Subsidiary

- Non

- Controlled

Controlled - Active Passive

Recommended

CrystalGraphics Presentations