Alternative Methods for Assigning Overhead Costs - PowerPoint PPT Presentation

1 / 21

Title:

Alternative Methods for Assigning Overhead Costs

Description:

To maintain the restaurant (facility) ... Maintaining equipment. Recording plant depreciation. Steps for Activity Based Costing (ABC) ... – PowerPoint PPT presentation

Number of Views:48

Avg rating:3.0/5.0

Title: Alternative Methods for Assigning Overhead Costs

1

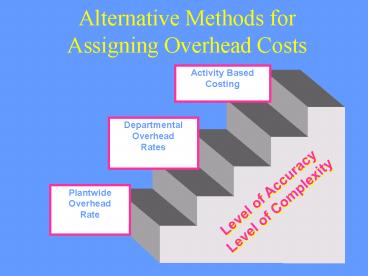

Alternative Methods for Assigning Overhead Costs

Activity Based Costing

Departmental Overhead Rates

Level of Accuracy Level of Complexity

Plantwide Overhead Rate

2

Symptoms of an outdated cost system.

- The outcome of bids is difficult to explain.

- Competitor's prices appear unrealistically low.

- Operational managers want to drop products that

appear profitable. - Profit margins are hard to explain.

- The company has a highly profitable niche all

to itself. - Customers do not complain about price increases.

- Some departments are using their own accounting

system.

3

Traditional cost systems

- Departmental or plant-wide OH rates.

- Tend to rely on unit-level cost drivers.

- Most common is direct labor hours.

- Assigns more cost to high-volume products.

- Ignores other factors such as design complexity

and product diversity. - As a result, complex low-volume products are

likely to be subsidized by high-volume products.

4

Consider the following two restaurants.

- One does a high-volume lunch business by limiting

the menu to a salad/soup bar and choice of five

sandwiches. - The second serves fewer customers, but has

excellent service and a wide menu selection. - The restaraunts are similar in size and are

located in the same area. - Which restaraunt is likely to be more costly to

operate? Why?

5

ABC/ABM

- Activities are the root cause of costs.

- Not all activities relate simply to the number of

units produced. - Need both unit and non-unit level cost drivers.

- Products/customers consume the activities.

- Get more accurate info by assigning cost based on

activities required (ABC). - To manage cost, we must reduce the consumption of

the costly activities (ABM).

6

Coopers Hierarchy of Activities

Activities performed to sustain the

organizations existence.

Facility sustaining

Activities performed to develop or support

product lines, but not specific units or batches.

Product sustaining

Activities performed for a group of

units/customers.

Batch level

Activities performed for each individual

unit/customer.

Unit level

7

Restaurant example continued

- Can you think of activities performed

- For each customer (unit)?

- For groups of customers (batch)?

- To develop/support menu items (product)?

- To maintain the restaurant (facility)?

8

Classify the following activities as unit, batch,

product or facility and suggest an appropriate

cost driver.

- Receiving raw material for production.

- Setting up production equipment.

- Machining the product.

- Assembling the product.

- Inspecting the product for quality.

- Shipping the product.

- Advertising the product.

- Maintaining equipment.

- Recording plant depreciation.

9

Steps for Activity Based Costing (ABC)

- 1. Identify the activities.

- 2. Combine activities into homogenous

- cost pools.

- 3. Select activity (cost) driver for each

- pool and calculate the activity rate.

- 4. Assign cost to products using activity

- rates or consumption ratios.

10

Activity Identification

Activity Inventory What activities are

performed?

1. Develop test programs 2. Make probe cards 3.

Test products 4. Set-up lots 5. Collect

engineering data 6. Move water lots 7. Insert

dies 8. Provide utilities 9. Provide space 10.

Purchase materials 11. Receive materials 12. Pay

for materials

Could be 200-300 activities, depending on the

size of the firm.

Where does this information come from?

11

Form Homogenous Cost Pools

Overhead Cost

Activity pool 3

Activity pool 1

Activity pool 2

Why do we need to combine activities into

pools? How many cost pools do we need? When can

you combine activities together?

12

Select an Activity Driver for Each Pool and

Calculate an Activity Rate

Overhead Cost

Activity pool 1 Setups

Activity pool 2 Machine hours

Activity pool 3 Engineering changes

Activity Cost of the Activity Rate

Activity Driver

Ex. 100,000 in pool 1 for 100 total set-ups.

13

Assign Overhead Cost to Products Using

Activity Rates or Consumption Ratios

Overhead Cost

Activity pool 1 Setups

Activity pool 2 machine hours

Activity pool 3 Engineering changes

Product A

Product B

Product B requires 40

setups.

Product A requires 60 setups.

14

A Traditional Costing Example

- Total overhead costs of 775,000 are currently

applied to product lines on the basis of direct

labor hours.

Product

Product Product

Line 1 Line 2 Line 3

Units produced 100,000 200,000

150,000 Direct labor hours

2,000 3,500

2,250 Total Overhead Cost

? ?

? Overhead Cost Per Unit ?

? ?

Calculate the overhead cost per unit.

15

Unit Overhead Cost Using Plantwide Rate

Predetermined Overhead Rate 775,000/7,750

direct labor hours

100 per direct labor hour

Unit Cost Using Plantwide Rate

Unit Cost Product Line 1 (2,000 dlh x 100)

200,000/100,000

2.00 Unit Cost Product Line 2 (3,500 dlh x

100) 350,000/200,000

1.75 Unit Cost Product Line 3 (2,250 dlh x

100) 225,000/150,000

1.50

16

An ABC Example

An ABC study revealed that the following

activities as the underlying cause of overhead

costs. 1. Writing Test Programs for Products

200,000 2. Making Circuit Boards (with

machines) 120,000 3. Setting-up Machines

175,000 4. Inserting Components

100,000 5. Providing Space

50,000 6. Utility Cost

130,000

Total Overhead 775,000

Are these unit, batch, product or facility level

activities?

17

An ABC Example (Continued)

Product

Product Product Operational Data Line

1 Line 2 Line 3 Units produced

100,000 200,000

150,000 Number of batches 200

300 600

Machine hours 5,000

6,000 4,000 Number of

products 150

50 200 Square feet of space

5,000 7,000

6,000 Direct labor hours

2,000 3,500 2,250

How many cost pools do we need? Select a

driver for each pool.

18

Forming Cost Pools and Selecting Drivers

775,000

Writing Prog. Making /Ins.

Setups

Space/Util. 200,000 220,000

175,000

180,000

Products Machine hours

Batches Square feet

Activity Drivers

Product Product

Product Line 1

Line 2 Line 3

19

Calculating Activity Rates for Each Cost Pool

Cost Driver Activity

Activity Pool Level Amount

Driver Rate

Writing Prog. Products 200,000 400

products 500 product Making/Ins. Units

220,000 15,000 M. H.

14.67/M. H. Setup Batch

175,000 1,100 batches

159.09/batch Space/Util. Facility

180,000 18,000 sq.. feet 10/sq. foot

20

Assigning Cost to Product Lines

Cost Product Product

Product Pool Line 1

Line 2 Line 3 Total

Writing Prog. 75,000 25,000

100,000 200,000 Making/Ins. 73,350

88,020 58,630

220,000 Setup 31,818

47,727 95,455 175,000 Space/Util.

50,000 70,000

60,000 180,000 Total

230,168 230,747 314,085

775,000

Unit Cost Product Line 1 230,168/100,000 units

2.30/unit Unit Cost Product Line 2

230,747/200,000 units 1.15/unit Unit Cost

Product Line 3 314,085/150,000 units

2.09/unit

21

Comparison of ABC and Conventional Costing

Unit Cost ABC Unit Cost Plantwide

Product Line 1 2.30

2.00 Product Line 2 1.15

1.75 Product Line 3

2.09 1.50

Rule-of-thumb Conventional cost systems

tend to over-cost high

volume products and under-cost low volume

items. (Please note

implications for product line 2.)

Recommended

CrystalGraphics Presentations