Depreciation - PowerPoint PPT Presentation

1 / 10

Title:

Depreciation

Description:

allowed rates by ATO have diminishing value rate 25% higher then prime cost rate ... regularly updated by ATO. Dr Alan J. R. Smith. Mechanical and Manufacturing ... – PowerPoint PPT presentation

Number of Views:97

Avg rating:3.0/5.0

Title: Depreciation

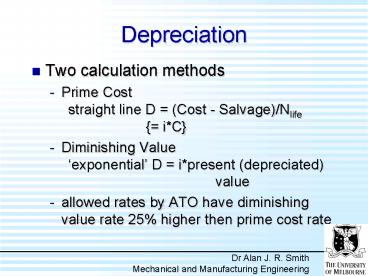

1

Depreciation

- Two calculation methods

- Prime Cost straight line D (Cost -

Salvage)/Nlife iC - Diminishing Value exponential D ipresent

(depreciated) value - allowed rates by ATO have diminishing value rate

25 higher then prime cost rate

Dr Alan J. R. Smith Mechanical and Manufacturing

Engineering

2

Depreciation

- Taxpayers are able to self assess their own

effective life for assets but many choose to use

the 'safe harbour' rates published by the Tax

Office - ATO 17th May 2000 - typical values (prime cost) were motor vehicles

22.5, plant 7.5, office equipment 15,

electronic equipment 33, buildings 4 - regularly updated by ATO

Dr Alan J. R. Smith Mechanical and Manufacturing

Engineering

3

Depreciation

- Remember depreciation money is still in the

company and unless spent, increases the cash

available for company purposes. - For uniform trading conditions, the real cash

gain for a firm is the profit plus depreciation

less dividend or net repayments of capital made

from the profit and loss appropriation or capital

accounts during the period.

Dr Alan J. R. Smith Mechanical and Manufacturing

Engineering

4

Budgeting

- Necessary (financial) planning

- For public service and for sections within a

company, it can simply involve the division of an

allocation of funds - For charities and other not-for-profit

organisations, it can mean estimating the

(annual) expected income then determining the

annual expenditure

5

Budgeting

- For commercial enterprises, there is also the

need to be concerned with cash flow - it is not sufficient to ensure a profit is made

at the end of the year - need to be able to pay all bills as they fall

due, esp. wages and utilities - A budget allows estimates to be made of any loans

that may be necessary IN ADVANCE

6

Budgeting

- A budget is a PLAN and as such may change during

the year - this should not be an excuse for not taking the

budgeting process seriously - this should not be an excuse for ignoring the

budget

7

Profit Loss Budget

Business Plan

Advertising Budget

Sales Plan

Distribution Budget

Revenue Budget

Prodn Admin Plan

Labour Plan

Equipment Plan

Capital Budget

8

- In practice companies will have a number of

budgets informed by various plans - Business plan informs the sales plan

- Sales plan informs the operations plan and the

advertising and distribution budgets - Operations plan informs the labour plan and

equipment plan - Revenue budget is based on the advertising

distribution budgets and labour plan - Capital budget depends on the distribution

budget and equipment plan

9

Budgetary Control

- A system of managing a business by making

forecasts of the different activities and

applying a financial value to each

forecast. Actual performance is subsequently

compared with the estimates.

10

Budgeting

- Because a number of costs (and revenue) are

dependent on sales, it can be more useful to use

a flex budget - Variable costs are expressed as percentages of

the budget case for 100 sales - e.g. if sales are above budget by 10 then it is

reasonable to expect raw materials to also be

above budget by about 10

Recommended

CrystalGraphics Presentations

![[DOWNLOAD]PDF The Economics of Inflation - A Study of Currency Depreciation in Post War PowerPoint PPT Presentation](https://s3.amazonaws.com/images.powershow.com/10087131.th0.jpg?_=20240727028)

![[PDF]DOWNLOAD The Economics of Inflation - A Study of Currency Depreciation in Post War PowerPoint PPT Presentation](https://s3.amazonaws.com/images.powershow.com/10088272.th0.jpg?_=202407301210)

![[DOWNLOAD]PDF The Economics of Inflation - A Study of Currency Depreciation in Post War PowerPoint PPT Presentation](https://s3.amazonaws.com/images.powershow.com/10088273.th0.jpg?_=202407301211)