Income Statement - PowerPoint PPT Presentation

1 / 43

Title:

Income Statement

Description:

If a firm buy and sell, or produce and sell, products, the net assets that ... You have earned the money because I took the car. But you have not received the cash. ... – PowerPoint PPT presentation

Number of Views:40

Avg rating:3.0/5.0

Title: Income Statement

1

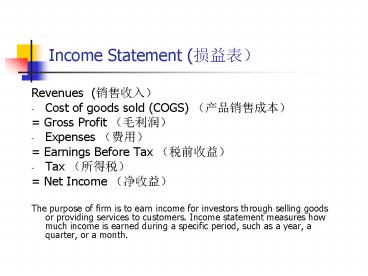

Income Statement (???)

- Revenues (????)

- Cost of goods sold (COGS) (??????)

- Gross Profit (???)

- Expenses (??)

- Earnings Before Tax (????)

- Tax (???)

- Net Income (???)

- The purpose of firm is to earn income for

investors through selling goods or providing

services to customers. Income statement measures

how much income is earned during a specific

period, such as a year, a quarter, or a month.

2

(No Transcript)

3

Definitions

4

Ledger (T- Account) treatment of income statement

accounts

- Revenues

- Gains

- Expenses (inc. COGS)

- Loss

- Dividends

5

(No Transcript)

6

Cash Accounting (?????)

- Revenues recognized at the time that cash is

received - Expenses recognized at the time that cash is

disbursed - Note Cash received from and disbursed (??) to

shareholders and creditors(???) is neither

revenues nor expenses, and does not enter income

statement under cash accounting - An example A toy retailer starts business on

November 1, 19x0, He pays two months rent on his

store, 2,000, on that day, and also purchases

and pay for 35,000 toys. However, he sells

nothing in November. In December, he sells all

the toys with a sales price of 40,000 and

collects 5,000 in cash

7

Cash Accounting Income Statement

8

Problems with Cash Accounting

- Mismatch the cost of efforts (expenses) with the

output of the efforts (revenues) - Delay recognition of revenues

- Provide opportunities to manage earnings

9

Accrual Accounting (?????????)

- Revenue recognition

- follow realization principle (????)

- 1) A firm has performed all, or most of, the

services it expects to provide - 2) The firm has received cash or some other

assets capable of reasonably precise measurement,

such as account receivables

10

Accrual Accounting

- Expense recognition

- When an asset is used directly to generate

revenues, the used asset becomes expense. E.g.,

Amazon.com sold books, the cost to purchase the

sold books become COGS, a part of expenses. This

is called matching principle(????) of accounting. - When an used asset is indirectly related to the

current, and only the current, period revenues,

we treat the used asset as expense. E.g., cash to

pay for advertisement, salary for the CEO. - When an asset is used to benefit both the current

and the future period, the benefit, nevertheless,

not matter current or future, is hard to identify

and measure, we treat the used asset as expense.

E.g., cash used to pay research and development

for pharmaceutical companies. This is

conservative principle(????) of accounting.

11

Accrual Accounting Income Statement

12

Adjusting Journal Entries Under Accrual Accounting

- Under accrual accounting, some journal entries

are not explicitly related to a transaction. We

make these entries, adjusting journal entries,

most likely at the end of an accounting period. - There are four types of adjusting entries

- Unearned revenue (?????)

- Accrued Revenue(????)

- Prepaid expense(????)

- Accrued expense(????)

13

Unearned Revenue

- Example Suppose you are the accountant of

Guanghua and Guanghuas policy is to

proportionately return student tuitions whenever

a student chooses to quit school (not a bad act,

Bill Gates quitted Harvard). So on September 1,

2002, you paid 80,000 to Guanghua for two-year

tuitions. - Receive cash

recognize revenue

14

Unearned Revenue

- On Sep. 1, 2002, although Guanghua received the

cash, to it, the cash received is unearned

revenue. That is, Guanghua has not provided you

educational service yet. Guanghuas journal

entry - Dr. Cash 80,000

- Cr. Unearned Revenue (liability) 80,000

- On Dec. 31, 2002, after you have spent half a

year at Guanghua to enjoy its superb service,

Guanghua has earned one-fourth of the tuitions.

Journal entry - Dr. Unearned Revenue 20,000

- Cr. Revenue 20,000

15

Accrued Revenue

- Example If you are a manufacture of cars and I

bought a car from you on Nov. 12, 2002 for

3,000, but we agree that I pay you next year.

You have earned the money because I took the car.

But you have not received the cash. Still, it is

your money and your revenue. - Dr. Account Receivable 3,000

- Cr. Revenue 3,000

- Recognize revenue Receive

cash

16

Prepaid expense

- Example, back to the Guanghua case, from your

point of view, the 80,000 is prepaid expense.

That is, if on Sep. 2, 2002, you want to quit

school, you will get money back (if you want to

try this, please do so before or after my

course). That is, you still own the money. - Pay cash

recognize expense

17

Prepaid expense

- On Sep. 1, 2002, your account

- Dr. Prepaid tuitions 80,000

- Cr. Cash 80,000

- On Dec. 31, 2002, you

- Dr. Tuition expense 20,000

- Cr. Prepaid expense 20,000

- If you quit school on this day, you get 60,000

back from the school.

18

Accrued Expense

- Example, you worked for your company in December

2002, and your company will pay your salary of

3,000 of December in January 2003. But to the

company, expense has incurred in 2002, although

cash is not paid in December of 2002. So the

company - Dr. Expense 3,000

- Cr. Salary payable 3,000

- recognize expense pay cash

19

The Final Stages of the Accounting Process (refer

to a premier on accounting handout)

- On Dec. 31 of the year, the accountants finished

all journal entries, posted to ledger

(T-accounts), calculated the balance (??)of every

ledger account, and did a trial balance. Now

she/he does adjusted journal entries, and then

posts to ledger again, and does an adjusted trial

balance. - What she/he has in hands now is a list of

accounts. Next - Prepare income statement

- Close income statement accounts to retained

earnings account - Prepare balance sheet

- Q.E.D

20

Expensing(???) vs. Capitalization (???) of

Expenditures(??)

- A firm pays employee salaries, we say the firm

expense employee salary - Expensed expenditures go to income statement

- Expensed expenditures help generate revenues in

current period - If a firm expenses the expenditure, current

earnings will be lower by that amount

- A firm buy a building, we say the firm capitalize

the building as asset. - Capitalized expenditures go to balance sheet

- Capitalized expenditures help generate revenues

in current and future periods - If a firm capitalizes the expenditure, current

earnings will not be lowered by that amount

21

Expensing vs. Capitalization of Expenditures

- But life is not so simple and straightforward.

Sometimes it is difficult to determine whether

the expenditures benefit future periods, and if

it benefits future periods, it is difficult to

determine which future period will benefit.

Therefore, firms expense some expenditures that

may otherwise be capitalized. This is a

conservative treatment of the expenditures by

GAAP. - Marketing expenditures

- Research and Development

- Stock options

22

The Worldcom scandal

- June 26, 2002, Worldcom reports it overstated

earnings by 3.8 billion in the past few years.

It quickly asked for chapter 11 protection - What did they do? Capitalize expenditures that

should have been expensed. That is, 3.8 billion

should not be on balance sheet, but go through

income statement as expense. - In 2001, the company reports earnings of 1.4

billion, which should have been a loss year.

23

(No Transcript)

24

(No Transcript)

25

The relation between balance sheet and income

statement

- Assets Liabilities Equity

- Equity Contributed capital(??) Retained

Earnings (RE) - Ending(????) RE Beginning (????)RE Net Income

Dividends - Net Income Revenues Expenses

- A L Contributed capital Beginning RE

(Revenues Expenses) Dividends - Therefore, revenues increase assets and equity

- expenses decreases assets and equity

26

Time Series analysis of common-size income

statement

27

Cross section analysis (????)of common-size

income statement

28

Growth analysis of income statement

29

(No Transcript)

30

(No Transcript)

31

A few items on I/S explained

- Cost of revenues Cost of goods sold (COGS)

- Sales and Marketing

- Selling, general and administrative

- Product development

- Depreciation and amortization

- Operating income or income from operation

- Extraordinary item unusual and infrequent

- Net Income

- Earnings per share-primary

- Earnings per share-diluted

- Earnings per share-end of year number of shares,

or average number of shares? - Pro Forma earnings As if earnings

32

AOL 2000

33

AOL 2000

34

Earnings Management-Why

- For managers earnings-based bonus

- For shareholders earnings-based bond covenant

- For the company

- Better IPO price(???????)

- Avoid government regulation

- Avoid paying employee high salaries

35

Earnings Management-How

- Accelerate or delay revenues

- Accelerate or delay expenses

- Take one-time gains or charges big bath

36

Earnings management Who gain, who lose?

- Enron case

- Worldcom case

37

Who Lose?

38

Who lose?

Life Sentence

39

How to detect earnings management?

Time-series analysis Cross-Sectional

analysis Growth analysis As long as ratios are

out of step with peers or trends, there is

reason for suspicion.

40

Price-to-earnings ratio P/E

- P/E is a ready yardstick for valuation

- Use comparable firms P/E to price IPO stocks

- P/E is a rough indicator of relative

over-valuation or under-valuation - Average P/E ratio of all stocks on a market

indicates the level of valuation of the market

41

P/E anomaly

- High P/E stocks (glamour stocks, growth stocks)

earn lower return in the one-year-ahead period

low P/E stocks (value stocks) earn higher stock

returns in the same period. The return

differential is not explained by risk. - Fama and French Journal of Finance 1992, the

numbers are monthly return in percentage

42

Caveats(??) in using P/E in valuation

- Negative earnings can not be used in computing

P/E - Earnings contain transitory (???) items, or

one-time items that drive P/E up or down

temporarily - P/E ratio is meaningful only when earnings come

from normal, repetitive operation - In investing community, people use different

earnings to compute P/E, lag earnings, lead

earnings, average earnings

43

Investing Motto

- Financial Statement is like bikini, what it

reveals is interesting, but what it conceals it

vital. - Burton G. Malkiel ltA random walk down wall streetgt

Recommended

CrystalGraphics Presentations