Chapter 2: An Overview of the Financial System - PowerPoint PPT Presentation

1 / 8

Title:

Chapter 2: An Overview of the Financial System

Description:

Short term (maturity 1 year), Intermediate term (1 maturity 10 years) Long ... Money Market market for short-term debt instruments ... – PowerPoint PPT presentation

Number of Views:785

Avg rating:3.0/5.0

Title: Chapter 2: An Overview of the Financial System

1

Chapter 2 An Overview of the Financial System

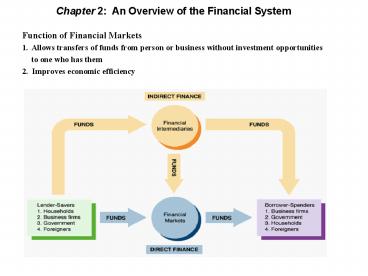

- Function of Financial Markets

- 1. Allows transfers of funds from person or

business without investment opportunities - to one who has them

- 2. Improves economic efficiency

2

Financial Markets

- Classifications A firm or an individual can

obtain funds in a financial market in two ways - 1. Debt Markets

- Short term (maturity lt 1 year), Intermediate

term (1ltmaturity lt 10 years) Long-term (maturity

gt 10 year) - Money Market market for short-term debt

instruments - Capital Market market for intermediate- and

long-term debt instruments - No ownership for debt holders.

- 2. Equity Markets

- Common stocks

- Confer ownership rights on the equity

holders. - The equity holders benefit directly from any

increases in the corporations profitability or

asset value. - The corporation must pay all its debt holders

before it pays its equity holders.

3

Another Classifications of Financial Markets

- 1. Primary Market

- New security issues sold to initial buyers

(investment banks underwriting securities). - 2. Secondary Market

- Securities previously issued are bought and sold

(e.g., NYSE/AMEX, NASDAQ) - Secondary markets do not help the corporations to

acquire funds, but do increase the liquidity of

the securities, which makes the securities in the

primary markets more attractive. - Secondary markets also determine the prices of

the securities issued in the primary market. - Secondary market can be organized in two ways

- 1) Exchanges

- Trades conducted in central locations (e.g., New

York Stock Exchange) - 2) Over-the-Counter Markets

- Dealers at different locations buy and sell

(e.g., NASDAQ)

4

Internationalization of Financial Markets

- International Bond Market

- 1. Foreign bonds (sold in a foreign country,

denominated in that countrys currency). - 2. Eurobonds (sold in a country but denominated

in a currency other than that of the country).

Now larger than U.S. corporate bond market. - a variant Eurocurrencies foreign currencies

deposited in banks outside the home country.

(e.g., Eurodollars) - nothing to do with euros.

- World Stock Markets

- U.S. stock markets are no longer always the

largest Japan sometimes larger

5

Indirect Finance Financial Intermediaries

- Financial Intermediaries

- More important source of finance than

securities markets - Needed because of transactions costs and

asymmetric information - Functions of Financial Intermediaries

- Financial intermediaries make profits by reducing

transactions costs. Reduce transactions costs by

developing expertise and taking advantage of

economies of scale. - Risk Sharing Create and sell assets with low

risk characteristics and then use the funds to

buy assets with more risk (also called asset

transformation). - Also lower risk by helping people to diversify

portfolios - Financial intermediaries reduce adverse selection

and moral hazard problems, enabling them to make

profits.

6

Asymmetric Information Adverse Selection and

Moral Hazard

- Adverse Selection

- 1. Before transaction occurs

- 2. Potential borrowers most likely to produce

adverse outcomes are ones most likely to seek

loans and be selected - Moral Hazard

- 1. After transaction occurs

- 2. Hazard that borrower has incentives to engage

in undesirable (immoral) activities making it

more likely that wont pay loan back

7

Financial Intermediaries

8

Regulation of Financial Markets

- Three Main Reasons for Regulation

- 1. Increase information to investors

- A. Decreases adverse selection and moral hazard

problems - B. SEC forces corporations to disclose

information - 2. Ensuring the soundness of financial

intermediaries - A. Prevents financial panics

- B. Chartering, reporting requirements,

restrictions on assets and activities, deposit

insurance, and anti-competitive measures - 3. Improving monetary control

- A. Reserve requirements

- B. Deposit insurance to prevent bank panics

Recommended

CrystalGraphics Presentations