CASE 5 Cash Flow Hedge of VariableRate Debt

Title:

CASE 5 Cash Flow Hedge of VariableRate Debt

Description:

CASE 5 Cash Flow Hedge of VariableRate Debt – PowerPoint PPT presentation

Number of Views:100

Avg rating:3.0/5.0

Title: CASE 5 Cash Flow Hedge of VariableRate Debt

1

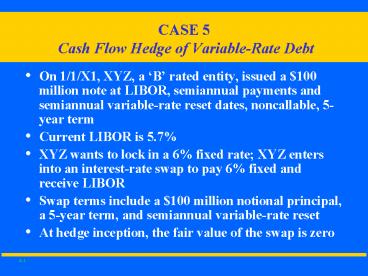

CASE 5 Cash Flow Hedge of Variable-Rate Debt

- On 1/1/X1, XYZ, a B rated entity, issued a 100

million note at LIBOR, semiannual payments and

semiannual variable-rate reset dates,

noncallable, 5-year term - Current LIBOR is 5.7

- XYZ wants to lock in a 6 fixed rate XYZ enters

into an interest-rate swap to pay 6 fixed and

receive LIBOR - Swap terms include a 100 million notional

principal, a 5-year term, and semiannual

variable-rate reset - At hedge inception, the fair value of the swap is

zero

2

CASE 5Cash Flow Hedge of Variable-Rate Debt

- Assume that during the six-month period ended

6/30/X1, interest rates increase. Also, a

comparable term pay-fixed, receive-variable

interest rate swap is priced at 6/30/X1 at a 7

pay-fixed rate. Given these facts, the direction

of fair value changes are as follows - Variable-rate debtno change in value given that

rates reset to market - Pay-fixed 6, receive-variable interest rate

swapincreases in value

3

CASE 5Cash Flow Hedge of Variable-Rate Debt

6/30/X1 12/31/X1 Variable-rate

debt 100,000,000 100,000,000 Variable rate

5.7 6.7 Semiannual debt payment 2,850,000 3,350

,000 Swap receive variable

(2,850,000) (3,350,000) Swap fixed

payment 3,000,000 3,000,000 Net debt and swap

interest expense 3,000,000 3,000,000 Rate

increased 100 basis points on 7/1/X1 reset.

4

CASE 5Cash Flow Hedge of Variable-Rate Debt

6/30/X1

12/31/X1 Fair value of pay 6 swap

3,804,0001 3,437,0002 1 PV of nine 500,000

semiannual payments, discounted at 3.5 per

period 2 PV of eight 500,000 semiannual

payments, discounted at 3.5 per period

5

CASE 5Cash Flow Hedge of Variable-Rate Debt

At 6/30/X1 Interest expense

2,850,000 Interest payable 2,850,000 To

record debt interest accrual Interest receivable

2,850,000 Interest expense

150,000 Interest payable 3,000,000 To record

swap accrual (receive 5.7 and pay-fixed

6) Swap asset 3,804,000 OCI 3,80

4,000 To record fair value of swap excluding

accrual

6

CASE 5Cash Flow Hedge of Variable-Rate Debt

At 12/31/X1, rates have remained the same as at

6/30/X1 and the swap market value has decreased

to 3,437,000 due the 12/31/X1 payment and time

passage. Interest rates reset on 6/30/X1 for

both the swap and variable-rate debt reflecting a

100 basis point increase in LIBOR.

7

CASE 5Cash Flow Hedge of Variable-Rate Debt

At 12/31/X1 Interest expense

3,350,000 Interest payable 3,350,000 To

record debt interest accrual ((.067

100m)/2) Interest receivable

3,350,000 Interest payable

3,000,000 Interest expense

350,000 To record swap accrual (receive 6.7 and

pay 6) OCI 367,000 Swap asset

367,000 To record fair value change of swap

excluding accrual

8

CASE 5Cash Flow Hedge of Variable-Rate Debt

- XYZ documented that the swap and variable-rate

debt terms for the nominal amounts, payment

frequency, reset dates, and maturity match - The effectiveness of the hedge was demonstrated

throughout the term of the hedge - This hedge is not exposed to basis risk because

the swap and debt each have the identical

variable rate (LIBOR)

9

CASE 6 Fair Value Hedge of Fixed Rate Debt

Long-Haul Method

- On 4/3/00, GlobalTechCoSub issues at par a

non-callable, 5-year, 100 million note at 8

fixed interest, semiannual payments (debt is

rated A1) - On 4/3/00, GlobalTechCo also enters into a 5-year

interest rate swap 101,970,000 notional amount,

pay LIBOR plus 78.5 basis points, receive fixed

at 8, semiannual settlement and interest reset

dates - Net interest outflow LIBOR plus 78.5 bps

(current LIBOR at 6.29) - Swap is at-market, therefore, no premium required

10

CASE 6 Fair Value Hedge of Fixed Rate Debt

Long-Haul Method

- Hedged item 100 million, 5-year, 8 percent

fixed rate, non-callable debt - Hedge Strategy Eliminate debt fair value changes

attributable to changes in the LIBOR swap rate by

converting interest payments to LIBOR based

variable-rate. - Hedging instrument Interest rate swap, terms

pay LIBOR plus 78.5 basis points, receive 8

fixed rate. Semiannual swap settlement and rate

reset at /3 and 10/5. Swap fair value at hedge

inception 0.

11

CASE 6 Fair Value Hedge of Fixed Rate Debt

Long-Haul Method

- Statement of hedge effectiveness A

duration-weighted hedge ratio calculates the swap

notional amount necessary to offset the debts

fair value changes attributable to changes in the

LIBOR swap rate. - PV01 debt 4.14

- PV01 swap 4.06

- Hedge ratio PV01 debt/PV01 swap 4.14/4.06

1.0197 - Swap notional 1.0197 x 100 million

101,970,000

12

CASE 6 Fair Value Hedge of Fixed Rate Debt

Long-Haul Method

- Statement of hedge effectiveness (continued)

- Therefore, a 1 basis point shift in the

GlobalTechCoSub 100 million debt issuance equals

a 1 basis point shift in 101,970,000 notional of

the LIBOR based swap.

13

CASE 6 Fair Value Hedge of Fixed Rate Debt

Long-Haul Method

- Statement of hedge effectiveness (continued)

- The swap accrual for its semi-annual settlement

is excluded from the swaps calculation of its

change in fair value. The debts interest accrual

is also excluded from its calculation of changes

in fair value. This simplifies the hedge

effectiveness calculation - On a prospective and retrospective basis, hedge

effectiveness will be assessed based upon a

regression analysis of changes in the LIBOR swap

rate and changes in the bonds present value,

calculated based on its yield at hedge inception,

adjusted for changes in the LIBOR swap rate (DIG

Issue E7)

14

CASE 6 Effect of 100 Basis Point Rate Increase

at 6/30/00

- 6/30/00 swap fair value change,

- Receive 8 fixed, pay LIBOR

- 78.5 basis points swap 4,252,000

- Less

- Swap accrual for the period 4/3-6/30 236,000

- Net Swap Loss 4,016,000

- (Interest rate shift assumed to be a parallel

shift in the yield curve)

15

CASE 6 Recording Hedge Activity

- 4/30/00

- No entry required because swap entered into

at-the-money - 6/30/00

- Dr Debt 3,775,620

- Cr Earnings 3,775,620

- Dr Earnings 4,016,000

- Cr Swap Liability 4,016,000To record

swap and debt fair value changes attributable to

changes in the LIBOR swap rate, excluding accruals

16

CASE 6 Ineffectiveness Recorded at 6/30/00

- The net earnings impact of the hedge was 240,380

due to some imprecision in the calculated hedge

ratio. The hedge would continue to qualify for

hedge accounting provided the regression analysis

justified the result - In practice, this result will be common

- The debts subsequent period changes in value

attributable to changes in the LIBOR swap rate

are computed by comparing its prior period

present value (not the same as its fair value) to

its current period present value, excluding

accrued interest

Recommended

CrystalGraphics Presentations