Crane v. Commr - PowerPoint PPT Presentation

1 / 17

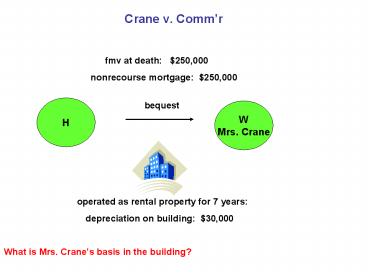

Title: Crane v. Commr

1

Crane v. Commr

fmv at death 2

50,000 nonrecou

rse mortgage 250,000

operated as rental property for 7

years depreciati

on on building 30,000 What is Mrs. Cranes b

asis in the building?

H

bequest

W Mrs. Crane

2

Mrs. Cranes Adjusted Basis

Original basis 250,000 (1014

fmv at death) less adjustments

30,000 (1016 adjustment for depreciation)

Adjusted

Basis 220,000

3

Sale to

Third Party transfer of b

uilding

subject to

250,000 mortgage

and 2,500 cash (boot)

Mrs. Crane

buyer

4

1001 Gain

Mrs. Cranes position

IRS Position AR 2,5

00 (cash only) 252,500 (cash mortgage)

AB 0 (equity)

220,000 (1014 basis as adjusted)

Gain 2,500

32,500

2,500

30,000

capital gain

depreciation

recapture

5

Commr v.

Tufts Original Purchase

transfer of building nonrecour

se mortgage lien 1,850,000

Seller

Buyer Tufts and partners

6

Partners adjusted basis Or

iginal basis 1,850,000 (1012 cost,

including mortgage) less

400,000 (1016 adjustment for

depreciation) Adjusted Basis

1,450,000

7

Sale to Third Party

fmv transfer of building fmv 1,400,000 AB

1,450,000

Buyer - Fred Bayles

Tufts partners

subject to 1,850,000 mortgage

8

1001 Gain Taxpayers posi

tion IRS

Position AR 1,400,000 (limited to bu

ilding fmv) 1,850,000 (full

mortgage) AB 1,450,000 1,450,00

0 ( 50,000)

400,000

loss

gain

deprec

iation recapture argumen

t based on Crane fn. 37

9

Bifurcation

Approach Part Discharge

Part Sale AR 1,850,00

0 (full debt)

1,400,000 (fmv of property transferred)

AB 1,400,000 (fmv property transferred)

1,450,000 (adjusted basis in

property) 450,000 (

50,000) gain

loss

discharge of debt

loss from sale

ordinary income

possibly capital

loss

net gain 400,000

10

Treas. Reg. 1001-2(c), ex (1) Assumption of

Recourse Note

1,000 cash

9,000 recourse loan

Original purchase price 10,000

Original basis Original

Debt 10,000 9,000

less 3,100 (depreciation)

1,400 (principal payments)

AB 6,900 remainin

g debt 7,600

11

Sale of asset for cash assumption of recourse

mortgage

fmv debt case

Buyer

TP (seller)

asset fmv 9,200

1,600 cash 7,600 assumption of remaining liab

ility (recourse)

9,200

1001 Gain AR 9,200 less AB 6,900

2,300

12

Treas. Reg. 1001-2(c), ex (2)

Assumption of Nonrecourse Note Crane facts

1,000 cash

9,000 nonrecourse loan

Original purchase price 10,000

Original basis Original

Debt 10,000 9,000 less

3,100 (depreciation)

1,400 (principal payments) AB 6,900

remaining debt 7,600

13

Sale of asset for cash assumption of

nonrecourse mortgage

still fmv debt case (Crane)

TP (seller)

Buyer

asset fmv 9,200

1,600 cash 7,600 assumption of remaining liab

ility (nonrecourse)

9,200

1001 Gain AR 9,200 less AB 6,900

2,300

14

Treas. Reg. 1001-2(c), ex (7)

Assumption of Nonrecourse Note Tufts facts

1,000 cash

19,000 nonrecourse loan

Original purchase price 20,000

Original basis

Original Debt 20,000

19,000

less 3,500 (deductible loss)

no principal payments

AB 16,500

remaining debt 19,000

15

Transfer of asset for assumption of nonrecourse

mortgage

fmv TP (seller)

Buyer

asset fmv 15,000

assumption of 19,000 remaining liability

(nonrecourse)

1001 Gain AR 19,000 less

AB 16,500 2,500

16

Treas. Reg. 1001-2(c), ex (8)

Transfer of asset for assumption of recourse

mortgage

still fmv TP (seller)

Buyer

asset fmv 6,000

assumption of 7,500 liability (recourse)

no information available on taxpayers asset basis

17

Treasury Regulation Approach for

Recourse Mortgages Bi

furcation Part Discharge

Part Sale

AR 7,500 (full debt)

6,000 (fmv of property

transferred) AB 6,000 (fmv property transfe

rred) ? (adjusted

basis in property) 1,500

?

gain

gain or loss

discharge of debt

gain or loss from sale

ordinary income

possibly

capital loss

Recommended

CrystalGraphics Presentations