Table 1

1 / 23

Title: Table 1

1

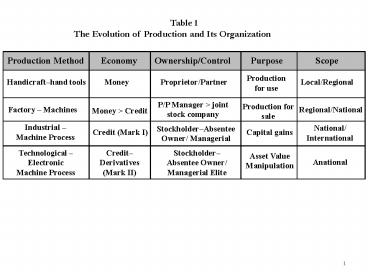

Table 1 The Evolution of Production and Its

Organization

Economy

Ownership/Control

Production Method

Purpose

Scope

Production for use

Handicrafthand tools

Money

Proprietor/Partner

Local/Regional

P/P Manager gt joint stock company

Production for sale

Regional/National

Factory Machines

Money gt Credit

Industrial Machine Process

National/ International

StockholderAbsentee Owner/ Managerial

Credit (Mark I)

Capital gains

Technological Electronic Machine Process

StockholderAbsentee Owner/ Managerial Elite

Credit Derivatives (Mark II)

Asset Value Manipulation

Anational

2

- Financial Instability

- Stability breeds instability

- Stability leads to comfort and belief that risk

is less (example US housing market 1975- 1995) - Expected future income of firm (example,

expected 6 average annual increase in US housing

prices, used in ratings models) - Income of firm realized vs speculative

3

Business Fluctuations - Theories

- Production Cycles

- Marx simple underconsumption

- Schumpeter innovation and increased investment

- End of investment opportunities

- Lack of creative destruction due to growing firm

size and inflexibility - Monetary Credit Cycles

- Keynes -- Both production and Monetary complex

underconsumption - Veblen -- speculation and credit cycles

- Minsky financial instability hypothesis will

not go into this-- similar to Veblen in some

significant ways

4

- Keynes Theory of Employment Money - and

Institutional theory - Fluctuations in economy due to Aggregates not

individuals - Under investment underconsumption theory of

the trade cycle - Long term involuntary unemployment

- Solution

- Government Borrow and Spend

- Consequences

- Deficit finance functional finance

- Balanced budget becomes part of mythology

- Saving is function of income not interest rate

- Changes the concept of necessity to raise

interest rate and other incentives to save - Capital (physical) accumulation theory of

classical theory obsolete (savings centered

theory) - Replaced by knowledge and resource based theory

- Resources are a function of knowledge and Become

. . . Not are - Scarcity as social condition transcends scarcity

as natural one

5

- To Repeat Institutionalization of intangible

property strengthens instability of financial

systems offsetting in part some of the gains of

previous institutional changes - Example

- A primer on modern housing Institutional

Evolution - Securities, Equity- Debt, from these all else is

derived. The innovations in finance are few,

just new names for the same things. We add

Insurance as a socialization of risk of damage - It has several traits

- Market Value (MV) selling price also

Collateral value - A Book Value (BV) replacement cost

- Debt Mortgage Balance (MB)

- Equity MV - MB

- MV gt BV asset appreciation

- BV lt MV asset depreciation

6

- AS a hedge against MV lt MB we developed and

expanded several institutions and organizations - Down payment, a monetary amount of some

percentage of the sales price (MVt), 20 percent

in the early years then less later Less than 20

usually required mortgage insurance - Income assurance, rigorous proof of income,

employment, etc. (mp 29 of GAI) - Credit rating, a number reflecting an evaluation

of the borrowers credit history. - 4. Enabling Organizations

- Local Savings and Loans Thrifts

- Capital Federal Savings Loan

- Argentine Saving Loan

- Lincoln National

- Federal Mortgage Mortgage Assurance

Institutions - Freddie Mac 1970 secondary mortgage loan

market - Fannie Mae 1938 national secondary mortgage

less reliance on thrifts - Securitization of mortgages

- VA loans 1944 18 million loans

- FHA Federal Mortgage Insurance 1934 34

million loans

7

- There were ancillary institutions and

organizations - Financial Regulation Interstate or Branch

Banking Banned - Separation of Commercial Banking from

Investment Banking (Glass-Steagall Act) - Third Party (Independent) Credit Rating

Agencies - Investment Activity gtdominatedgt Trading

Activity - The led to a US housing market and housing that

was the envy of the world

8

Number of Housing Units Built in US, by Selected

years, 1919 and before to 2009

Table 2-1. Introductory Characteristics--Occupied Units

Numbers in thousands.

Characteristics Total occupied units Tenure Tenure

Characteristics Total occupied units Owner Renter

Total 111,806 76,428 35,378

Year Structure Built3, 5

2005 to 2009 5,884 4,601 1,283

2000 to 2004 8,102 6,371 1,731

1995 to 1999 7,825 6,221 1,603

1990 to 1994 5,995 4,715 1,280

1985 to 1989 7,648 5,159 2,489

1980 to 1984 6,380 4,201 2,179

1975 to 1979 11,835 7,471 4,364

1970 to 1974 9,413 5,696 3,718

1960 to 1969 13,326 8,917 4,409

1950 to 1959 11,771 8,528 3,243

1940 to 1949 6,745 4,423 2,322

1930 to 1939 4,828 2,904 1,924

1920 to 1929 4,331 2,520 1,811

1919 or earlier 7,724 4,703 3,021

Median 1974 1975 1971

- But a House is more than a place to live, it is

also an asset, a source of equity and debt.

9

- Then comes a retrenchment to the old habits

- A belief in the ever expanding housing market

and home prices - Belief in self-regulating markets to deliver on

their utopian promise - An ideological power structure to assist in

removing or forestalling regulatory forces - Trading as a dominant process for earning it

- SPEED, trading at the speed of light 24 hours per

day - This led to

- Savings Loan Industry Deregulated 1981 now

can engage in banking activity - Financial Regulation Interstate Banking Ban

repealed 1984 - Separation of Commercial from Investment Banking

(Glass-Steagall Act) repealed 1995 - Third Party (Independent) Credit Rating Agencies

compromised - Investment Activity gt morphs to gtTrading Activity

after dot com bubble burst - One consequence was a spawning of new or

repackaged investment instruments in the image of

Goldman Sachs Trading Company of 1929. - An example

10

Credit Default Swap 1 (CDS) Playing short for

the CDO price to go down or to fail (default)

this is roughly equivalent to buying a fire

insurance policy on your house with a value

greater than MV and then hiring someone to set it

on fire. If the CDO goes down, you gain because

the CDS (insurance) pays out at the price of the

CDO at the time you bought the CDS (the insured

amount). CDS 2 long playing for the CDO

price to go up or not to fail (not default)

this is roughly equivalent to buying a fire

insurance policy on your house for less than the

MV then paying someone to stand watch with a fire

hose. One could buy any combination of the

derivatives, CDO (MBS is one) and CDSs Now

suppose we have an important investment company

seeking ratings for instruments that it wants to

sell. It uses that position to persuade the

rating agency that the instrument is worthy of a

high rating.

11

Making Collateralized Debt Obligations Mortgage

Backed Securities Simple Tranche

Beginning Portfolio of Mortgages

Collateralized Debt Obligation Low Risk Fund Name

Beta 1

Collateralized Debt Obligation Medium Risk

Fund Name Junk 1

Collateralized Debt Obligation Risky Fund Name

Default 1

Collateralized Debt Obligation High Risk

Fund Name Toxic 1

Collateralized Debt Obligation Lowest Risk

Fund Name Alpha 1

Rating AAA

Rating BBB

Rating NA Not For Sale

Rating DDD

Rating CCC

These may be rated by a third party and sold

based on that rating. The higher the rating the

lower the risk and hence the lower the return.

Investors may choose the level of risk and return

based on the rating and the transparency of the

collateral behind the debt. Also, and this is

one purpose for these securities, an investor may

choose the timing of their income from the

tranche they buy.

Fair enough, but now the fun starts. We move on

to create a Synthetic CDO

12

Making Collateralized Debt Obligations

Synthetic Tranche

Alpha 1

Beta 1

Junk 1

Default 1

Toxic 1

Surplus Toxins

Rating AAA

Rating BBB

Rating DDD

Rating AAA

Rating BBB

Rating AAA

We can create many combinations of financial

instruments based on the previous portfolios.

With a AAA rating these can be sold to

organizations required to buy only AAA securities.

On the theory that several toxic assets in a

portfolio are less risky than one of them we

create another CDO and rerate it

higher. Especially if we can buy insurance and

play it short then we may get a higher rating

13

Goldman Sachs went public in 1999 In 1998 72

of its net income came from investment banking

asset management services In 2009 76 came

from trading and the remainder from Investment

banking asset management services

14

SEC civil fraud lawsuit, filed in April 2010

Abacus mortgage-backed CDOs On April 16, 2010,

the Securities and Exchange Commission (SEC)

announced that it was suing Goldman Sachs and one

of its employees, The SEC alleged that Goldman

misstated and omitted facts in disclosure

documents for a synthetic CDO product it called

Abacus 2007. The allegation is that Goldman

misrepresented to investors that an independent

selection agent, ACA, had reviewed the mortgage

package underlying the credit default

obligations, and that Goldman failed to disclose

to ACA that a hedge fund, Paulson Co, that

sought to short the package, had helped select

underlying mortgages for the package against

which it planned to bet. The complaint states

that Paulson made a 1 billion profit from the

short investments CDSs, while purchasers of the

materials lost the same amount. The two main

investors who lost money were ABN Amro and IKB

Deutche Industriebank. IKB lost 150,000,000

within months on the purchase. ABN Amro lost

840,909,090. Goldman stated the firm also lost

90 million and did not structure a portfolio

that was designed to lose money The New York

Times reported that After the SEC announced the

suit during the April 16, 2010 trading day,

Goldman's Sachs's stock fell 13 to close at

160.70 from 184.27 on volume of over 102,000,000

shares (vs. a 52 week average of 13,000,000

shares). The firm's shares lost 10 billion in

market value during the trading session. On April

30, 2010, shares tumbled further on news that the

Manhattan office of the US Attorney General

launched a criminal probe into Goldman Sachs,

sending the stock down more than 15 points, or

nearly ten percent to 145.

15

Goldman Sachs Stock Price 2003-2011

16

New Theories

- New Institutional Economics

- Coase Nature of Firm (why are there firms)

- Transactions Costs

- Substitution at the Margin labor/capital

production function - Simon

- Not firms that are explained by markets --

Rather Markets are explained by firms - Organizational Capitalism

- Williamson

- Limited Information (Bounded Rationality of

Simon) - Opportunism

- Self interest with guile

- Asset Specificity Make/Buy

- Penrose -- a Veblenian Update

- Everything can not happen at once

- A person can not do everything/anything alone

- The Learning firm

- Can not buy inputs the way the firms uses them

labor - Objective Knowledge -- transferable via books,

manuals - Experiential Knowledge

17

Path Analysis

- Veblen

- British Rail System in 1914

- The mud hole metaphor more on this later

- David

- Clio and the Economics of QWERTY 1985

- Keyboard configuration

- Technological Lock-in

- Why the nature of a path

- Ergodic

- Non-ergodic

- Small events early in a technology

18

Path continued

- Arthur

- Non-linear probability 1991

- Example of rings in an urn

- Draw a sample and replace with color bias

- What happens

- no stable equilibrium

- No necessity to pick better technology

- VHS Beta

- Increasing returns problem

- Possible solution Positive feedback

- Standard approach is negative feedback system

- Firm and industry location

- Carpet firms in Georgia why there?

- Third Italy history of institutions and

institutional adjustment - Complexity theory

19

Path Dependence A Story and a Metaphor

- The Reivers

20

From Faulkners The Reivers There was something

dreamlike about it. Not night-marish just

dreamlike--the peaceful, quiet remote, sylvan,

almost primeval setting of ooze and slime and

jungle growth . . . In it the expensive useless

mechanical toy rated in power and strength by the

dozens of horses, yet held helpless and impotent

in the almost infantile clutch of a few inches of

the temporary confederation of two mild and

pacific elementsearth and water . . . the

three of us, . . . now unrecognizable mud-colored

creatures engaged in a life-and-death struggle

with it, . . . And all the while, the man sat in

his tilted chair on the gallery watching us while

Ned and I stained for every inch . . . and Boon .

. . strove like a demon, titanic, . . . lifting

and heaving it forward . . . he dropped, flung

away his pole. . . How much do you have to pay

him to get dug out? Ned asked. Two dollars,

Boon said. Two dollars? Ned said. This

sho beats cotton. He can farm right here setting

in the shade without even moving. What I wants

Boss to get me is a well-traveled mudhole.

Morning, boys, he said. Looks like youre

about ready for me now. Looks like it, Boon

said. . . . We might a got through . . . if you

folks didnt raise such heavy mud up

here. Dont hold that against us, the man

said. Muds one of our best crops up

thisaway. At two dollars a mudhole, it ought to

be your best, Ned said. That was last year,

the man said. Its double now. Its six

dollars, he said. I charge a dollar a

passenger. There was two of you last year. That

was two dollars. The price is doubled now.

Theres three of you. Thats six dollars Boon

said, Suppose I dont pay you six dollars.

Suppose I dont pay you nothing. You can do

that too, the man said. . . . . Maybe youd

rather walk back to Jefferson than pay two

dollars. (Faulkner, pp. 80-91)

21

- Roads, Cars Mud holes

- Evolution of Roads, Cars

- And the Economy becomes dependent on single

source variable route individual transportation

system - GM plan

- Economies are both path dependent and path

created - Depends on structure, function and flexibility

- Flexibility is inversely related to strength of

tradition - Myth, legend and invidious differential advantage

- Strength of status quo

- Flexibility is directly related to strength of

learning and growth of community shared knowledge - Technology

- Education

- Objective and Experiential knowledge (the

interaction of knowing doing)

22

Mud Puddles Mud Holes Quagmires

Wooden baseball bats Typewriter Keyboards Cities located in flood plains

VHS videotapes Computer Operating systems Cities located in deserts

File name extension OPEC and Exxon Railroad gauge

Y2K bug National brand beer Automobile dominated transportation

Language homonyms Sport Utility Vehicles Pecuniary dominated industrial apparatus

23

Examples of Feedback Attributes

Instrumental Ceremonial

associative territorial

deliberation calculation

technical skill invidious comparison

means-end-means expediency

inventiveness appearance

honesty deceit

adaptive inflexible

democratic autocratic

confidence anxiety

creativeness credit conscious

innovation opportunism

participatory proprietary

imaginative guileful

cooperative competitive

generosity selfishness

decency meanness

forgiveness revenge

Recommended

CrystalGraphics Presentations