The Future of Electronic Commerce - PowerPoint PPT Presentation

1 / 18

Title:

The Future of Electronic Commerce

Description:

Notational money: ledger entries in Demand Deposit Accounts ... Example: NetBill, CompuServe, AOL, MSN. xx. The NetBill Concept ... – PowerPoint PPT presentation

Number of Views:53

Avg rating:3.0/5.0

Title: The Future of Electronic Commerce

1

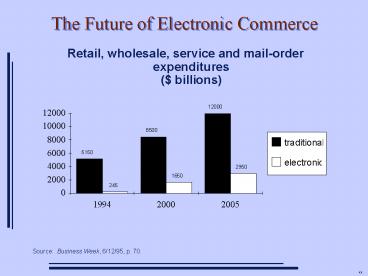

The Future of Electronic Commerce

- Retail, wholesale, service and mail-order

expenditures( billions)

Source Business Week, 6/12/95, p. 70.

2

Electronic Commerce

- Many phases to a commercial transaction

- learning about what goods are available

- finding potential suppliers

- negotiating price

- ordering goods

- goods delivery

- payment

- after sales support

3

The Internet and Information Markets

- The global reach of the Internet makes it the

leading network for disseminating information - There are many ways to organize a market for

information - The lack of payment mechanisms to date has

limited the variety of market structures

4

Payment Systems

- There are two kinds of money

- Token money tokens which represent value

- tokens can be exchanged for goods

- Notational money ledger entries in Demand

Deposit Accounts - money is transferred between accounts upon

instruction - e.g. by a check

- clearing required if accounts are at different

institutions - accounts may have negative balances

- e.g. credit card accounts

5

Payment Systems

- Payment System tradeoffs

- time

- setup cost

- transaction cost

- risk

6

Financial Transaction System-Cost Structure

7

Internet-Based Payment Models

- Secure transmission of credit card information

- Digital cash

- Digital checks

- Centralized online transactions

8

Credit Card Info Sent Direct to Merchant

(Netscape Model)

Merchant

Private Line

Credit Card Acquirer

Encrypted tunnel through the Internet

- Consumer sends card direct to merchant

- Similar to todays phone order

- Must trust merchant with card info

- High transaction costs

Internet

Consumer

9

Third Party Intermediary Model(CyberCash)

- Protects consumers card info

- Use Internet for reaching Cybercash gateway to

acquirers - Adds to credit card card cost

Merchant

Encrypted tunnel through the Internet

Internet

CyberCash

Consumer

10

Credit Card Acquirer On the Net (STTSEPPSET)

- Protects consumers card info

- Use Internet for reaching acquirer

- Still uses expensive credit card transactions

Merchant

Encrypted tunnel through the Internet

Internet

Consumer

11

Green Commerce Model(First Virtual)

- Messages sent in clear

- Credit card number stored at FV

- User must agree to pay after receiving

information goods - Credit Card transaction costs

Merchant

First Virtual

Internet

Consumer

12

Digicash Model

- 1- Consumer asks Bank for Digicash

- 2- Bank sends Digicash bits to consumer

- 3- Consumer sends Digicash to merchant in payment

- 4- Merchant checks that Digicash has not been

double spent - 5- Bank verifies that Digicash is valid

- Advantages

- Privacy, Scalability

- Disadvantages

- Complexity

- Detecting double spending

- Robustness against failure

- Accountability

Merchant

5

4

3

Bank

2

1

Consumer

13

Approach Digital Checks

- Consumers issue signed drafts on online bank

accounts - Merchants may do online or delayed clearing

- Examples NetCheque, FSTC NetAccount

14

Approach Online Transactions

- Funds transfer between accounts at a central

server - All accounts at the central server

- Prepaid or postpaid consumer accounts

- Advantages

- Low transaction overhead cost

- Disadvantages

- Scalability server may become a bottleneck

- Requires arrangement with accounting server

- Example NetBill, CompuServe, AOL, MSN

15

The NetBill Concept

- An electronic accounting server to enable network

based commerce - Accounts maintained at NetBill for rapid,

inexpensive payment clearing (1 transaction cost

for a 10 item)

Network

Service

Provider

End

User

NetBill

Server

Bank

16

Aggregation

- Users and Merchants create NetBill aggregation

accounts. - Each purchase transaction moves funds from the

users NetBill account to the merchants NetBill

account - Money transferred into or out of the aggregation

account using conventional money transfers - credit card charge

- ACH

- Fixed cost of conventional transfers amortized

over many microtransactions - Aggregation account can be run as a prepaid or as

a credit account - Prepaid conventional debit in advance of

micro-transaction - Credit charge user after aggregated

transactions reach a threshold

17

Issues of Trust in Electronic Commerce

- What does a merchant need to know about a

customer? - name? demographics?

- that the merchant will be (has been) paid?

- Who to trust

- financial intermediaries

- public key certificate authorities

- credential authorities

- The theory of reliable transactions has been

based on premise that errors are accidental not

deliberate. - New mechanisms needed to protect against errors

deliberately introduced with intent to defraud.

18

Summary

- The Internet is becoming the Global Information

Infrastructure - All phases of commerce can be supported by

networks - Organization of electronic information markets is

currently limited by lack of Internet payment

systems - Numerous payment models are being developed

- For information goods, delivery and payment

should be linked as a single atomic transaction

at low cost.

Recommended

CrystalGraphics Presentations