Harnischfeger - PowerPoint PPT Presentation

1 / 30

Title:

Harnischfeger

Description:

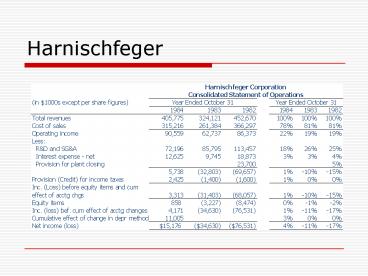

... you think investors will 'see through' these changes? Harnischfeger ... Investors see through? ... Stock market may or may not see through these managements. ... – PowerPoint PPT presentation

Number of Views:2922

Avg rating:3.0/5.0

Title: Harnischfeger

1

Harnischfeger

2

Harnischfeger

- We recommend the stock of Harnischfeger

Corporation for purchase in speculative accounts

because we expect the company to report a modest

profit this year and untaxed earnings of 3 per

share in 1985, following ten years of

deteriorating financial statements and two years

of large losses. Earnings power, assuming a

sustained recovery of the companys markets,

could be 4.00-6.00 per share in the 1986-1987

time period. The Harnischfeger stock is selling

at less than three times these peak earnings

(were they taxed) and at a slight discount to

book value.

3

Harnischfeger

4

Harnischfeger

- What was responsible for Harnischfegers turn

around? - Identify all the accounting policy changes and

accounting estimates that Harnischfeger made

during 1984. Estimate, as accurately as possible,

the effect of these changes on the companys 1984

reported profits.

5

Harnischfeger

- Accounting Changes

- Depreciation method add 11M

- Depreciation estimate add 3.2M

- Pension gain rate of return assumption for

pension add 3.9M and 0.1M - LIFO liquidation add 2.4M

- Provision for doubtful accounts add 2.6M

6

Harnischfeger

- Harder to determine for these changes

- Fiscal year change for subsidiary 15 months in

1984, insignificant change to net income, sales

increase by 5.4M - RD expense reduced expenditures to below Kobe

reimbursement - Included sales from Kobe Steel why? Help build

topline

7

Harnischfeger

- What do you think are the motives of

Harnischfegers management in making the changes

in its financial reporting policies? - Do you think investors will see through these

changes?

8

Harnischfeger

- Incentives

- Boost stock price to raise new capital

- Meet earnings targets for compensation

- Avoid violating debt covenants

- Improve image with customers, suppliers, etc.

- Internal pricing tied to external reporting

numbers. Accelerated depreciation makes cost

appear too high.

9

Harnischfeger

- Investors see through?

- Considerable evidence in finance and accounting

that capital markets are generally efficient - For stock prices to reflect reality in an

unbiased manner, not necessary to have everyone

see through marginal investors are the price

setter.

10

Harnischfeger

- From the management side - why manage earnings

- Investors didnt adjust their original

conservative accounting - Unpleasant experience with debt covenant

- Interaction between mgmt accounting and external

accounting.

11

Harnischfeger

- Harnischfeger managements perspective on

earnings management - In accounting there is no such thing as absolute

truth. The same underlying reality can be

accounted for using a range of assumptions. The

earlier philosophy of this company was to choose

the conservative alternative whenever there was a

choice. Now we have decided to change this. We

would like to tell the world that we are alive

and well. We wish to tell the truth but do not

want to be overly conservative in doing so.

12

Harnischfeger

- Harnischfeger managements perspective on

earnings management - As a company you have to put the best foot

forward if you want to raise capital, convince

customers that you are a viable company, and

attract talented people to work for the company.

I feel that the financial reporting should help

rather than hinder the implementation of our

operating strategy. In my opinion, the changed

accounting format highlights the effectiveness of

our strategy better than the old policies do.

13

Harnischfeger

- Harnischfeger managements perspective on

earnings management - When the outside world compares our financial

performance with that of other companies, they

may or may not take the time and effort to

untangle the effects of the differences in

financial policies that various companies follow.

My own belief is that people adjust for the

obvious things like one-time gains and losses but

have difficulty in adjusting for ongoing

differences. In any case, these adjustments

impose a cost on the user.

14

Harnischfeger

- Harnischfeger managements perspective on

earnings management - If people adjust for the differences in

accounting policies when they compare us with

other companies, then it should not matter

whether we follow conservative or liberal

policies. But suppose they do not adjust. Then

clearly we are better off following the more

liberal policies than conservative policies. I am

not sure whether people make the adjustments or

not, but either way we wish to present an

optimistic version of the picture and let people

figure out what to do with the numbers.

15

Harnischfeger

- Assess the companys future prospects given your

insights and the information in the case on the

companys turnaround strategy.

16

Harnischfeger SCF

17

Harnischfeger

- Assessing their turnaround strategy

- Changes in top management

- Cost reductions to lower the companys breakeven

point - Reorientation of the companys business

- Restructuring the companys finances to

facilitate the implementation of the

reorientation strategy

18

Harnischfeger

- Subsequent events

- 1985

- Changed accounting for the cost of duration

patterns and tooling, from expensing to

capitalizing - Reported a net profit of 0.74 per share for

fiscal 1985. The accounting changes described

above contributed 0.24 per share to the reported

profits. - Raised 147M by issuing preferred stock.

19

Harnischfeger

- Subsequent events

- 1986

- Mr. Goessel was appointed the chairman and CEO of

the company Mr. Grade as president and COO. Mr.

Goessels previous appointment was president and

COO and Mr. Grade CFO. - Acquired Beloit corporation for 175 million in

cash. Later sold 20 of the stake for 60 million

in cash.

20

Harnischfeger

- Subsequent events

- 1986

- Report a 1.14 per share loss (2.15 profit from

continuing operations 4.45 loss from

discontinued operations and 1.16 per share from

the adoption of new pension accounting rules.)

21

Harnischfeger

22

Harnischfeger

- Wrap up

- Managers exert significant discretion in choosing

accounting method and estimates. - These choices affect the reported financial

statements. - Various incentives exist for earnings management

- Understanding these incentives is essential for

evaluating current performance and assessing

future aspects of a firm. - Stock market may or may not see through these

managements. - A sophisticated and diligent analyst can uncover

more information than average investors.

23

Corporate Governance and SOX

- Effect on Auditors

- Auditors must register with PCAOB

- Annual quality inspections every year for

registrants that audit more than 100 issuers - Lead and reviewing partners must rotate off every

5 years - no movement by auditor into CEO/CFO/Chief

Accountant position for two years

24

Corporate Governance and SOX

- New audit committee requirements

- members must be independent

- financial expert financially literate

- responsible for appointment, compensation and

oversight of independent auditors

25

Corporate Governance and SOX

- Management assessment of internal controls,

Section 404 - Management is responsible for Internal controls

- annual assessment of effectiveness (section 404)

- Benefit - fewer misleading and fraudulent

financial statements assuming...

26

Corporate Governance and SOX

- Cost vs. Benefit

- Cost from Foley and Lardner 2005 study

- average cost of being public in 2004 increased

33 over 2003 for a company with annual revenue

under 1B 223 in total since SOX - for companies with revenues over 1B cost of

being public 14.3M, 1M in lost productivity

27

Corporate Governance and SOX

- Cost from Foley and Lardner 2005 study

- Small cap audit fees rose 84 to 1.04M in 2004

from 2003 - Mid-Cap audit fees rose 92 to 2.18M in 2004

from 2003 - Large cap audit fees rose 55 to 4.81M in 2004

from 2003 - Self reported results

28

Corporate Governance and SOX

- Corporate Responsibility for financial reports

- CEO CFO must certify

- They reviewed the financial reports

- report (to their knowledge) does not contain any

untrue statement or omit material information - Disclosures present operations and financial

condition fairly - Internal controls were evaluated and are

effective - Have disclosed material deficiencies and frauds

to auditors

29

Corporate Governance and SOX

- Limitations on auditor services

- Specified non-audit services cannot be provided

to client - Financial information systems design and

implementation - Investment management securities services

- Legal, actuarial and expert services unrelated to

the audit - tax preparation allowed, tax strategies not

allowed

30

Corporate Governance and SOX

- Limitations on auditor services

- Cost vs. Benefit

- Raises the cost of both audits and other services

as it reduces the economies of scale and

knowledge enjoyed by the auditor - There is no evidence that auditor performing

other services led to substandard auditing

(although a lot of anecdotal evidence, but is

this what we should base policy on...)

31

Corporate Governance and SOX

- How big was the problem?

- First point - not all restatements are a result

of fraudulent information or inadequate audits - GAO study of restatements 1997-2002 found on

average 169 restatements per year - restatements have increased in recent years,

but probably due changes in rules conservatism

Recommended

CrystalGraphics Presentations