Group 1: State Opportunities - PowerPoint PPT Presentation

1 / 46

Title: Group 1: State Opportunities

1

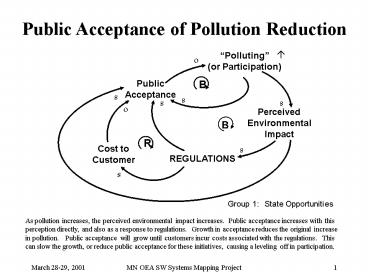

Public Acceptance of Pollution Reduction

?

Polluting (or Participation)

o

Public Acceptance

s

s

s

s

o

Perceived Environmental Impact

Cost to Customer

s

REGULATIONS

s

Group 1 State Opportunities

As pollution increases, the perceived

environmental impact increases. Public

acceptance increases with this perception

directly, and also as a response to regulations.

Growth in acceptance reduces the original

increase in pollution. Public acceptance will

grow until customers incur costs associated with

the regulations. This can slow the growth, or

reduce public acceptance for these initiatives,

causing a leveling off in participation.

2

Overall public sentiment depends on strength of

NIMB and cost concerns

Overall Public Concern About Water/Air Quality

o

o

Local Ground Water/Air Actual Quality

o

s

Regulations Monitoring

s

Public Concern About Cost

o

s

s

Technology Costs

s

Group 1 State Opportunities

As local ground water/air quality is degraded, it

is corrected by both regulations and monitoring

and an increase in public concern which supports

these initiatives. As the costs are spread to

all the public, the overall public concern for

cost decreases the water/air quality concern and

support for regulations and monitoring. Only the

local public maintains a heightened concern for

the air and water quality, and relative cost

insensitivity.

3

Increased Landfilling Reduces Resource Recovery

Creating Self-fulfilling Prophesy

Waste to Resource Recovery

o

- Other factors driving this shift

- Laws

- Cost

- Generation level

- Reduction/Increase

- Recycling

- Capacity

Waste to Landfill

s

o

Ability to sustain RR facilities

Group 2 System Analysis Update

4

Market Size Is a Fundamental Limit to Adam

Smiths Invisible Hand(s)

Market size

o

o

Price

Supply

Demand

s

s

Group 2 System Analysis Update

5

Corrugated container demand follows overall

business cycle

o

o

Price

Supply

Demand

s

s

s

Demand for Old Corrugated Containers

- Other factors

- Regulatory Pressure

- Nat. Resource Value (loss)

- Division Credit

Group 2 System Analysis Update

6

Technology drives participation through

increasing convenience

Participation

s

s

R

Technology improvements

s

Convenience e.g. of sorts

Group 2 System Analysis Update

7

Tipping In State or Out of State

Creating a Self-fulfilling Prophesy

s

Cost of In State Tipping

R

Cost of O.O.S. Tipping

Landfilling Out-of-State

s

- Other factors

- Political will

- Waste Increases

- Processing Capacity

o

Group 2 System Analysis Update

8

Legislative solutions to crises take a long time,

and can create oscillation.

Constituent Interest

s

Crisis / Awareness

Legislative Interest

s

o

Legislative Interest

Now

1970

Time

Group 2 System Analysis Update

9

Increasing Economies Leads to Decreased

Competition

Volume per Hauler

s

o

Economies of scale / scope

s

Competition

of Haulers

o

s

o

Price to Consumer

Group 2 System Analysis Update

10

Health of Natural Resource will spiral downward

if limit is reached.

Pollution

- Factors affecting pollution

- Manufacturing

- Consumption

- Design

- Factors affecting behavior change

- Education

- Cost

- Policy

s

Natural Cleansing Rate

Environmental Impact

R

s

s

o

Health of Environmental Resource

Group 3 Costs/Investments, Education

11

Organized Waste Disposal System in Moorhead with

Govt Control

Volume

R

Service Provider Fee Setting

Recovery

Tip Fees

Total Cost for Service Provider

Collection

Group 3 Cost / Investment

12

Education can help reduce environmental impact if

environmental options are available

Key Players in Education Government Consumers Civi

c Orgs Business Citizens Schools

Public Awareness

s

s

Availability of Environmental Options

Environmental Education

s

s

Environmental Impact

Responsible Actions

o

Group 3 Education

13

When facility capacity increases, businesses work

to find markets to increase volume.

Waste Generation

s

Population

s

s

R

Facility Capacity

Economic Strength

s

s

s

Waste Processing Disposal

o

s

s

s

Facility Utilization

Other Drivers

R

o

In or Out-of-State Marketing

Group 4 Role of Public/Private Sector

14

State level policy can inform federal

understanding and policy.

Quality of Federal Env. Policy

s

Competing Interests

s

o

MN Environmental Policy

Federal Understanding

s

s

s

MN Quality of Understanding

s

Other States Understanding

Group 4 National Challenges

15

Barriers to profits increase out-of-state

disposal, which increases barriers.

s

Garbage Out-of-State

Barrier to Profits

R

s

- Examples of barriers

- Taxes

- Tip Fee

- Regulation

- Others

Group 5 Tools

16

Design changes can reduce packaging costs and

waste for manufacturers.

Consumer Convenience

s

s

Waste Management

Packaging Waste

B

s

o

s

s

Cost of W.M. recycling/disposal

Marketing Value of Packaging

Required Shipping Protection

Group 5 Goals Ideals

17

Education increases until it achieves an implicit

goal or limit, then decreases.

s

B

Recycling Rate

Education

o

Group 5 Goals Ideals

18

Fundamental limit to increasing public interest

may be cost

Regs

s

s

s

Cost to Public

Public Interest in Environment

Perceived Pollution

R

o

s

- Other Limit

- Complexity

Group 1 State Opportunities

19

Legislative Activity Limited By Special Interests

Manage Your Limits

Special Interests

s

s

s

Legislative Activity

Constituent Interest

Lobbying Activity

s

o

s

s

Situation (Crisis Awareness)

Group 2 Systems Analysis Update

20

Response to crisis can be limited or reinforced

by special interests.

Special Interests (Lobbyists)

o

s

s

s

Crisis (perception) Awareness

Constituent Interest

Legislative Activity

s

o

Group 2 System Analysis Update

21

History of SWM Post WWII

I3 EPR Zero Waste Green Euro Stds I1

?

New Facilities 1970-85

Dramatic Waste Increase 1950-1970

Slow Increase in Recycling Industry

Consolidation 1997-2001

Nimby I2 Recycling 1985 Env. Mvt. No New Burners

Dramatic Increase Recycling

1 Decline in Waste 1996-1997

1985-1997

Group 2 System Analysis Update

22

Percentage MSW Disposed Out-of-State Limited By

Siting Concerns

Inability to Site/Expand OOS Landfills

s

o

Per Ton of in-state Processing

Out of state Available Capacity

MSW Out of state

s

o

o

o

Per Ton OOS

s

Cost-effective in-state disposal options

Group 2 System Analysis Update

23

MSW Shifting the Burdens

Manage the Waste (Focus of Resources on Disposal)

Recycling Programs

s

s

o

s

o

o

Focus on Conservation

Increasing MSW

Shift of Focus Away From RRR

Increasing MSW

o

o

s

s

Waste Reduction Reuse

o

Reduce, Reuse, Recycle (Zero Waste)

s

Group 2 Systems Analysis Update

24

Use of Recycling Material is limited initially by

flow, then capacity

Total Processing Capacity

Recycled Material Availability

Demand for Recycled Material

s

o

s

Vol. Purchase of Recycled Material

Convenience Low Cost

o

o

s

s

Available Processing Capacity

Group 3 Costs/Investments

25

Facility Owners Investments Pay off Long-term

Competition Regulations

s

s

s

- Sales

- Service

- Products

Capital Expenditures

Waste Volume Profit

R1

o

s

s

R2

s

Processing Capacity

R2

B1

Profit

R1

Group 4 Role of Public/Private Sector

26

Perceived Value of Waste Abatement may be a limit

to abatement technology.

Perceived Value of Abatement

s

Waste Reduction

Maximum Cost

s

s

Available Technology for Abatement

Waste Abatement Goals

R

s

B

s

Abatement Cost

s

o

Group 5 Goals Ideals

27

Past Leadership Attempts Create Barriers to New

Efforts

Waste Management Act Tools

o

s

Legal Challenge

B

R

s

s

Contention

Lack of Policy Direction

R

s

o

s

s

Lack of Funds

B

Fear

s

o

New Tools that solve Funding Issues

o

Group 1 State Opportunities

28

Taxes to cover program shortfall decrease ability

to develop alternative incentives.

Taxes / New Tools

s

B

s

o

Tax Burden Legality Issues

Program Funding Shortfall

R

o

B

s

Funding Alternatives (Eliminate Program Mandates)

o

Group 1 State Opportunities

29

Bypassing costly environmental protective

disposal is Fix That Fails

Refuse Derived Fuel Disposal Utilization (Env.

Protective)

s

s

LF/OOS Disposal Costs

Bypass More Costly () Disposal to Out of state

Landfill

o

s

Removal of HHW From Stream and Toxics

s

Clean Up Costs (Front and back end)

o

Environmental Damage

s

Group 1 Market Development

30

Development of the recycling business using

incentives for supply demand

Cost

Quality

s

Total Recyclable Waste flow

s

Availability

s

s

Demand for Recycled Materials

s

Recycling Volumes

Recycling Goals (Mandates)

s

s

s

s

s

Recycling Participation

Recycling Costs

Recycling Revenues

s

s

o

o

Waste Requiring Disposal

s

Profitability

Group 2 System Analysis Update

31

Manufacturing Leadership and Consumer Education

Necessary to achieve multiple goals.

Recycling Movement

Educate Public on Choices

o

B

o

s

Manufacturers Waste Cost

Refillables

B

s

B

o

o

- Cost to consumer

- Program - indirect

- Product - direct

Group 2 System Analysis Update

32

If SWT excess is returned, it will reinforce SW

generation.

- Solid Waste Tax

- Support Prog

- Incentives to Reduce

Economic Boom

s

B

s

s

o

B

SW Generation (landfill closure program)

Excess SWT returned (despite percd

revenue cap)

o

B

s

o

Support for MSW Reduction

Group 3 Costs/Investments

33

Planning should Include Stakeholders to solve

complex issues.

Assured WasteSupply

o

Court Dec. Carbone

o

B

B

o

o

s

R

Ability to Make Debt Service

s

Waste Flow Out-of-State/ Other Facility

Anticipated Landfill Cost

s

B

o

s

Competitiveness of County Tip Fees (Taxes, etc.)

Group 4 Role of Public/Private Sector

34

Continuously improve understanding of life cycle

costs, recognizing lag in implementation

Identify SW Technologies Life Cycle Costs

s

B

o

o

R

Inappropriate SW Technologies Implementation

Inconsistent Funding/Attn. Per Hierarchy

SW Technologies

o

B

Taxes User Fees

s

s

Fund SW Tech w/ Public/Private Funds to Max.

Env. Protection

s

Group 4 Role of Public/Private Sector

35

Subsidies can have unintended side-effects.

Transfer Tax Subsidized to Recycling

o

- Rebates

- Markets

- Curbsides

SW Flow to Local Facilities

s

B

o

o

(When) Net Cost of Recycling Disposal Cost

Local Debt (Defaults)

R

o

o

B

Available

s

s

Development of Cost Effective Markets/Infrastructu

re

Group 5 Goals Ideals

36

Solid Waste Options to Map

- 1. Landfill (including Gas Recovery and Bio

Reactor) - 2. Reduce

- 3. Recycling

- 4. Waste to Energy (including Ash Utilization)

- 5. Composting

- 6. Reuse

- 7. Hazardous Waste Management

- C D

- Home Burning/Dumping

37

Natural Resources (not waste)

38

Consumer Behavior Choices

39

Consumer Education and Understanding

Consumer Understanding

40

Composting Stock and Flows

41

Home Burning Stock and Flows

42

Landfill Stocks and Flows

Not Bio-reactor landfills

43

Recycling Stocks and Flows

44

Waste-to-Energy Stocks and Flows

45

Hazardous Household Waste Stocks and Flows

46

State Opportunities Stocks and Flows

Recommended

CrystalGraphics Presentations