Global Cost of Capital - PowerPoint PPT Presentation

1 / 41

Title:

Global Cost of Capital

Description:

To calculate a WACC for a 'multiple layer' financing, you need to figure out the ... Negotiable certificates issued by a US bank to represent the underlying stock ... – PowerPoint PPT presentation

Number of Views:74

Avg rating:3.0/5.0

Title: Global Cost of Capital

1

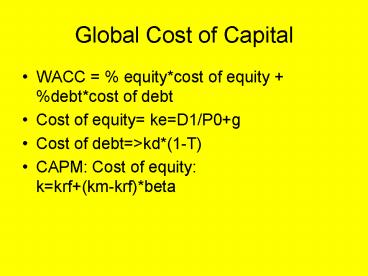

Global Cost of Capital

- WACC equitycost of equity debtcost of

debt - Cost of equity keD1/P0g

- Cost of debtkd(1-T)

- CAPM Cost of equity kkrf(km-krf)beta

2

How to calculate

6(1-30)

41.3(14-4)

3

WACC

- To calculate a WACC for a multiple layer

financing, you need to figure out the amounts of

each type of financing and therefore its weight - To do this, they must all be in the same

currency, so use the exchange rates

4

Which pieces?

5

What are the components

6

Market Liquidity Marginal Cost of Capital (MCC)

- Degree to which a firm can issue new security

without depressing the existing market price. - Degree to which a change in price of firms

securities elicits a substantial order flow - Eventually, as companys needs expand the

marginal cost will increase (I.e, the next

increment will be more expensive)

7

The Role of International Capital Markets in

Market Liquidity

- Euromarkets

- Individual capital markets

- Expand the supply of capital for a firm, when

domestic market is saturated

8

Market Segmentation

- A national capital market is considered segmented

if the required rate of return on securities in

that market differs from the required rate of

return on securities of comparable expected

return and risk that are traded on other national

securities markets

9

Reasons for Market Segmentation

- Information barriers

- Transaction costs

- Foreign exchange risk

- Takeover defenses

- Small country bias

- Political risk

- Regulatory barriers

10

Implications

- Marginal cost of capital higher when in

segmented market lower when integrated markets - Potential risk reduction because of global beta

foreign stocks are not closely correlated with US

stocks. - FX risk and return in international portfolios

(return on security, return on currency)

11

Cross-listing abroad

- Liquidity of existing shares (ADRs)

- Increased share price

- Liquid secondary market

- Acquisition of local firms

- Visibility, acceptance

- Local management compensation (and global,

sometimes) - But some barriers (disclosure, etc.)

12

Depositary Receipts

- American Depositary Receipts (occasionally

referred to as American Drawing Rights in web

sources) - Negotiable certificates issued by a US bank to

represent the underlying stock - Use eliminates some issues with dividends and

transfer of ownership

13

Financing Considerations

- When companies look for debt financing, they

always need to look at-quantity of money

needed-maturity-type of repayment stream - When a multinational firm looks at debt

financing, currency denomination arises as

another issue to consider

14

Typically

- Company wants to finance current assets with

current liabilities and long term assets with

long term liabilities (maturity matching) - Depending on how conservative or aggressive a

firm is, they may finance all or part of

permanent current assets with long term funds to

avoid refunding risk

15

Adding the Global Dimension

- Operating exposure management may call for

matching foreign currency assets with foreign

currency liabilities - Focus on balance sheet or income statement

exposure? - Cash flow should be the focus!

- Effective cost of fx denominated debt includes fx

risk component (calculation)

16

Effective cost

- Foreign Exchange risk can add to the effective

cost of debt - Proceeds of loan Calculated at current spot rate

at the time of borrowing - Repayment Calculated at ending spot rate

- Kd (1kFd)(1change spot)-1

- change spot (S1-S2)/S2100 (indir)

17

To compare financing alternativesover a period

of more than an year

- In order to compare financing alternatives, you

need to compare the US (parent currency) cash

flows - To calculate the effective rate for a multiple

year period, you need to calculate the IRR - Remember, a currency weakens IF you can buy more

of it with 1 and strengthens if you can buy less

of it with 1

18

Pricing Terms Review

- LIBORLondon Interbank Offered Rate deposit rate

applicable to interbank loans Used as a

reference rate - Borrowers usually pay a premium over the base

rate (LIBOR or other) - Up front fees are sometimes paid they impact the

effective cost of the credit (net proceeds less

than face amount)

19

ECP EMTN(Calculate Present Value)

- Euro Commercial Paper market price can be

calculated as MPFace Value/1(N/360)(Y/100)

-Ndays remaining to maturity-Yield in annual

(market) - Pricing of EMTN is more complex-Present value

of each payment must be calculated (including

principal at end)-Days as of payment

interval-Discount factorannual yield adjusted

to reflect payment period

20

Capital Structure Review

- Cost of capital changes as the amount of debt

increases as portion of the capital - Debt capital is generally less expensive than

equity capital, up to a point where the risk of

insolvency becomes too high - Cost of capital for large firms generally lower

than smaller firms (access)

21

Adding the global dimension

- US Multinational firms have lower cost of capital

than domestic only firms, or multinationals

domiciled in illiquid markets - The US MNCs have essentially a flat Marginal Cost

of Capital curve, while the others face an

increasing MCC due to lower available supply of

financing

22

Adding the global dimension

- Multinational firms may be in a better position

to support higher debt due to diversification of

cash flows - This assumes that geographic areas are at least

at different stages of economic cycles - Given recent and current headlines, do you buy

this argument or not?

23

Hedging Interest Rates

- See table 14.5 for full summary.

- If you have a payment due, you can sell a future.

- If rates go up Futures price falls, short earns

a profit - If rates go down Futures price increases, short

earns a loss - They offset the changes in the rate.

24

Foreign Affiliates

- Foreign direct investment can be political hot

potato - Affiliate capital structure can have an impact on

how the investment is viewed by the host

country-Debt ratio norms vary-Minimum own

capital and insolvency (Finland example) - Localizing financial structures has both

advantages and disadvantages

25

The best course to follow?

- Ultimately, the wealth of the shareholders of the

multinational firm will likely be maximized by

borrowing at the lowest effective cost (after

adjusting for fx risk) to reduce the WACC - Therefore, paying attention to cosmetics at the

local level may be suboptimal

26

Funding sources for financing Foreign Affiliates

- Internal funds

- Funds from within the corporate

family-Parent-Sister affiliates-Parent

guarantees - Funds from external sources-Parent

country-Outside parent country-Local (where

affiliate is)

27

Should a company invest abroad?

- Options available to enter a foreign market-100

DFI in an affiliate-Joint Venture with local

firm-Exporting-Licensing-Management contracts

28

Strategic motives

- New markets for products

- Cheap or hard to transport raw materials

- Production efficiency where a factor of

production is cheaper - Access to technology/expertise-foreigners coming

to US-what about US firms in Russia, India? - Political safety

29

Capital Budgeting

- Identify investment outlays-purchase,

transportation, installation of

equipment-increases in working capital - Identify annual cash flows-any relevant cash

flow, positive or negative, due to decision to go

ahead with this project, including opportunity

costs-do not consider sunk costs - Identify terminal cash flows-salvage value of

equipment/operation-recovery of working capital - Discounted cash flow/discount rate

30

Adding the global dimension

- Parent cash flows (even though financial)

- Project cash flows (operational)

- Affiliate to affiliate opportunity costs

- Tax, political, legal constraints

- Ways to reposition funds

- Inflation differences and FX fluctuations

- Segmented market opportunity

- Tax and other incentives, political risk

31

Project Point of View

- In local currency

- Does project meet criteria from a local

company/market perspective-is return competitive

with local investor expectations/minimum (govt

bonds) - ..from a parent perspective, what influences

shareholder value..? Cash flow!

32

Repatriation Flows

- Dividends - as return on capital investment

- Principal and interest - as payment for borrowed

funds - Intra-firm sales (transfer pricing) or products

and services - Royalties and license fees

33

Repatriation Flows and Taxes

- Dividends distributed after tax, as in the US

- Interest payments before tax, as in the US

- Transfer prices may lower foreign tax liability,

but remember the issues - Royalties and license fees reduces foreign tax

liabilities - Tax gross up for tax calculations?

- Blocked funds?

- Adjust cash flows for higher risk?

34

Capital Budgeting Process

- 1. Define the cash flows for foreign operation

for periods 0 through n a) Initial /Investment/

Outlayb) Annual Cash Flows (Rev, Cost, Depr,

Taxes, Add Back Depr)c) Terminal Cash Flow - Notesa) Working Capital increase in initial

outlayb) You depreciate cost

35

Capital Budgeting Process

- 2. Determine Annual Cash Flows to Parenta)

Dividend (Net Income? Net Income plus

Depreciation? Restrictions?)b) Other - 3. Translate to Parent Currency at rates

applicable rates (can do at different points in

the process but must do before take PV)

36

Capital Budgeting Process

- 4. Determine Terminal Cash flow (yr n)a) Sales

proceeds (if you sell for book value, after tax

issame as before tax) or PENet Income in

Yrnb) Infinite stream of dividendsc) Working

capital recovery - 5. Determine Value and of delayed repatriation

of Blocked Funds in yr n a) Reinvest (calculate

FV at year n of each years)b) Calculate Present

value of FV - 6. Calculate sum of all Present Values

37

When Calculating Cash Flows

- Often you need to calculate Revenues based on

units and price. Both may change over the time

frame. - Unit cost may also be given and needs to be

multiplied by volume - A dividend to the parent may be the only parent

cash flow

38

Example - Assumptions

We use these assumptions to build an income

statement and cashflow to the parent

39

Example Income Statement and Cash flow to parent

Units Price

Units cost

80 0f NI

Last Div/ 20

40

Another Example(In class if time)

41

(No Transcript)

Recommended

CrystalGraphics Presentations