Chapter 12 Cash Forecasting

1 / 20

Title:

Chapter 12 Cash Forecasting

Description:

Forecasting Methods: Pro Forma Statements. Based on the percentage-of ... Pro Forma Statements (continued) Generate projected balance sheet and income statements. ... –

Number of Views:1093

Avg rating:3.0/5.0

Title: Chapter 12 Cash Forecasting

1

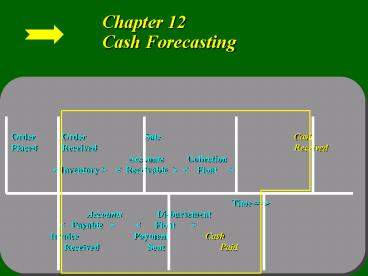

Chapter 12Cash Forecasting

Order Order Sale

Cash Placed Received

Received

Accounts Collection lt

Inventory gt lt Receivable gt lt Float

gt

Time gt Accounts Disbursement

lt Payable gt lt

Float gt Invoice

Payment Cash

Received Sent

Paid

2

Objectives of Cash Forecasting

- Liquidity Management

- Financial Control

- Strategic Objectives

- Capital Budgeting

- Cost Management

- Currency Exposure

3

Steps in the Cash Forecasting Process

- Step 1

- Forecast Horizon and Intervals

- Step 2

- Variable Identification

- Step 3

- Modeling the Cash Flow Sequence

- Step 4

- Model Estimation

- Step 5

- Model Audit

4

Short-Term Forecasting Horizon

- Daily or weekly forecast for a period of up to a

month. - Aids in cash concentration transfers, funding

disbursement accounts, and making short-term

borrowing and investment decisions. - Helps in setting and managing balances used for

bank compensation.

5

Medium-Term Forecasting Horizon

- Also referred to as cash budgets.

- Forecast for 1 to 12 months.

- Used to determine the need for short-term credit

or availability of funds for short-term

investments. - Can be used as a benchmark of performance by

comparing actual cash flows to forecast cash

flows.

6

Long-Term Forecasting Horizon

- Forecast covers any period beyond one year.

- Are strategic forecasts used in long-term

financial planning. - Used by financial institutions and rating

agencies for credit analysis and evaluation.

7

Forecasting Philosophy

- Number and type of forecasts

- Expenditure on forecasts

- External versus internal forecasts

- Quantitative versus judgmental forecasting

8

Degree of Certainty

- Certain Flows

- Predictable Flows

- Less Predictable Flows

9

Data Identification

- Sources

- Identification

- Account Structure

- Reporting Requirements

- Historical Data

10

Forecast Method Selection

- Establishing Data Relationships

- Selecting a Method

- Testing Relationships

- Managing the Costs of Forecast Systems and Data

11

Forecasting Methods

- Methods for Short-Term Forecasting

- Receipts and disbursement forecast

- Distribution forecast

- Modified accrual

- Methods for Medium- and Long-Term Forecasting

- Pro forma statement

- Adjusted net income

12

Statistical Tools

- Causal methods

- Regression

- Time-series methods

- Moving average

- Exponential smoothing

- Time-series regression

- Model estimation

- Model audit

13

Forecasting MethodsReceipt and Disbursement

- Receipt Schedule

- Disbursement Schedule

- Both schedules are prepared on a cash basis.

- Completed forecast indicates the projected

deficiency or surplus of funds in relations to a

companys minimum cash requirement.

14

Forecasting Methods Distribution Forecast

- The total estimated cash flow is spread over the

days in the forecast horizon using proportions

that are using actual historical patterns. - Easy and inexpensive to prepare.

- Allows the incorporation of seasonality and

trends. - Large data requirements for proportion estimation.

15

Forecasting Methods Pro Forma Statements

- Based on the percentage-of-sales method.

- Requires a sales forecast.

- Determine balance sheet and income statement

items that can be assumed to be a constant

percentage of sales. - Assume other balance sheet and income statement

items are constant or can be updated based on

available information.

16

Pro Forma Statements (continued)

- Generate projected balance sheet and income

statements. - If projected assets are greater than projected

liabilities and equity, there is a projected cash

shortage. - If projected assets are less than projected

liabilities and equity, there is a projected cash

surplus.

17

Statistical Forecasting Time Series Forecasting

- Simple Moving Average

- Gives equal weight to past observations

- Will always lag any trend in actual cash flow.

- Approach can be useful in identifying cycles and

patterns of past data but does not take these

patterns into account in the forecast

18

Time Series (continued)

- Exponential Smoothing

- Allows the cash flow forecast to be adjusted by

the prior period forecast error. - Allows for more weight to be placed on the most

recent actual cash flows by choosing a smoothing

constant close to 1. - Forecaster must select the smoothing constant.

- Simplest version of the technique will lag trends

in the data.

19

Forecast Validation

- In-Sample Validation

- Out-of-Sample Validation

- Ongoing Validation

20

Summary

- The chapter began with a discussion of the

philosophy and environment within which cash

forecasts are made - The value of forecasts is to borrow less or

extend investment maturities - The five steps of forecasting were developed and

two major time intervals were presented - Forecast models were divided in two categories

causal and time-series - We discussed daily forecasting in the context of

the distribution method

Recommended

CrystalGraphics Presentations