Pprice of debt security0.5 - PowerPoint PPT Presentation

1 / 13

Title:

Pprice of debt security0.5

Description:

Thus the debt reduction raises AV for 2 reasons: Relative payments d/D, rise. P rises. ... Mv is the change in the market value of debt (=Expected ... – PowerPoint PPT presentation

Number of Views:37

Avg rating:3.0/5.0

Title: Pprice of debt security0.5

1

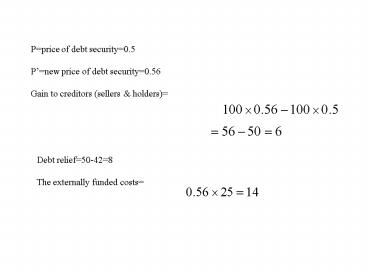

Pprice of debt security0.5 Pnew price of

debt security0.56 Gain to creditors (sellers

holders)

Debt relief50-428 The externally funded costs

2

Cross Section

3

(No Transcript)

4

Gain to sellers

Gain to holdout creditors

Total gain to creditors

5

Emerging Markets 1997

- Korean Crisis (1997)

- Liberalization of capital account was associated

with 120 billions of capital inflows, 1992-1997.

Reversals of flows in second half of 1997 thru

1998 generated a downturn in the economy and debt

problem but this time mostly to private sector

and financial intermediaries- although there was

a substantial Intl bail out.

6

Brady Bonds Deal

- A country issues new bonds (Brady Bonds) with a

reduced rate of interest, and with Industrial

Country Coovts guarantees. Thus the market will

purchase these bonds since they are credit

worthy. - Resources obtained from the Brady Bonds issue

will be used to buy back the country old debt.

(on which the country was not credit worthy) - Thus, the real amount to a combination of

external funding (not thru grants but through

good credit) that finances a buy back of old debt.

7

Price

1

New price

0.56

Old price

AV

0.5

MV

Nominal debt

100

75

25

8

Knocked DownSecondary-market debt

prices,September, 1991, of face value

9

International Cross-Section Regression

- Pprice

- DNominal Debt

- XExports

- GGrowth rate

10

At D

11

Debt Reduction and Expected Repayments Effect on

probabilities.

Dface value VpD(1-p)d

Marginal change in probability of good state when

face value increases by 1 unit

- Thus the debt reduction raises AV for 2 reasons

- Relative payments d/D, rise

- P rises.

12

AV Average of debt 0.5 (price) MVMarginal

value of debt0.33 (1/3)

MV

Mv is the change in the market value of debt

(Expected repayment to creditors) if the

NOMINAL debt is increased by 1 unit.

13

PDV

Debt relief Laffer Curve

D

D

1

P

AV

D

D

MV

Recommended

CrystalGraphics Presentations