STRATEGIC COST MANAGEMENT BA122B Spring 2005Slide 51

1 / 11

Title:

STRATEGIC COST MANAGEMENT BA122B Spring 2005Slide 51

Description:

Sets costs in the commitment phase-concurrent engineering ... Value engineering. Identify components for cost reduction. Generate cost reduction ideas ... –

Number of Views:35

Avg rating:3.0/5.0

Title: STRATEGIC COST MANAGEMENT BA122B Spring 2005Slide 51

1

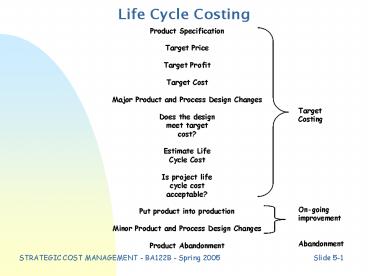

Life Cycle Costing

Product SpecificationTarget PriceTarget

ProfitTarget CostMajor Product and Process

Design ChangesDoes the designmeet target

cost?Estimate LifeCycle CostIs project life

cycle cost acceptable?Put product into

productionMinor Product and Process Design

ChangesProduct Abandonment

TargetCosting On-goingimprovement Abandon

ment

2

Product Cost Life Cycle

- R D

- Design

- Production

- Marketing Distribution

- Customer Service

Upstream(focus for earlysettlement here)

Downstream

3

Shift in Strategic Impact

- Shift focus from manufacturing costing to

- Upstream or downstream focus using the value chain

4

Target Costing

- Customer Orientation

- Sets costs in the commitment phase-concurrent

engineering - Supports keiretsu model via the value chain

- Price led costing

- Cross functional product teams

- Focuses on life cycle costing

5

Target Costing Process

- Establishment phase

- Market research

- Competitor analysis

- Niche definition

- Customer requirement definition

- Product feature definition

- Market price determination

- Profit rate

6

Target Costing Process

- Attainment phase

- Cost gap computation

- Design costs out

- Design release and continuous improvement

7

Cost Reduction

- Cost analysis

- Components list

- Functional analysis

- Customer requirement ranking

- QFD Matrix

- Relative functional rankings

- Value engineering

- Identify components for cost reduction

- Generate cost reduction ideas

- Testing and implementation

- Cost estimates required at each design iteration

8

Value-Index Analysis

- Choose features and options based upon customer

preference - Value-Index Cust. Preference Feature

Cost - VI gt 1increase spending

- VI lt 1decrease spending

9

TC-Strategic Implications

- Quality is improved through the customer focus of

target costing - Cost reduction is the heart of target costing

- Time reduction is a natural by-product due to

concurrent engineering

10

TC-Attribute Implications

- Technical

- Decision relevance improves (quality, cost and

time issues are integrated) - Process understanding improves

- Behavioral

- Early finance involvement and teamwork are

mandated - Undesirable attributes of longer development,

burnout, feature creep internal conflict can be

managed

11

TC-Attribute Implications, cont.

- Cultural

- Organizational culture must be prepared

- Commitment to sustaining values must be

established - Customer focus

- Cross-functional cooperation

- Open sharing of information

Recommended

CrystalGraphics Presentations