Net Present Value NPV - PowerPoint PPT Presentation

1 / 3

Title:

Net Present Value NPV

Description:

Yr Net return x Discount factor = Present Value. 0 -100 x 1.0 = -100. 1 25 x 0.952 = 23.8 ... Present Value of total cash inflow = 108.25. NPV = 8.25 ... – PowerPoint PPT presentation

Number of Views:803

Avg rating:3.0/5.0

Title: Net Present Value NPV

1

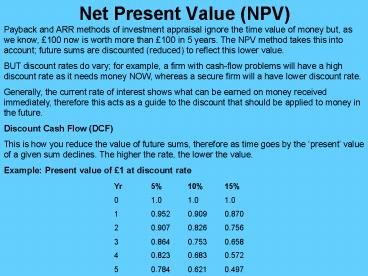

Net Present Value (NPV)

Payback and ARR methods of investment appraisal

ignore the time value of money but, as we know,

100 now is worth more than 100 in 5 years. The

NPV method takes this into account future sums

are discounted (reduced) to reflect this lower

value. BUT discount rates do vary for example, a

firm with cash-flow problems will have a high

discount rate as it needs money NOW, whereas a

secure firm will a have lower discount

rate. Generally, the current rate of interest

shows what can be earned on money received

immediately, therefore this acts as a guide to

the discount that should be applied to money in

the future. Discount Cash Flow (DCF) This is how

you reduce the value of future sums, therefore as

time goes by the present value of a given sum

declines. The higher the rate, the lower the

value. Example Present value of 1 at discount

rate Yr 5 10 15 0 1.0 1.0 1.0 1 0.952

0.909 0.870 2 0.907 0.826 0.756 3 0.864 0.75

3 0.658 4 0.823 0.683 0.572 5 0.784 0.621 0.

497

2

Calculating the NPV Example Project A costs 100

initially. It then provides an annual return of

25 for 5 years. The discount rate is 5. What is

the NPV? Yr Net return x Discount

factor Present Value 0 -100 x 1.0 -100 1

25 x 0.952 23.8 2 25 x 0.907 22.675 3

25 x 0.864 21.6 4 25 x 0.823 20.575

5 25 x 0.784 19.6 Present Value of

total cash inflow 108.25 NPV 8.25 In

accounting terms, the investment produces a

profit of 125-100 25. In NPV it is only 8.25.

BUT this is still a positive outcome. On

financial grounds, any positive NPV is worthwhile

(and vice versa).

- Advantages of NPV

- Considers the time value of money.

- Good for analysis of single projects.

- A positive NPV means accept, a negative means

reject.

- Disadvantages of NPV

- Based on an arbitrary discount rate.

- Time consuming and harder to calculate.

- Difficult to understand.

3

Investment Appraisal- comparisons of various

methods