Audit Reports under Various Circumstances - PowerPoint PPT Presentation

1 / 9

Title:

Audit Reports under Various Circumstances

Description:

'less likely than not' 'more likely than not' less than 'probable' 'probable' ... loss .5 .5. b. Pending litigation--fixed damages. material loss. Severe ... – PowerPoint PPT presentation

Number of Views:39

Avg rating:3.0/5.0

Title: Audit Reports under Various Circumstances

1

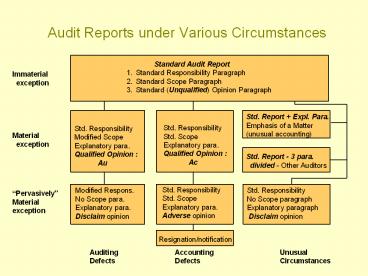

Audit Reports under Various Circumstances

Standard Audit Report 1. Standard

Responsibility Paragraph 2. Standard Scope

Paragraph 3. Standard (Unqualified) Opinion

Paragraph

Immaterial exception

2

Certification (source chooses measurement

criteria and auditor -- will it work?)

Auditor

Audit Report

Management

Investors

Audited Financials

3

Accounting Measurement Types

- Hard numbers - attached to physical (fiscal)

quantities of primary transactions cash,

receivables, inventory, fixed asset additions,

payables, related sales and cost of sales - Allocations - spread hard numbers over time,

segments, units produced depreciation expense,

accumulated depreciation, goodwill amortization,

overhead assignment. - Accounting estimates - approximate value of

transactions or losses that may occur in the

future or have occurred bad debts, warranty

expense, for inventory obsolescence losses - Uncertainties - disclosure of possible losses

that cannot yet be quantified as a point

estimate, but affect interpretation of current

financial statements.

4

Probability that an event or condition has or

will occur

5

Three Loss Contingency Distributions

a. Pending warranty costs

of possible loss

3.0

1.5M

M

0

6

Conditions and Events That May Indicate

Substantial Doubt about an Entitys Ability to

Remain a Going Concern

- Negative (financial) trends

- Other indications of possible financial

difficulties - (loan defaults, refinancing, lack of compliance)

- Internal matters (labor problems, unfavorable

long-term commitments, dependence on particular

project success) - External matters that have occurred

Source SAS No. 59 (ACIPA, 1988), para. 6

7

Going-Concern Auditing and Reporting--U.S. GAAS

Review Conditions, Events, and Audit Findings

8

Auditors Reporting Decision Model

Real-world conditions of client related to

Fee potential

Personal observation and audit firms client

selection/ retention policies

Auditing Procedures

General Guidance and criteria

Auditor

GAAP

Mental image of client conditions

GAAS and professional ethics

Utility function

Knowledge and skills

Processing

CPA firm policies

Laws and regulations

Decision (adjust, disclose modify report, resign)

Audit contract

Audited financial statements

Audit report

9

World Wide Acquisitions, Inc.(reverse the

reporting process)

- Co. A - divided audit report

- Co. B - going concern paragraph

- Co. C - except for (unjustified acctg. change)

- Co. D - accounting change paragraph (D has none)

- Co. E - related party paragraph

- Co. F - standard report -- any problems?

Recommended

CrystalGraphics Presentations