DOUBLE TAX RELIEF - PowerPoint PPT Presentation

1 / 15

Title:

DOUBLE TAX RELIEF

Description:

MIXER COMPANIES ... attraction therefore to mix high and low rates through a mixer company ... Although the mixer cap would allow a maximum of 60 if only the ... – PowerPoint PPT presentation

Number of Views:333

Avg rating:3.0/5.0

Title: DOUBLE TAX RELIEF

1

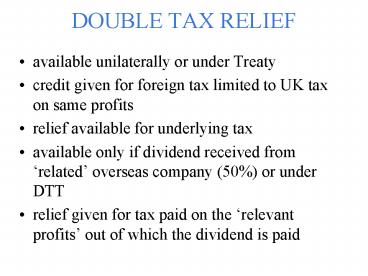

DOUBLE TAX RELIEF

- available unilaterally or under Treaty

- credit given for foreign tax limited to UK tax on

same profits - relief available for underlying tax

- available only if dividend received from

related overseas company (50) or under DTT - relief given for tax paid on the relevant

profits out of which the dividend is paid

2

TA 1988 s792(1) underlying tax means, in

relation to any dividend, tax which is not

chargeable in respect of that dividend directly

or by deduction

3

MIXER COMPANIES

- Restriction of relief to UK tax might result in

dividends from high rate countries not being

fully relieved while dividends from low tax

countries would have UK tax still to pay - attraction therefore to mix high and low rates

through a mixer company - had become commonly used with Holland being a

popular location - could involve an ADP dividend from a CFC

- attacked in FA 2000

4

Country X Country Y Mixer Profits 2,000,0

00 4,000,000 6,000,000 Overseas

tax 1,400,000 1,000,000 2,400,000 Dividend

paid to UK 600,000 3,000,000 3,600,000 Underly

ing tax 1,400,000 1,000,000 2,400,000 Gross 2,

000,000 4,000,000 6,000,000 UK corporation tax

(30) 600,000 1,200,000 1,800,000 Credit for

foreign tax (600,000) (1,000,000)

(1,800,000) UK tax payable NIL

200,000 NIL Unused foreign tax credits

800,000 600,000

5

FA 2000 CHANGES

- relief for overseas tax will be capped at 30

- mixing with dividends from CFCs relying on the

distribution exemption will not be permitted - a pooling of other overseas dividends will be

allowed with underlying tax up to 45 - excess credit can be carried back 3 years or

carried forward indefinitely against the same

pool - a form of group relief will also be available for

excess credits

6

MIXER CAP

- S 799(1A)

- INTM164220

- Applies only to underlying tax

- relief limited to stated formula

- does not apply to dividends mixed within same

country - ADP dividends segregated out from 2001

- relief for excess credits

7

LIMIT ON OVERSEAS TAX

(D U) x M D Dividend U underlying

overseas tax M maximum relievable rate (UK

corporation tax rate at time dividend is paid)

8

UK

140

BV

80

60

H 100-40

L 100-20

9

Dividend Tax attributable Mixer cap

formula Credit allowable L to

BV 20 (80 20) x 30 30 20 H to

BV 40 (60 40) x 30 30 30 BV to

UK 60 (140 60) x 30 60 60

Although the mixer cap would allow a maximum of

60 if only the final dividend from BV to the UK

were considered, because the mixer cap has also

been applied to each component dividend the

maximum credit is restricted to 20 and 30, total

50. There will be an additional 10 tax payable on

the part of the final Case V dividend that

represents the dividend from L. Case V income

(gross) 200 UK corporation tax

60 DTR (50) Tax payable 10 Eligible

unrelieved foreign tax 10 (60 -50)

INTM164230

10

UK has a subsidiary A in country A that in turn

holds three subsidiaries B pays a dividend to A

of 85 in respect of which it has paid underlying

tax of 15 C pays a dividend to A of 100 in

respect of which there is nil underlying tax but

10 withholding tax is payable D pays a dividend

to A of 60 in respect of which it has suffered

underlying tax of 40. A then pays a dividend of

235 up to the UK.

11

UK

235

A

100-10

60

85

B a CFC paying an ADP

C a CFC with exempt activity

D trading company

12

(D U) x M Company D Company C (6040) x 30

30 (limit) (9010) x 30 30

(limit) actually paid 40 actually

paid 10 relieved 30

relieved 10 excess 10

excess - EUFT NB if D had

incurred tax of 50 the EUFT would have been 15

(ie 45 -30)

13

Case V Computation ADP dividend 85

Residual dividend (235-85) 150 Underlying tax

15 Underlying tax (10 40) 50

Gross dividend 100 Gross dividend 200

CT 30 CT _at_ 30

60 DTR (15) DTR

(10 30) (40) Net UK tax

15 Net UK tax 20 Eligible

unrelieved foreign tax (EUFT) 10

14

PRE FA 2000 POSITION

Dividend received 235 Underlying tax

(151040) 65 Case V income 300 Corporation

tax _at_ 30 90 DTR (65) Tax payable

25

15

2009 Proposals

Change from taxing foreign dividends and

relieving double taxation through crediting

foreign tax, towards an exemption from taxation

on certain dividends Replace CFC rules with

a controlled company (CC) regime, which would

be an income-based regime under which the

mobile or passive income of all 10 per cent

subsidiaries of large and medium-sized

UK-resident companies would be taxed in the

United Kingdom To change the current regime

in respect of interest relief for the costs of

funding foreign activities and profits

Recommended

CrystalGraphics Presentations