Allowances and reliefs - PowerPoint PPT Presentation

1 / 18

Title:

Allowances and reliefs

Description:

Allowance given automatically to all UK residents and some non residents (eg EU residents) ... The allowance is given in full in the tax year in which a ... – PowerPoint PPT presentation

Number of Views:49

Avg rating:3.0/5.0

Title: Allowances and reliefs

1

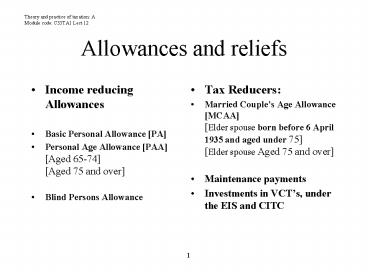

Allowances and reliefs

Theory and practice of taxation AModule code

C33TA1 Lect 12

- Income reducing Allowances

- Basic Personal Allowance PA

- Personal Age Allowance PAAAged 65-74Aged

75 and over - Blind Persons Allowance

- Tax Reducers

- Married Couples Age Allowance MCAAElder

spouse born before 6 April 1935 and aged under

75Elder spouse Aged 75 and over - Maintenance payments

- Investments in VCTs, under the EIS and CITC

1

2

Allowances and reliefs

- INCOME REDUCING ALLOWANCES

2

3

Application of Income reducing Allowances

- The allowance is deducted from

- the taxpayers Statutory Total Income (S.T.I.)

- to give taxable income.

- This has the effect of reducing the amount of

income - on which income tax must be paid.

- Relief will therefore effectively be obtained at

the individuals marginal rate of tax - i.e. the highest rate of tax that an individual

pays.

3

4

INCOME REDUCING ALLOWANCES - Personal Allowances

- Determining factors

- Age of individual

- Level of income received (in some cases)

4

5

INCOME REDUCING ALLOWANCES - Basic Personal

Allowance

- Basic Personal Allowance PA

- Allowance given automatically to all UK residents

and some non residents (eg EU residents) - The allowance is given in full in the tax year in

which a taxpayer is born or dies - The allowance is specific to the individual - any

unused personal allowance PA of one spouse can

never be transferred to the other or to anyone

else - The PA for 2006-07 is 5,035

5

6

BASIC PERSONAL ALLOWANCESEXAMPLE 1

- Mrs Green, aged 45 on 6 April 2006 had income of

3,000 in 2006-07 - (a) Calculate her taxable income for the year

- (b) What proportion of her personal allowance may

be transferred to her spouse? - SOLUTION

- Statutory total income

3,000 - Personal allowance

3,000 Taxable income

NIL - Her unused personal allowance 2,035

(5,035-3000)may not be transferred to her spouse

6

7

BASIC PERSONAL ALLOWANCESEXAMPLE 2

- Mr Black, aged 59 on 6 April 2006 has income of

30,000 for 2006-07 - He died on 1 February 2007.

- Calculate his taxable income for 2006-07

- SOLUTION

- Statutory total income

30,000 - Personal allowance

5,035 - Taxable income

24,965 - The personal allowance is given in full in the

year of death (or birth).

7

8

INCOME REDUCING ALLOWANCES Personal Age

Allowances

- Personal Age Allowance PAA

- For those aged over 65, or who reach the age of

65 during the tax year the personal allowance is

increased to 7,280 for 2006-07 - For those aged over 75, or who reach the age of

75 during the tax year the personal allowance is

increased to 7,420 for 2006-07 - The allowances are given in full in the year in

which the taxpayer dies - Unused allowances are not transferable

8

9

INCOME REDUCING ALLOWANCES - Personal age

allowances

- Reduction of personal age allowance

- If an individuals Statutory Total Income (STI)

is above a certain limit, the allowance will be

reduced - The allowance can not be reduced below the basic

personal allowance available to all taxpayers - When a taxpayer makes a donation under Gift Aid

the STI that is compared with the income limit

must be reduced by the gross amount of the

donation. - In other words the STI arrived at if the gross

amount of the gift aid payment was included in

the computation like an annual charge (Dont

include it twice)

9

10

INCOME REDUCING ALLOWANCES Personal Age

Allowances

- RESTRICTION OF AGE-RELATED ALLOWANCES 2006-07

- The full amount of the allowances may be claimed

where the Statutory Total Income does not exceed - 20,100 (The upper income limit)

- Where this is exceeded, the excess is calculated

and the PAA is reduced by ONE-HALF of this

excess

10

11

INCOME REDUCING ALLOWANCES Personal Age

Allowances

- Mr Brown is 65 on 15 December 2006.

- His income for 2006-07 is 10,000

- Calculate his taxable income for the year.

- SOLUTION

- Statutory total income

10,000 - Less Personal allowance

7,280 - Taxable income

2,720 - The personal age allowance is given since Mr

Brown attains 65 in the year of assessment The

full allowance is given since his income did not

exceed the Upper income limit of 20,100.

11

12

INCOME REDUCING ALLOWANCES Personal Age

Allowances

- Mrs Grey was born on 1 April 1932. Her income for

2006-07 was 23,000 - Calculate her taxable income for the year.

12

13

Personal Age AllowanceMrs Grey Solution

- Restriction of allowance

- Statutory total income

23,000 - Less upper income limit

20,100 - Excess of income 2,900

- Personal age allowance Aged 75 on1/4/07ie during

tax year 2006-07 7,420 - Less restriction 1/2 excess of 2,900

1,450

- PAA

5,970 - This can not be reduced below 5,035

- Taxable income 2006-07

- Statutory total income

23,000 - Personal allowance

5,970 - Taxable income

17,030

13

14

INCOME REDUCING ALLOWANCES - Blind Persons

Allowance

- An allowance of 1,660 is available to a person

who is registered blind at any time during the

tax year - The allowance is available for the year before

registration, if proof of blindness were obtained - A married couple who are both blind may each

claim the allowance - A married blind person may transfer unused blind

persons allowance to his/her spouse and same sex

civil partners (whether or not blind)

14

15

INCOME REDUCING ALLOWANCES - Blind Persons

Allowance

- Example

- Angela, aged 60 on 6 April 2006, has an annual

salary of 30,000. - She has a loan of 14,000 at 10 to buy shares in

her employee-controlled company, and another loan

of 10,000 at 14 to buy a conservatory for her

house. - She receives Bank interest (net) of 1,000 per

annum. - Her husband is registered blind but has no income

of his own. - What is her taxable income for 2006-07?

15

16

INCOME REDUCING ALLOWANCES - Blind Persons

Allowance

- Solution

- Total Non- Savings

- Savings

- Salary 30,000 30,000

- Bank int 1,000x100/80 1,250

1,250 - 31,250 30,000 1,250

- Less charge

- 14,000_at_10 1,400 1,400

- STI 29,850 28,600 1,250

- Less Personal allowance -5,035 -5,035

- Blind PA -1,660 -1,660

- TAXABLE INCOME 23,155 21,905 1,250

16

17

INCOME REDUCING ALLOWANCES - Blind Persons

Allowance

- Example

- Mrs Green (aged 45 at 6 April 2006) is registered

blind. Her income for 2006-07 is 5,000. - 1. Calculate her taxable income for the year

- 2. What proportion of her personal allowances may

be transferred to her (sighted) spouse?

17

18

INCOME REDUCING ALLOWANCES - Blind Persons

Allowance

- Solution

- 1.Statutory total income

5,500 - Personal allowance 2006-07 5,035

- Blind persons allowance 465

5,500 Taxable income

NIL - 2.Surplus of BPA transferable to spouse

1,660-465 1,195 - The unused part of her Blind Persons Allowance

may be transferred to her spouse irrespective of

whether or not he is sighted.

18